Global| Jul 16 2008

Global| Jul 16 2008Euro Area HICP Sees Core Decelerate

Summary

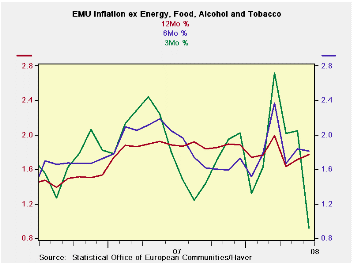

Although the ECB policy remains steadfastly fixed on the behavior of the HICP headline, it is the HICP core that is showing signs of behaving. The six month pace of the core at 2.3% is as low as it has been since Oct 2007 (eight [...]

Although the ECB policy remains steadfastly fixed on the behavior of the HICP headline, it is the HICP core that is showing signs of behaving. The six month pace of the core at 2.3% is as low as it has been since Oct 2007 (eight months ago). The three-month pace at 1.3% is as low as that metric has been since March of 2006 (twenty seven months ago). The trends may be too good to be true or even lasting but for now they are a note of optimism in an otherwise rotten policy environment. Moreover I think their message is the right one.

Headline inflation, the ostensible ECB target rate, is not supposed to rise more that 2% Y/Y. I fact the headline pace has not been below 2% since August of 2007. The current pace is 4.0% double the targeted top pace.

However the sharp drop in the Zew index this week has everyone in Europe thinking about coming weakness. This may be one reason that oil prices finally became vulnerable on Mr Bernanke’s remarks yesterday, as oil fell an outsized $6/bbl.

There has been a certain denial of the transmission of the US business cycle to Europe and to the rest of the world. But with so many benefiting from US demand it is hard to understand where that view originated. Europeans seemed to foster a view of newfound invincibility but the jump in inflation has undermined that. And the view itself helped the euro to climb to new heights, but now there is evidence of growth fading more severely and that will test the ECB and likely bring the euro down a notch or two.

While the ECB does not make the core HICP the centerpiece of policy the fact that core inflation has decelerated to 1.3% over three months from 2.3% over six months and 2.5% over 12-months seems to say that there is some progress on the inflation front apart for the headline where oil especially is wreaking such havoc. The ECB does have some authentic scope to be a bit pragmatic on the inflation front due to the kind trend in core inflation. A weakening economy will give it more lee way still.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Jun-08 | May-08 | Apr-08 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.5% | 0.6% | 0.0% | 4.1% | 4.1% | 4.0% | 1.9% |

| Core | 0.2% | 0.2% | -0.1% | 1.3% | 2.3% | 2.5% | 1.9% |

| Goods | 0.4% | 0.8% | 0.6% | 7.6% | 6.0% | 4.9% | 1.5% |

| Services | 0.3% | 0.4% | -0.1% | 2.2% | 2.5% | 2.5% | 2.6% |

| HICP | |||||||

| Germany | 0.5% | 0.6% | -0.4% | 2.7% | 3.2% | 3.4% | 2.0% |

| France | 0.5% | 0.5% | 0.1% | 4.5% | 4.0% | 4.0% | 1.3% |

| Italy | 0.6% | 0.4% | 0.0% | 4.2% | 4.6% | 4.0% | 1.9% |

| Spain | 0.6% | 0.7% | -0.1% | 4.9% | 4.5% | 5.0% | 2.4% |

| Core excl Food Energy & Alcohol | |||||||

| Germany | 0.1% | 0.3% | -0.5% | -0.4% | 0.8% | 1.8% | 2.1% |

| France | #N/A | 0.1% | 0.1% | #N/A | #N/A | #N/A | 1.4% |

| Italy | 0.4% | 0.2% | -0.1% | 1.9% | 3.1% | 3.0% | 1.9% |

| Spain | 0.3% | 0.3% | -0.1% | 2.2% | 2.6% | 3.4% | 2.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief