Global| Aug 28 2014

Global| Aug 28 2014EU Commission Indices Drop for EU and EMU in August to 8-Month Lows

Summary

The EU Commission indices for August have their EU and EMU headlines and sector headlines available, but country detail is only available for a few early reporters rather than for the full set of EMU members. The economic sentiment [...]

The EU Commission indices for August have their EU and EMU headlines and sector headlines available, but country detail is only available for a few early reporters rather than for the full set of EMU members.

The EU Commission indices for August have their EU and EMU headlines and sector headlines available, but country detail is only available for a few early reporters rather than for the full set of EMU members.

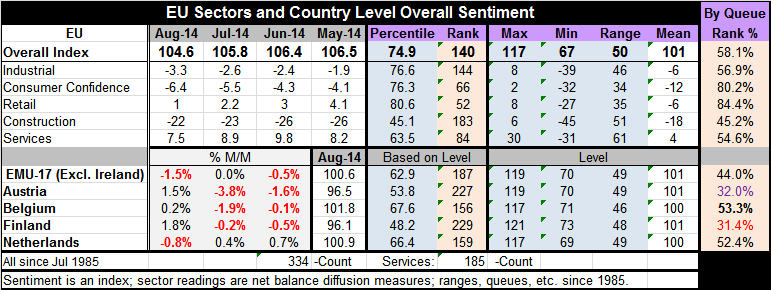

The economic sentiment indicator for the European Union fell to 104.6 in August from 105.8 in July. The industrial confidence measure for the EU fell to -3.3 from -2.6. Consumer confidence fell to -6.4 from -5.5. The retail metric fell to 1 from 2.2. The construction sector measure increased to -22 from -23. The services metric fell to 7.5 from 8.9. The EMU index fell to 100.6 in August from 102.1 in July.

The percentile standing of the EU index is now down to its 58th percentile of its historic queue. This means that the index has been higher 42% of the time and lower about 58% of the time. The median is at the ranking of the 50th percentile. The relatively strongest sector (ordered by percentile standings) is retailing in its 84th percentile, followed by consumer confidence in its 80th percentile, followed by the industrial sector in its 56th percentile. Next the services sector ranks in its 54th percentile and the construction sector ranks in its 45th percentile. These are very moderate readings.

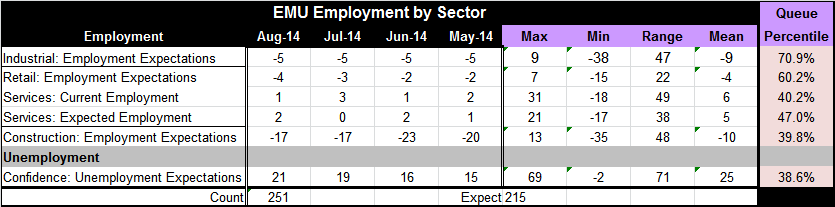

But we have (above) a table pertaining to the EMU members and their responses to various employment metrics in various sectors. Industrial employment expectations were flat at -5 in August while retail employment expectations slipped to -4 in August from -3 in July. The assessment of current employment in the services sector slipped to 1 in August from 3 in July. Expected employment in that sector, however, rose to 2 in August from 0 in July. Expected employment in the construction sector was flat at -17 in both August and in July. In the consumer confidence report, responses about unemployment expectations rose to 21 in August from 19 in July. There has been a steady, rising progression in that sector of expectations that unemployment would be rising. The responses to this question rose from 15 in May 2014 to 21 in August 2014, the current reading. However, the reading at 21 is still only a 38th percentile reading; it is substantially below its midpoint, which would be at the 50th percentile level. Unemployment expectations are heightened but are not out of control.

Country Readings

There are only a handful of EMU countries that reported economic sentiment readings for August. These early reporters are Austria, Belgium, Finland, and the Netherlands. Among these, only the Netherlands posted a decline in August at 0.8%. Finland posted a 1.8% rise, Belgium a 0.2% rise, and Austria a 1.5% rise. Each of these countries with the EMU indicator rising in August had also seen declines in both June and July in the two earlier months. There is not much strength indicated by the early reporters.

The queue standing of the economic indicators of the early reporters show Belgium at its 53rd percentile, the Netherlands at its 52nd percentile, Austrian at its 32nd percentile, and Finland at its 31st percentile. All early reporters have moderate-to-weak readings on overall economic sentiment.

Other Key News for EMU

In other important data reported today, Germany and France report increases in the number of unemployed.

The Geopolitical Front

The geopolitical news that has been hanging over the head of Europe seems to have gotten worse with Ukraine reporting outright incursions by Russian nationalist troops not just by separatists. These troops are reported to have taken over an additional city in Ukraine.

Worries are mounting that Russia may be preparing for some kind of an outright invasion. It looks as though Ukraine was beating the separatists back and, had they been successful, it would have been a black eye for Vladimir Putin. Instead of accepting that, Putin seems to have upped the ante.

Evidence suggests that Putin has been supplying the rebel separatists and even fighting on their behalf with Russian troops both in Ukraine and launching artillery attacks from Russian soil against troops in Ukraine. This is a substantial escalation and with Putin publicly denying Russian involvement or otherwise suggesting that his intentions are purely humanitarian or to protect Russian separatists in the area from unfair treatment.

All this has to leave us with considerable uncertainty about what his plans are. It looks as though the uncertainty hanging over the euro area is continuing and very possibly, worsening. This month's EU indices showed a sharp drop in the EU index. At 104.6, it was last lower in December 2013. The EMU index at 100.6 was last lower also in December 2013. We're looking at a reversal of eight months of EU and EMU progress based on the metrics in this month's EU Commission report. And now there is talk of upping the sanctions further.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief