Global| Jun 29 2017

Global| Jun 29 2017EU Indexes Make Strong Gains in June. What's Next? Will June End the Monetary Policy Honeymoon...Soon?

Summary

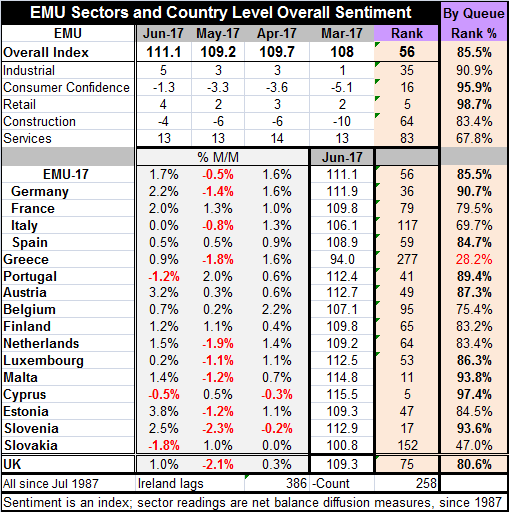

Strong gains in and across EMU The EU Commission index for all of the EMU rose to 111.1 in June from 109.2 in May. Over the last 21 years, a monthly gain this strong or stronger has occurred only 16% of the time, marking the month's [...]

Strong gains in and across EMU

Strong gains in and across EMU

The EU Commission index for all of the EMU rose to 111.1 in June from 109.2 in May. Over the last 21 years, a monthly gain this strong or stronger has occurred only 16% of the time, marking the month's gain as relatively strong. In addition, the level of the index has a historic top 15% queue standing as well. EMU activity and momentum seem solidly in place.

Markit readings are still out in front of the EU Commission gauges

We have Markit sector readings available over the last five years. By comparison, the EU index for industry shows an identical top reading for this period for the manufacturing/industrial sector as does Markit; both score manufacturing as having a top reading over the past five years. For services, the EU index is weaker with a top 22 reading by rank giving it a top one third standing among is observations of the last five years. The Markit index for services has a higher relative standing of 5 or a top 8 percentile reading. Still, both the Markit and the EU surveys put the economy on a solid and strong path- we can knit pick about the exact positioning- but the message is clear. While the Markit indexes are as strong or stronger than the EU survey, the EU survey is also quite solid viewed on its own merits.

Sectors show balance and mostly strong growth

By sector, the EMU industrial sector viewed on a broader basis on data back to July 1987 has 90.9 queue percentile standing; consumer confidence has a 95.9 percentile standing; and retailing has a 98.7 percentile standing, Construction has an 83.4 percentile standing and services has a 67.8 percentile standing. All of these are still quite strong with retailing and consumer confidence in the 'extremely strong' category. It is unusual for the EMU to be led by retailing and the consumer. But this, of course, is only when ranked in relative terms; the raw diffusion score still has the industrial sector stronger and services stronger still. But services usually log positive number for diffusion and that alone gives it a relatively high diffusion score among other sectors where negative readings proliferate.

Most of EMU shows momentum

The chart looks at 12-month percent changes in the EU indexes. On that basis, the second largest EMU-economy France is spurting; Italy is lagging. The EMU and Germany are making solid gains and show less indication of accelerating in June compared to earlier months.

Wow is most of EMU finally on the SAME PAGE!

The country detail on the EMU indexes shows that the EMU finally has a broad sharing of prosperity. Only three countries Portugal, Cyprus and Slovakia show backtracking on the month. In terms of the queue standings on the levels of the EU indexes, only Greece is weak, with a 28th percentile standing. After that, only Slovakia is below its median (reading of 50) with a standing at its 47th percentile. After that, the weakest queue standing is from Italy at the 69.7 percentile mark, a reading that is still quite firm and well above its median. There are four EMU members with readings in their 90th percentile and seven with readings in their 80th percentile. That's 11 out of 16 readings in the top 20th percentile of their historic queues of readings, an impressive showing.

The trappings of change

On balance, we can begin to see the worm is turning. It is clear why Germany is getting more hopped up to hike rates and why Draghi is retreating slowly in his obstinacy to them. The EMU economy not only is doing better, but the progress is now more widely shared. Based on economic performance, most members' conditions could warrant a rate hike. But that, of course, is abstracting from the ECB's key policy metric which is inflation.

Slowly I turn, inch by inch, step by step

The ECB is about inflation and inflation is still below target with core inflation stuck farther below target. And while Draghi is finally prevaricating, he is looking toward to the transition to rate hikes with a plan to make the transition slowly and deliberately.

Is inflation really gathering or is this episodic?

In data reported today, German states are starting to show some inflation lift. In the U.K., Mark Carney has admitted that at some point the U.K. would be withdrawing its stimulus. And even the Bank of Canada is now looking at the potential to hike rates perhaps as soon as July. All of this talking and repositioning has stirred up the foreign exchange markets.

Regulatory loosening meets monetary tightening

In the U.S. in the wake of successful stress tests on banks, the Fed has set banks loose on their individual proposed capital projects and a number have announced stock buy backs or increased dividend pay-outs. In Europe, there is concern that that U.S. Treasury is backtracking on Basel rules and, that in a quest for deregulation, banks will be allowed to go astray again. So we have a more mature position in the business cycle with regulation and restraint coming undone and monetary tightening either in force or about to be transitioned.

Signals on the cycle

The business cycle may not be what it once was, but these are clear signals. Perhaps not as clear as 'one if by land, and two if by sea.' but clear nonetheless. The global economy is transitioning. And if inflation is able to find a sustainable toe-hold, central banks are prepared to launch a move back toward normalcy or, at least, to make a move to dilute the punch-bowl.

Got inflation?

The question is still on inflation, however, as OPEC is still struggling to gain control of oil prices, as oil did mount an increase in price today. Despite some inflation stirring among the German states, globally goods are sill in excess supply; a real ramp up of inflation seems unlikely. The countries of the West are still high cost producers compared to Asia and Mexico and that should further keep wages under wraps. However, there is a new product cycle in gear since technology plays a stronger role in output. With more technology wage disadvantages, do not count as much against you anymore. There has been, despite the global glut and weak growth, some stimulus to manufacturing investment and output in the West even in the face of excess capacity and lower wages abroad. We have seen that wages are not rising very fast in the U.S., the UK or Germany, in relatively recent reports. All of this puts the move to automation and the ongoing supplantation of labor by the internet and by use of software in perspective and helps to explain why the job front has not become dynamic. Even when jobs return, they are not the same jobs. Instead, wages lag and domestic indicators of labor market tightness do not create wage pressures the way they would have in the past.

The new business cycle and the Heisenberg principle

The question ahead of us now is what the new business cycle will look like. It appears that we are over some sort of hump and that there is more growth and maybe even enough momentum that global economics no longer require the constant tailwind of an accommodative monetary policy in order to move ahead. Of course, that judgement is still being made for these economies with that tailwind in force. This is why Draghi is so careful about talking of its removal. Heisenberg uncertainly principles may apply here. That is once we actually exit the period of monetary accommodation conditions may no longer seem so solid.

Operation Twiggy and Dr. Seuss

In the U.S., the period of watchful waiting is over. The Fed has been staking steps out there on the thin ice and has had to pause and freeze before restarting its tightening journey. Others before it had tried tightening and had to go back. The Fed may be pausing again even as it is planning to perform 'Operation Twiggy' on its balance sheet. And other central banks are looking to follow the Fed's lead. I must say that despite these solid looking readings across Europe I still am wary of the effect of synergy, the impact of many central banks acting in the same way at the same time. Everyone thinks hey, we are taking these small or marginal steps, but in the aggregate there is more stimulus being withdrawn than what meets any one central banker's eye. With a tightening cycle, it can quickly go from one pip, two pips to cracked ice and blue lips. The more banks that get out there on that thin ice, the thicker it has to be to support everyone.

Lessons from marathon?

When the marathon is run in New York City and they start off on the Verrazano Bridge, runners are warned not to all run in-step and to create a common harmonic that could vibrate the bridge and damage it. With one runner we wouldn't mention such a risk, but with thousands it becomes a potential problem. So even if central bankers are all talking of their own small steps, let us be wary that they are all doing this together and that the sum of the parts might make a much more impactful whole than we now expect. Despite the fact that we are on the verge of a shift in the cycle, this cycle is different because it is a long expansion already. It is a weak expansion in terms of growth. It is not generating the kinds of excesses that past expansions did because of external competition and technology events. Because of this, the usual domestic pressures are not in play. In fact, we may not be entirely sure what is in play since we have not really seen this before. Although we are in a more mature stage of expansion, it is still something we have not seen before. So let's not be too sure about thinking that we know what comes next.

One suggestion...

In past cycles - as the Fed keeps reminding us- a tightening labor market and capacity use constraints would squeeze factor availability and help to boost price pressures. So the Fed is looking around rooting in those same bushes for the same sort of trouble. But in this environment, technology and trade are the key factors keeping inflation at bay. Does that mean that trouble will come from either the technology sector or from the foreign sector? Will this expansion be undone by rising inflation as in the past or will it be something else? This is where we have to be open-minded and vigilant and where central bank dogmatism will not serve it well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief