Global| Nov 18 2009

Global| Nov 18 2009EMU Trade Balance Improves

Summary

The Confederation of British Industry survey shows industrial trends continue to make progress and cut their declining trends. Still the declining trends remain large and the degree of progress is slow although this month’s gain in [...]

The Confederation of British

Industry survey shows

industrial trends continue to make progress and cut their declining

trends. Still the declining trends remain large and the degree of

progress is slow although this month’s gain in orders is one of the

sharpest.

The Confederation of British

Industry survey shows

industrial trends continue to make progress and cut their declining

trends. Still the declining trends remain large and the degree of

progress is slow although this month’s gain in orders is one of the

sharpest.

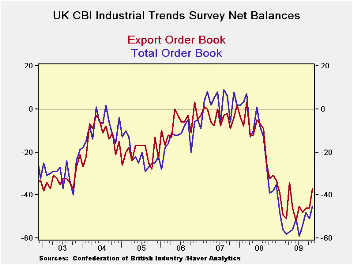

Total orders revived to -45 from -51 a still steep negative reading but a substantial month-to-month gain in November. Export orders, following the pattern of other EU countries, have made even grater progress this month improving to -37 from -46.

Overall orders bottomed in the cycle at -59 in July and the series has only clawed back to -45 by November. This month’s six point gain month to month gain is twice the pace of the rise from the cycle low (approx 3.5 per month). The surge in export orders this month is even more impressive on that score since those orders had only been rising by 3 points per month from their cycle low compared to this month’s jump of nine points.

The outlook for the volume of output has improved rapidly from its cycle low of -48 in March of this year. Its rapid increases came in April, May and in August. In October the outlook index for volume switched to a positive reading and this month it holds that same reading of +4. Although the month to month improvement in the volume outlook index has stagnated this month, the level of the reading staying in positive territory still marks it as a good result.

The survey evidence is that British industry sees itself improving and expects that to continue. Overall orders are showing strong improving profiles and are being spurred substantially by export orders. While orders have a long way to go to become a truly positive reading, the outlook of the British industry survey respondents says they expect it to get there. On balance the survey is a good result.

| UK Industrial volume data CBI Survey | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Reported: | Nov 09 |

Oct 09 |

Sep 09 |

Aug 09 |

Jul 09 |

12MO Avg |

Pcntle | Max | Min | Range |

| Total Orders | -45 | -51 | -48 | -54 | -59 | -51 | 21% | 9 | -59 | 68 |

| Export Orders | -37 | -46 | -46 | -48 | -45 | -43 | 27% | 3 | -52 | 55 |

| Stocks:FinGds | 20 | 10 | 13 | 13 | 20 | 23 | 67% | 31 | -2 | 33 |

| Looking ahead | ||||||||||

| Output Volume:Nxt 3M | 4 | 4 | -2 | -5 | -14 | -28 | 68% | 28 | -48 | 76 |

| Avg Prices 4 Nxt 3m | -5 | -4 | -10 | -17 | -6 | -10 | 28% | 34 | -20 | 54 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief