Global| Jul 19 2019

Global| Jul 19 2019EMU Trade and Current Account Surplus Rise As Trade Flows Ease

Summary

The EMU current account and trade accounts widened as merchandise exports rose and imports contracted. Services account income flows rose to create a larger net inflow while current transfers and outflow item diminished. Both accounts [...]

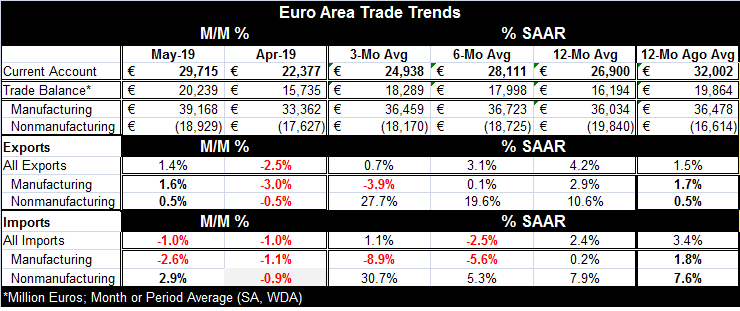

The EMU current account and trade accounts widened as merchandise exports rose and imports contracted. Services account income flows rose to create a larger net inflow while current transfers and outflow item diminished. Both accounts added to the trade surplus to push the current account to an even larger surplus in May.

The EMU current account and trade accounts widened as merchandise exports rose and imports contracted. Services account income flows rose to create a larger net inflow while current transfers and outflow item diminished. Both accounts added to the trade surplus to push the current account to an even larger surplus in May.

The current account and trade surpluses both are smaller over 12 months and six months, but the current surplus is smaller over three months while the trade surplus grows.

Trade flows showed an export rise of 1.4% in May as imports fell by 1.0%. Sequentially exports are slowing from a pace of 4.2% over 12 months to 3.1% over six months to 0.7% over three months. Imports are slowing as well but not sequentially as their 2.4% 12-month pace gives way to a 2.5% decline over six months as the three-month pace rebounds to gain 1.1% which exceeds the six-month pace but is below the 12-month pace.

Flows are divided into manufacturing and nonmanufacturing flows on each side. The manufacturing flows are relatively well behaved while the nonmanufactures are buffeted by commodity price swings and other factors; they are especially impacted by energy prices. For manufactures trade, both exports and imports show sequential slowing. Despite the slowing for both manufactures flows, export growth holds an edge over import growth on each of the three horizons.

Nonmanufactures show the opposite sequential acceleration in progress for exports as imports show the same accelerating trend but not sequentially. The slowing global growth has damped trade flows and brought weakness particularly to the manufacturing sectors of many economies. Today Fitch warned China that its use of debt to try to maintain growth was becoming dangerous. But of course, China would rather risk steps of stimulus than to admit or allow its economy to suffer from U.S. tariffs. Pride comes before the fall so does excess debt. Because of the Maastricht rules, Europe does not fall into this trap. Most EU economics have little or no wiggle room under the Maastricht rules to add debt to support growth given their current economic situations. Italy earned a small variance from this situation.

International rate cuts/domestic realities

Global growth has slowed and central banks that had been reluctant to cut rates have been joining in as the Bank of Indonesia and the Bank of Korea, both long dormant over rate cuts, have instituted cuts this past week. The focal point for all of this is the U.S. where Jay Powell, when testifying last week, talked of the Fed’s commitment to hits its 2% target at a time when that target had been missed persistently. Stimulus would help to hit the target - or at least send the message that the Fed is trying to hit it. Powell has encouraged markets to believe that that is where he is headed, down the path to a rate cut. However, not all data line up behind that notion. After a very weak report, employment gains snapped back in June; likewise, the July Philadelphia manufacturing business outlook survey showed a sharp rebound after a terrible fall in June. Now economic conditions do not seem as needy. Still, as of July 17, the Atlanta Fed’s GDP Now-cast puts Q2 growth at just 1.6%, well below the 3.1% pace that the economy has hit. In discussing the ‘right’ policy, U.S. officials have (oddly) been talking a lot of the needs of the international community and of the lack of fire-power for stimulus in Europe and in Japan.

Global growth challenges

The Fed usually sets aside notions that it is making polices for external events. When the international economy is suddenly a reason for the Fed to move, you know that something is up. The Fed can play Hokey-pokey with any event or concept either choosing to put it in play of to take it out.

Apparently after a long stretch of personal introspection on policy, the Fed is finally picking its head up, seeing the needs of the rest of the world and preparing to do something that might help everyone.

Might...

In the mid-1980s, polices were being implemented on a more coordinated basis as counties tried to manage exchange rates. That ‘experiment’ brought the Plaza Accord and the Louvre Accord, deals named after the locations of their negotiations. The Plaza Accord did succeed (or at least coincide) with the dollar turning lower. But the Louvre Accord did not stop the dollar falling vs. the yen. That accord was supposed to stop the yen at about yen 140/dollar and instead the yen continued to power higher to an exchange rate that peaked around yen 85/dollar. After a while, it became clear that this exchange rate game was not useful although markets loved it because it set up trading opportunities in currencies. Central banks instead decided that each would go home and ‘stick to their own knitting.’

That was then. This is now.

Back to the future

So…they’re back! Not the Poltergeist, but the central bankers meddling in one another’s business. So far, it is just the U.S. that is apparently strongly deciding to base its domestic policy move on international needs. Separately, there is also all that tariff stuff… But the rest of the Fed may not be on this same page; Mr. Powell may find dissent if he continues down this path. Of course, it’s a bit of a ‘road under repair’ that is merging traffic from several different paths: one looks at the international scene, another looks at the U.S. inflation undershoot, and another looks at the U.S. economy finding a good deal of weakness but a mixed bag of indicators overall.

Since Powell began floating this policy trial balloon, markets has been one-upping their expectations’ with some looking or a 50 bp cut. That now seems unlikely given the mixed nature of incoming U.S. data. The overseas data continue weak. And it’s true that foreign central bankers generally have less ammunition than the Fed has. Powell and a research paper by NY Fed President John Williams argued for the need to be bolder and bit pre-emptive when policy operates on the fringes of the zero bound. Fed Vice Chairman Richard Clarida seemed to support those remarks as well. But not all do and it is likely that the next FOMC meeting will produce dissent on the other side of the issue. Mr. Bullard, who dissented at the last meeting, likely will get his rate cut this meeting and he has been clear that he is not looking for - or supporting - a 50bp cut. But many others remain concerned about financial stability and the impact of lower rates on speculation and on potentially unstable borrowing.

The Fed has macro prudential tools it can use to help stabilize markets. So while it is busy cutting rates, maybe it could polish those and begin to use them selectively to fine tune stimulus and yet preserve financial stability. Abroad, there is still a lot of concern about Italian banks that are able to find solace, stability and to mark time in this low rate environment. They remain a ticking time bomb and they are not alone. As helpful as a Federal Reserve rate cut in the U.S. might be, since these monetary effects spread across exchange markets to various national bond markets, the Fed can only do so much. At the end of the day, Fed policy can’t be the frosting on the cake of European policy, but it might make a nice fancy decoration that helps it to look better.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief