Global| May 16 2019

Global| May 16 2019EMU Trade Surplus Withers

Summary

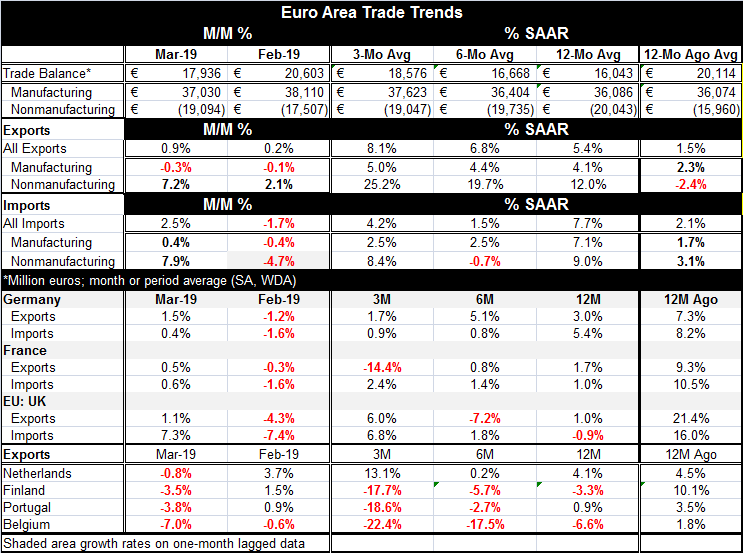

The European Monetary Area logged a smaller trade surplus in March as it fell to 17.9 billion euros from 20.6 billion euros in February. One year ago, the surplus stood at 20.6 billion euros. Exports slowed to a 0.9% gain month-to- [...]

The European Monetary Area logged a smaller trade surplus in March as it fell to 17.9 billion euros from 20.6 billion euros in February. One year ago, the surplus stood at 20.6 billion euros.

The European Monetary Area logged a smaller trade surplus in March as it fell to 17.9 billion euros from 20.6 billion euros in February. One year ago, the surplus stood at 20.6 billion euros.

Exports slowed to a 0.9% gain month-to-month as imports rose by 2.5% narrowing the surplus as imports grew faster than exports. Over 12 months imports grow faster than exports with a gain of 7.7% compared to 5.4% for exports, reducing surplus compared to one year ago. But over six months and three months, exports grow faster than imports.

Trends may be better represented by manufacturing trade. There, export growth accelerates steadily and mildly from 4.1% over 12 months to a pace of 5% over three months. On that same progression, manufacturing imports slow from a gain of 7.1% over 12 months to an annualized gain of 2.5% over three months. Over three months and six months exports outpace imports, but imports are faster over 12 months for trade in manufactures, the same as for overall trade.

Nonmanufacturing trade flows show exports with double-digit growth rates and accelerating. Imports are less steady but also grow just short of a double-digit pace over 12 months and three months. Still, import growth lags well behind export growth for nonmanufactures.

On balance, the surplus decline logged in March does not appear to be on solid footing and does not flow out of recent trends in either manufacturing or nonmanufacturing trade flows.

Of course, EMU trade is the sum of trade from all its members. But a simple summing of member trade trends might look different than the EMU aggregate. This is because members report exports by country jurisdiction while the EMU flows only count as exports those shipments outside the euro area. Germany may export to France and France to Germany, but neither of those flows is an EMU export even though each is, respectively, a German export and a French export. To sum national trade flows to agree with EMU reported trade, all country-reported exports and imports internal to the EMU must be removed.

That goes some way to explain why there is so much export weakness in March as well as over three months when we look at the country detail but do not see the same sense of weakness in the EMU-reported export flows. For example, over three months, Finland. Portugal, Belgium and France record double-digit export declines. While Germany is a larger exporter, its exports only expand at a 1.7% pace. EMU reports export gains at an 8% pace. While export strength may come from other members, the likely culprit is that internal exports among EMU members are become weaker. Over 12 months, EMU-reported exports are stronger than the exports of every country listed in the table.

The ZEW experts continue to see EMU and global weakness. German real export orders are declining over 12 months. The U.S. reported yesterday surprisingly weak retail sales and industrial output. China’s economic data have come in a bit softer than expected as well. It is too soon to call it a slip into recession, but some of the underpinnings of strength are gone. And the OECD leading indicators point to a broad-based slowdown as being in progress. A lot of data are consistent with that view.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief