Global| Nov 18 2013

Global| Nov 18 2013EMU Trade Balance Improves

Summary

The EMU trade surplus is on the rise. While that may be good for the value of the euro, it may not be a good development overall. The upright green bars in the graph tell the story of persistent surpluses, but that story is given a [...]

The EMU trade surplus is on the rise. While that may be good for the value of the euro, it may not be a good development overall. The upright green bars in the graph tell the story of persistent surpluses, but that story is given a bit more flesh by looking at the red and blue lines on the graph. Except for early 2011, EMU export growth has exceeded import growth and there has been a surplus on the trade account as a result. Moreover, the surplus has grown and it appears to be growing again. Exports appear to be ending their period of contraction while imports are not there yet.

The EMU trade surplus is on the rise. While that may be good for the value of the euro, it may not be a good development overall. The upright green bars in the graph tell the story of persistent surpluses, but that story is given a bit more flesh by looking at the red and blue lines on the graph. Except for early 2011, EMU export growth has exceeded import growth and there has been a surplus on the trade account as a result. Moreover, the surplus has grown and it appears to be growing again. Exports appear to be ending their period of contraction while imports are not there yet.

The issue here is that worldwide growth is weak. And Europe has some of the most affluent economies in the world. Yet, in this period when there is such a struggle for growth, the EMU region is relying on export penetration as one of its pillars of growth.

Running a current account and trade surplus may be good for bolstering the value of the euro, but it will not be helpful in a world environment in which many countries with less development and less growth will find that their counterpart deficits (implied by EMU surpluses) are keeping them from attaining their own growth targets.

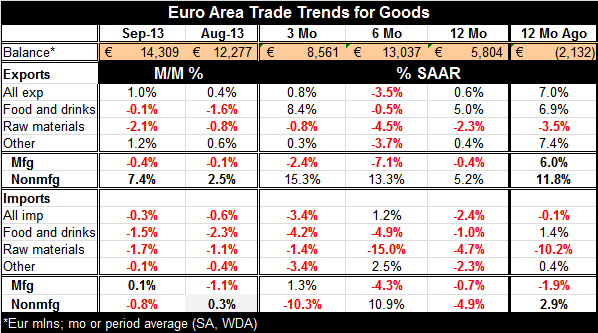

Europe's nonmanufacturing exports are growing at a very strong 15.3% annual rate over three-months and by over 5% over 12-months. For imports both manufacturing and nonmanufacturing flows are weak and are lower on balance over 12-months. Italy and Spain, for example, still have imports shrinking over 12-months. While Germany sports 12-month export growth, it pairs that with import shrinkage. The problem with the eurozone's `unbalanced growth' is that its most efficient members are growing spurring exports, but not at the same igniting a step-up in domestic demand. Europe's economies that would be more prone to imports are instead still struggling and are not importing as they normally would. One critique of this observation is that some of those imports will never go back to past-patterns- nor should they. While that is true, it is also true that the part of Europe that has not imported as much needs to import more, and that is not happening.

Germany seems to think that the rest of Europe needs to close the gap on German productivity in order to be healthy. But if that were to happen, the EMU region would become a huge juggernaut and would develop a huge trade surplus with the rest of the world! The European Monetary Union needs a plan to develop demand where it has been weak and enhance productivity where it has been weak. If it only acts to balance budgets in counties where there has been fiscal excess and to enhance region-wide productivity, it will become a region with trade problem of another sort.

Germany is already at a trade position putting it at odds with surplus rules in the European Union. We have seen the problems China ran into by pursuing export-led growth while wearing blinders. China's malaise has had implications for all nations with export led growth. It is just unclear if there will be any real global policy to address the problems created by persistent and excess surplus countries. But ignoring the issue and putting EMU on a path to become one of those is not a good idea.

Europe needs growth, but it also needs balanced growth. And right now, that is not what it is getting. Like China, it is big enough that its imbalances can cause problems for the rest of the world. That's not a good policy tilt with such fragile global economic conditions.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief