Global| Sep 16 2020

Global| Sep 16 2020EMU Surplus Grows As Exports Rise Strongly

Summary

Trade flows are still depressed compared to what they previously were doing. Year-over-year exports and imports are contracting at about a 10% or so pace while previous to the recession export and import growth rates had been in a [...]

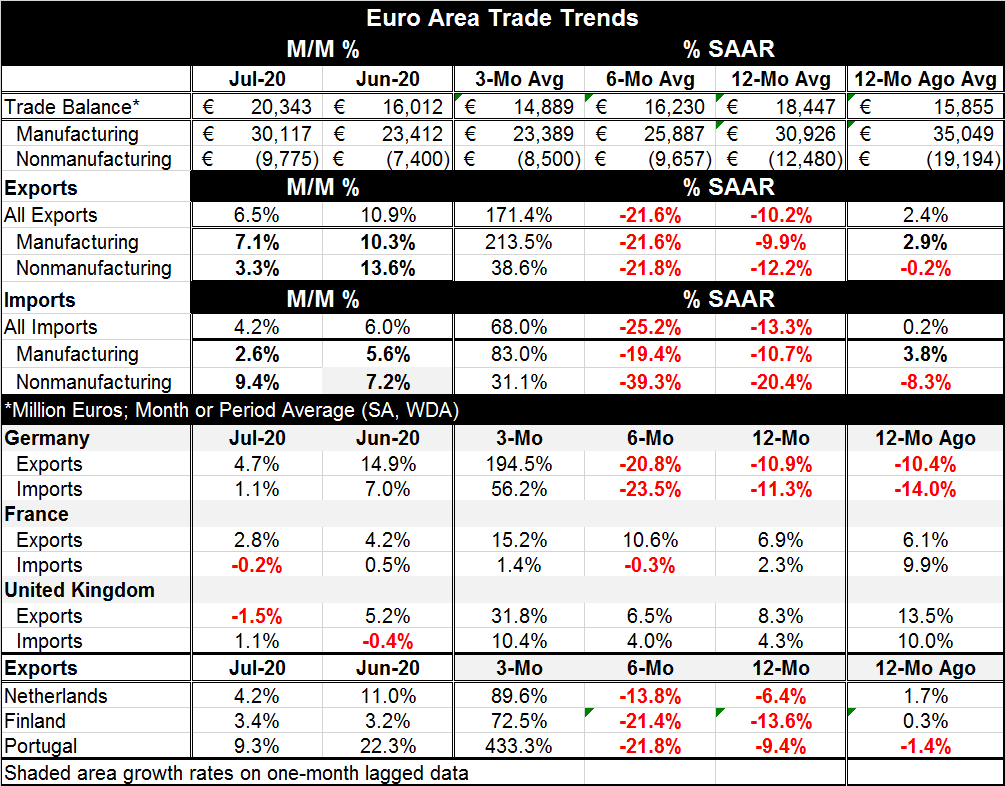

Trade flows are still depressed compared to what they previously were doing. Year-over-year exports and imports are contracting at about a 10% or so pace while previous to the recession export and import growth rates had been in a range of 5% to 10%. However, the balance between exports and imports does appear to have been restored as it shows a higher surplus on the month of 20.34 billion euros up from 16.01 billion euros in June. The 12-month average for the surplus is 18.45 billion euros.

Trade flows are still depressed compared to what they previously were doing. Year-over-year exports and imports are contracting at about a 10% or so pace while previous to the recession export and import growth rates had been in a range of 5% to 10%. However, the balance between exports and imports does appear to have been restored as it shows a higher surplus on the month of 20.34 billion euros up from 16.01 billion euros in June. The 12-month average for the surplus is 18.45 billion euros.

Exports rose by 6.5% in July compared to a 4.2% rise in imports. In June, exports grew by 10.9% while imports rose by 6% creating an even larger export import growth rate gap in June than in July.

Exports of manufactures are outstripping growth for imports of manufactures for three months running. But export flows had been much harder hit in April. While exports of manufactures are decisively faster-growing over three months (213.5% annual rate compared to an 83% annual rate for imports), over six months and 12 months their growth rates are nearly the same.

The growth rates of nonmanufactures have been variable in their impact of exports and imports, but growth has mostly favored exports. Imports of nonmanufactures surged at nearly three times the growth rate of exports in July after lagging export growth nearly two to one in June. Over three months, nonmanufactures saw exports and imports both growing with exports a bit faster. Over six months and 12 months, both exports and imports of nonmanufactures are plunging with imports weaker than exports.

Trade date for Germany, France and the United Kingdom show some striking consistencies in July, in June as well as over the last three months. Among the nine pairs of growth rates (exports to imports) on these segments, exports are outperforming imports consistently in eight of the nine comparisons (U.K. trade flows in July are the only exception). However, over six months and 12 months, German flows imploded sharply while French and U.K. exports both continued to expand and imports also show growth on those two time periods except that over six months French imports show an exceedingly small decline.

We also have export flows for the Netherlands, Finland and Portugal. They all follow the overall EMU and German pattern rather the U.K.-French patterns with flows declining over 12 months declining even faster over six months then growing at a sharp, strong pace over the last three months.

Despite the EMU/German/Dutch/Finish/Portuguese trends that show exports up sharply over the last three months, the Baltic dry index is not showing much of a revival in global trade overall. In part what we are observing in Europe is not so much a pick-up in trade as a claw-back of growth lost as trade flows do not so much 'grow' and they get back to ground that has been lost. This is staving off the further loss of shipping volume.

Despite the EMU/German/Dutch/Finish/Portuguese trends that show exports up sharply over the last three months, the Baltic dry index is not showing much of a revival in global trade overall. In part what we are observing in Europe is not so much a pick-up in trade as a claw-back of growth lost as trade flows do not so much 'grow' and they get back to ground that has been lost. This is staving off the further loss of shipping volume.

Today, however, the OECD raised its outlook for growth in 2020. The easing of coronavirus restrictions is going faster than it had assumed; it looks for the global economy to shrink this year by 4.5% instead of 6%. Separately the German finance minister, Olaf Scholz, said that the European economy was recovering faster than what many had feared. However, he urged continued support for growth for companies and for consumers. New Zealand added its voice to the chorus for greater optimism as it now looks for its economy to shrink by 'only' 16% in the June quarter instead of the 23.5% fall it had estimated previously. There is some optimism afoot. But there is no new optimism on the recently mooted bipartisan $1.5 trillion support package in the U.S. Moreover, today's consumer spending news in the U.S. was decidedly weaker than expected and weaker than recent past trends had been. Apparently there are two sides to every 'story.' And there is still the brewing snit between the U.K. and EU as well as ongoing post Brexit trade negotiations there that the recent U.K. actions may have just torpedoed. Growth news continues to have its pluses and its minuses. On balance, this was still a 'plus' day.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief