Global| Dec 20 2016

Global| Dec 20 2016Euro Area Current Account Surplus Shrinks

Summary

The EMU-wide current account and trade balances both contracted in October. Exports fell for the second month in a row while imports rose, more than shaking off their decline in September. In terms of 12-month trends, exports are [...]

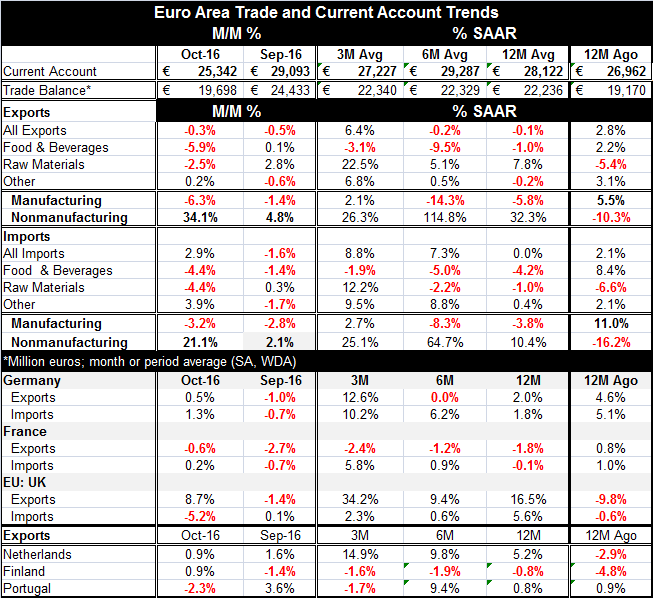

The EMU-wide current account and trade balances both contracted in October. Exports fell for the second month in a row while imports rose, more than shaking off their decline in September. In terms of 12-month trends, exports are lower by 0.1% from their level of 12-months ago while imports are dead flat. However both exports and imports are gaining some momentum over recent months; both show positive three-month rates of growth, for example.

The EMU-wide current account and trade balances both contracted in October. Exports fell for the second month in a row while imports rose, more than shaking off their decline in September. In terms of 12-month trends, exports are lower by 0.1% from their level of 12-months ago while imports are dead flat. However both exports and imports are gaining some momentum over recent months; both show positive three-month rates of growth, for example.

Manufactures trends tell a story of ongoing lethargy

If we break export and import trends into trends for manufactures vs. nonmanufactures, what emerges is that the real strength in both flows (such as it is) comes from nonmanufactures. Oil prices have been swinging higher and these are all nominal figures so the higher oil and other commodity prices filter through to read as higher values of imports and exports. This robs the nominal data of signaling power for growth. However, if we confine our view to the trends for manufactured goods, we find exports are contracting over 12 months and six months then post a weak 2.1% annual rate gain over three months. Similarly, for imports manufactures show declines over 12 months and six months but a gain of 2.7% at an annualized rate over three months. Despite the recent pick up in both flows, the overriding view is that exports and imports remain weak in the EMU.

Some are stronger

In the bottom portion of the table, we offer some trends for individual EMU members or of other countries in Europe to better identify trends. However country level data, especially for trade, are always subject to a good deal of volatility. Here we see strength over three months in nominal German exports and imports in the U.K. as well as in U.K. exports and strength in Dutch exports. But over 12 months, both German flows post growth of 2% or less while the U.K. (with a weak and weakening exchange rate) logs a strong, 16.5%, export gain and Dutch exports mount a firm gain of 5.2%.

Some are weaker

Conversely, French exports are lower over three months and 12 months, as are Finnish exports. Portugal has an export drop over three months and a weak rise of 0.8% over 12 months. Imports that will be weighted toward fuels in Europe show gains but not strong ones in Germany and in the U.K. with French imports lower over 12 months by just 0.1%.

Summing up trade trends

On balance, we see some considerable variation in trade tends. But only U.K. and Dutch exports are really strong and solid throughout their trend. For the EMU as a whole, manufactures which are relatively freer of commodity price fluctuation effects show weak imports and exports with the most recent data subject to huge variations in the categories of other exports and other imports. But the signals from manufactured goods trends remain lethargic for exports but do show some ongoing expansion for imports.

Oil, OPEC and dash of geopolitics

Oil is a major problem to deal with in trade data analysis. To make matters worse OPEC is implementing its embargo selectively. It has cut its allocations to the U.S. and kept its deliveries up in Asia. This sort of cutback pattern can also distort local trade patterns. While oil prices are firming for now, the acid test for OPEC will come over a longer stretch of time when its cohesion and the enticement to cheat will be grater. Historically OPEC has had a hard time holding the cartel together. And while some news articles are praising the Saudis for their leadership, the fact is that the Saudis led and no one followed forcing them to take the brunt of the cutbacks from their own allocation. They had tried to overproduce oil and send pain to other OPEC members, but oil market conditions were too slack and their own ability to pump more was being strained, at least in the short run. In the end, it was better for the Saudis to take a bigger cutback on their own and bide their time trying to draw others into the fold with smaller cuts or output freezes intended to soak up the oil excess slowly as growth returns. With oil production gaining in the U.S., the Saudis have cut their oil allocations the most to the U.S.

Some think that the Saudis and others have learned their lesson and that OPEC will maintain discipline. But before the financial crisis, the Saudis had completely taken their eye off the ball and allowed oil to trade up to near $150/barrel, a price not in the Saudi long-term interest but one that brought needed revenue to finance the Saudi's growing adventures. I am not so sure that Saudi Arabia has the same degree of disciple it used to. Its 'needs' have changed. It certainly does not have the same degree of power or of influence among oil-producers. And it is depends on nonmember Russia to cut for this plan to work and Russia is another country with severe budget issues. It is still under the strain of sanctions for its activities in Crimea and Ukraine.

Now the political relations among OPEC members are worse than they used to be and OPEC depends on the cooperation of many nonmembers for its success as well. In the meantime, the higher that spot oil prices go, the more extra output will be coming from the U.S. This wrinkle makes the OPEC price-firming game a real tightrope and all the more vulnerable to any cheating. It is not clear to me that OPEC has the skill, determination or cohesion to play this game effectively over the longer term. Some think they do and that they have learned their lesson. This view will be tested. In the past, greed has won out. I don't see that changing. I will give the firming price trend as much as six months before I think we will see it showing the strains of cheating.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief