Global| Aug 23 2016

Global| Aug 23 2016Euro Area Flash PMIs Make Gains But Fail to Impress

Summary

The EMU composite PMI for August was last stronger in March but last persistently stronger from February 2015 to January 2016. At 53.3 the PMI gauge for the EMU is in the top 67th percentile of its historic queue of data back to [...]

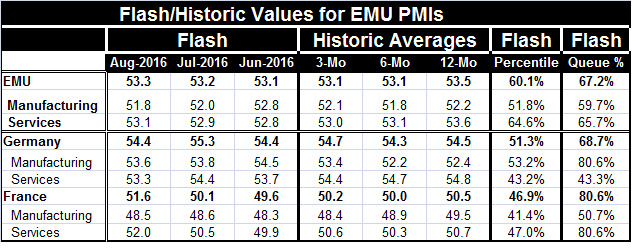

The EMU composite PMI for August was last stronger in March but last persistently stronger from February 2015 to January 2016. At 53.3 the PMI gauge for the EMU is in the top 67th percentile of its historic queue of data back to January 2011. Although at a level of 53.3, the PMI shows little momentum as it is barely above its three-month and six-month averages, both at 53.1. The EMU services sector has the relative strongest queue standing for this period at its 65.7 percentile. EMU manufacturing stands only in its 59.7 percentile. But services momentum is fading as its diffusion reading's average fades from 12-month to six-month to three-month. The current month at 53.1 is barely above its three-month average. Manufacturing momentum is substantially flat with a weaker six-month average than its 12-month average, but an uptick for the three-month average yet with a current month that is below its three-month average. Those twists and turns do not add up to a lot of momentum. Despite this being the strongest composite EMU PMI in five months, it is not very impressive.

The EMU composite PMI for August was last stronger in March but last persistently stronger from February 2015 to January 2016. At 53.3 the PMI gauge for the EMU is in the top 67th percentile of its historic queue of data back to January 2011. Although at a level of 53.3, the PMI shows little momentum as it is barely above its three-month and six-month averages, both at 53.1. The EMU services sector has the relative strongest queue standing for this period at its 65.7 percentile. EMU manufacturing stands only in its 59.7 percentile. But services momentum is fading as its diffusion reading's average fades from 12-month to six-month to three-month. The current month at 53.1 is barely above its three-month average. Manufacturing momentum is substantially flat with a weaker six-month average than its 12-month average, but an uptick for the three-month average yet with a current month that is below its three-month average. Those twists and turns do not add up to a lot of momentum. Despite this being the strongest composite EMU PMI in five months, it is not very impressive.

The German composite, or private sector PMI, fell month-to-month but has a stronger standing than the EMU PMI at its 68.7 percentile. Germany has a much stronger queue standing with an 80th percentile mark for manufacturing, contrasting with its very weak 43rd percentile standing for services. Germany's manufacturing PMI has mixed trends and the manufacturing gauge is lower month-to-month. But its moving averages show a stronger three-month average than six-month average and the August manufacturing PMI is ahead of its three-month average. Services show a steady erosion in the average values for its PMI from 12-month to six-month to three-month with the current reading for August weaker still and falling month-to-month. These opposite sector trends make it difficult to handicap the German economy. Its overall PMI fell month-to-month on weaker services and weaker manufacturing.

France saw its composite PMI rise month-to-month by one and one-half points, a very solid pick up. Still, the monthly averages for the French composite PMI have been stuck barely above the breakeven mark of 50. With this month's surge, the French composite rises to 51.6, well below the German and EMU diffusion values but with its 80.6 percentile standing. The French manufacturing sector eroded in August and continues to contract as it has been doing on average on the last three, six, and 12 months. Still, that sector has been so hopelessly stuck below neutral that at that mark France's manufacturing sector is still barely above its median (calculated back to January 2011). The French services sector picked up in August, rising to 52.0 from 50.5, a sharp month-to-month gain. Still, this strength is not echoed by trend. The services readings for France clusters around a diffusion value of 50 over the past year and erodes from 12-month to six-month but picks up from three-month to six-month. The French service sector diffusion measure at 52 in August is its strongest reading since October 2015. The August level represents an 80th percentile standing for services in France.

In August, we see France and Germany each with different relative strength. France is driven by a rebound in services while Germany sees somewhat weaker growth in both sectors. On balance, the EMU statistics do not look compelling this month either. France's services sector is impressive for the one month, but that jump comes out of the blue. More recently, France has been bemoaning the slowdown in tourism, something that should undermine its services sector. Because of terrorism concerns, tourism to France is off sharply. France's tourist board data show hotel stays are down 8.5% in the Ile-de-France region for the first half of 2016. Foreign tourist stays are down by 11.5%. With this as background, it is hard to take the rebound in French services too seriously. In addition to tourism, there has also been flooding in Paris that has disrupted the tourist trade. We will want to see if this French service sector gain has legs beyond August.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief