Global| Mar 21 2014

Global| Mar 21 2014Euro Area Current Account Continues Run Up

Summary

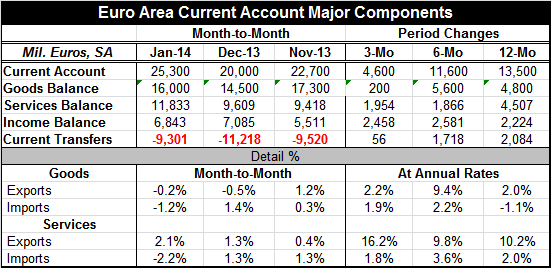

The euro area current account surplus moved even higher in January as goods exports pulled back slightly and goods imports fell relatively sharply. Over three months export and import growth rates are pretty similar, a 2.2% pace for [...]

The euro area current account surplus moved even higher in January as goods exports pulled back slightly and goods imports fell relatively sharply. Over three months export and import growth rates are pretty similar, a 2.2% pace for exports compared to a slightly slower 1.9% pace for imports. However, sticking with goods flows, year-over-year exports are up by 2% while imports are down by 1.1%. These are the figures plotted the chart on the left.

The euro area current account surplus moved even higher in January as goods exports pulled back slightly and goods imports fell relatively sharply. Over three months export and import growth rates are pretty similar, a 2.2% pace for exports compared to a slightly slower 1.9% pace for imports. However, sticking with goods flows, year-over-year exports are up by 2% while imports are down by 1.1%. These are the figures plotted the chart on the left.

While the chart hints at some ongoing improvement in imports, pay attention to the scale. Notice that imports are simply falling by less on a year-over-year basis in the most recent periods. While that is progress of sorts, it doesn't help to stimulate demand anyplace else in the world. And with exports posting some positive growth, the two trends together help to push out the trade surplus and bloat the current account surplus of the European Monetary Union (EMU). These trends are further accentuated by the performance of services trade where export growth has accelerated from 10% year-over-year to over 16% at an annual rate over three months. During this period the imports of services in the euro area are up only 2% year-over-year and growing at an even weaker 1.8% annual rate over three months.

The current account surplus has gone from about 13.5 billion euros on average over the past 12 months to a 25 billion euro pace in January. The goods balance has gone from 4.8 billion euros over 12 months to a 16 billion euro pace in January. The services balance has gone from 4.5 billion euros to an 11.8 billion euro pace in January. The income balance has also grown sharply from 2.2 billion euros over 12 months to 6.8 billion euros in January. What has weakened has been the current transfer account. Current transfers have gone from about 2.1 billion euros over 12 months to a pace of -9.3 billion euros in January. This rapid step down the pace (.step up in the negative pace) reflects much of what's wrong with the global economy. Since the euro area is running a large surplus, it contributes to forcing other countries to running balancing deficits. Europe, especially Germany and France, have a lot of guest-workers operating in their economies because those workers found economic opportunity with better jobs than these workers could get at home. As a result, many these workers send monies home and this is largely reflected in the current transfers. Conditions in the rest of the world are so weak that workers in the euro area countries are increasingly sending funds home to help families overseas; there continues to be substantial pressure for this sort of flow instead of creating jobs in the home countries of the guest workers.

The world economy needs more growth. If the largest economies of the world won't provide that growth and won't provide increasing domestic demand, it's going to be even harder for the rest of the world to make its recovery. The United States has already been running substantial and persistent current account deficits. The US is doing more than its share to help stimulate the rest of the world economy in contrast with the euro area that is running large and rising current account surpluses.

The world economy needs to find some balance and stop countries from running persistent surpluses and deficits. This requires some realignment in growth rates and probably a shift in currency exchange rates as well. However, there is no sign that any such policy coordination is underway nor is there any sign that persistent deficit countries are trying to use the framework under the World Trade Organization (WTO) to achieve balance by demanding redress from countries that are running these kinds of persistent surpluses. I continue to mark this behavior as a substantial stumbling block to achieving sustained growth for the world economy.

Undoubtedly, the euro area has its internal issues, and in some way, having a growing surplus helps to augment GDP in the region. That much is good news for the EMU, at least. However, we know and that the composition of the surplus has a lot to do with Germany which has the largest current account surplus of any country in the world and that the countries in the euro area where growth is still lagging are also lagging in terms of their trade competitiveness and trade performance. When we gaze upon EMU trade performance, we have to be aware of its underlying heterogeneity.

When we look at statistics for the euro zone, we're looking at statistics for trade from the zone to areas outside of the zone. All of the intra-zone trade is ignored in this calculation. This is appropriate since that's trade within the currency area; while it does cross national borders, it doesn't cross the border of the euro zone which is the area that we are inspecting. Similarly, when we look at exports from the US, we look at exports that cross the US international borders and we do not include shipments made from Michigan to Ohio or California to Nevada.

The euro area in January shows an increase in the goods balance and also shows an increase in the services balance. The income account surplus is slightly smaller in January than it was in December. Posting negative numbers on a more continuing basis, are current transfers which did `grow' slightly in January compared to December as the negative outflow diminished. However, over earlier periods the current transfers were positive numbers. That trend is shifting.

The biggest problem in the euro area has been growth, plain and simple. Its inability to prop up domestic demand enough to support import growth is part of that larger problem. The region needs to develop domestic demand so it can put people to work and create imports to generate demand to help growth in the rest of the world. While the euro area and the European Central Bank undoubtedly are more focused on what happens inside of the region, the euro area is a big enough region that we have to be concerned about its impact on the rest of the world economy as well. And with Germany, the country with the largest current account surplus in the world, embedded in the euro area statistics, the euro area has a long way to go in order to create some increase in its domestic demand and stimulus for the rest of the world.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.