Global| Jul 30 2020

Global| Jul 30 2020EU Sentiment Indexes Continue Their Rebound

Summary

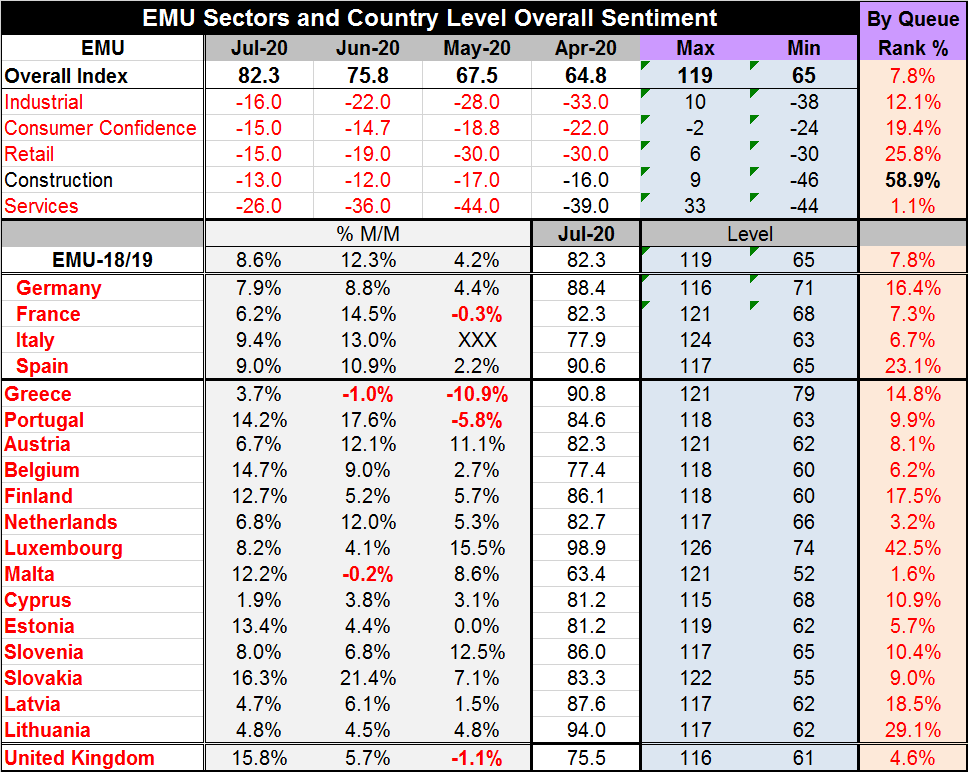

The European Commission economic sentiment gauge for the EMU improved again in July, rising to 82.3 from June’s 75.8. However, it still has a queue standing in its 7.8 percentile, marking it as lower than this less 8% of the time. The [...]

The European Commission economic sentiment gauge for the EMU improved again in July, rising to 82.3 from June’s 75.8. However, it still has a queue standing in its 7.8 percentile, marking it as lower than this less 8% of the time. The rebound is ongoing, but it is slow. In fact, the rebound is so slow that the EMU-wide unemployment rate ticked higher to 7.8% in June from 7.7% in May. Because of renewed virus outbreaks, recovery from the initial phase of infection has been, and continues to be, uneven.

The European Commission economic sentiment gauge for the EMU improved again in July, rising to 82.3 from June’s 75.8. However, it still has a queue standing in its 7.8 percentile, marking it as lower than this less 8% of the time. The rebound is ongoing, but it is slow. In fact, the rebound is so slow that the EMU-wide unemployment rate ticked higher to 7.8% in June from 7.7% in May. Because of renewed virus outbreaks, recovery from the initial phase of infection has been, and continues to be, uneven.

Sector results

This month three of the five indicators in the EU index improved. The improving metrics were for the sectors: industry, retail, and services. Their improvement month-to-month was substantial in each case. The weakening gauges were for (1) Consumer confidence, that slipped by a small amount from -14.7 to -15 and (2) Construction, that sector fell back to a -13 reading in July from -12 in June. Despite the fact that three gauges improved and two deteriorated, the clear signal here is that improvement was the trend of the month. The deteriorations were small while the gains were large.

Country results

That explains why every early reporting EMU member (18 of them) showed month-to-month improvement in July. The smallest index gain was a rise of 1.9% in Cyprus, followed by 3.7% in Greece, 4.7% in Latvia and 4.8% in Lithuania.

Six counties made month-to-month gains measured in double digits led by Slovakia, Belgium, and Portugal. Among the big four economies, Spain and Italy each had gains on the month of 9% or more, but neither quite reached double digits. The overall EMU gauge gained by 8.6% in July, less than the 12.3% gain it logged back in June.

Queue standings

At a time when an index plunges then makes several months of increases, we tend to look at the monthly changes and indicators of improving economic health. The monthly changes are important, but we also have to get perspective on what is the level of activity that has been returned by this process. The queue standings perform that service. The overall EMU gauge has a 7.8% standing and that is lower than any of the other sector metrics except services. The service sector has a 1.1 percentile queue standing. The industrial sector stands at 12.1 percentile and consumer confidence has returned to a 19.4% mark, but construction has been resilient and it has a percentile standing above its historic median at 58.9%. Construction has been resilient overall as well as across the EMU and the United Kingdom.

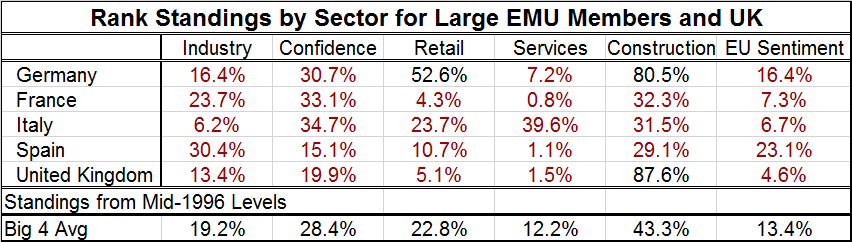

The table below breaks out the largest EMU economies: Germany, France, Italy, and Spain and adds the U.K. to the mix. In this format, the strength of the construction sector sticks out. It is clearly the strongest in Germany and in the U.K. The weakness in service is also clear. The individual sectors tend to have the highest standings in Germany and the lowest in Spain. This, however, is not borne out by the EU overall sentiment values by country because that index weights the sector metrics and industry gets a large weight. Meanwhile, industry lags in Germany and has a relatively higher reading in Spain. Those factors skew the overall EU sentiment reading.

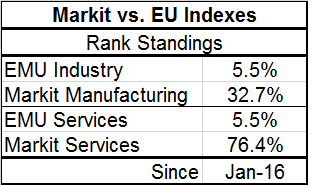

One interesting feature is how fast the Markit gauge for EMU industry and services have come back compared to the EU measures for the two EMU sectors. Measured to January 2016, the Markit services gauge has a 76.4 percentile standing in July, compared to a 5.5 percentile standing in the EU Commission framework. Manufacturing in the Markit framework has a 32.7 percentile standing, compared to a standing of 5.5 in the EU Commission framework. The Markit gauges are much more buoyant and the EU Commission is much more restrained. It’s a curious difference. And the Markit service index is almost back to a normal level (with a 76th percentile standing). That does not seem right. Could it be that the Markit gauges have overshot their mark and will have to undergo some pull back? We will see.

One interesting feature is how fast the Markit gauge for EMU industry and services have come back compared to the EU measures for the two EMU sectors. Measured to January 2016, the Markit services gauge has a 76.4 percentile standing in July, compared to a 5.5 percentile standing in the EU Commission framework. Manufacturing in the Markit framework has a 32.7 percentile standing, compared to a standing of 5.5 in the EU Commission framework. The Markit gauges are much more buoyant and the EU Commission is much more restrained. It’s a curious difference. And the Markit service index is almost back to a normal level (with a 76th percentile standing). That does not seem right. Could it be that the Markit gauges have overshot their mark and will have to undergo some pull back? We will see.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief