Global| May 06 2015

Global| May 06 2015EMU Services Slip a Bit in April

Summary

The services sector has been carrying the European recovery, but that sector backed off with its PMI index edging lower to 54.1 in April from 54.2 in March. Still, the services PMI has a queue standing in the 76.2 percentile, much [...]

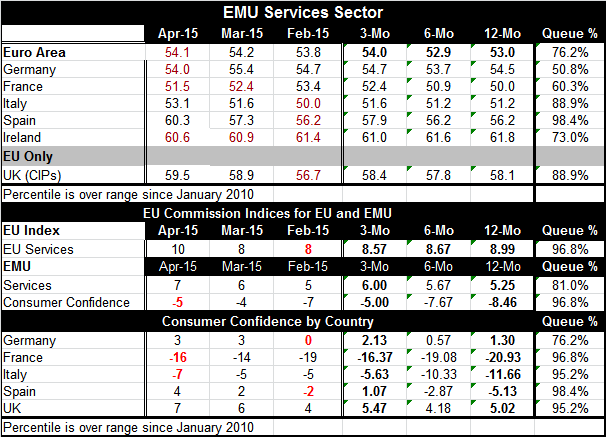

The services sector has been carrying the European recovery, but that sector backed off with its PMI index edging lower to 54.1 in April from 54.2 in March. Still, the services PMI has a queue standing in the 76.2 percentile, much higher than the manufacturing sector's 59.4 percentile standing. Services are still leading Europe ahead and by a large margin.

The services sector has been carrying the European recovery, but that sector backed off with its PMI index edging lower to 54.1 in April from 54.2 in March. Still, the services PMI has a queue standing in the 76.2 percentile, much higher than the manufacturing sector's 59.4 percentile standing. Services are still leading Europe ahead and by a large margin.

But in Germany the services sector is much weaker, stuck in its 50.8 percentile. In France it stands in the 60.3 percentile. Italy and Spain have much stronger relative standings with Italy in the 88.9 percentile and Spain in the 98.4 percentile. The U.K., a non-common currency country, has its services sector strong in its 88.9 percentile.

Manufacturing is in a slump because of weak global demand and intense competition out of Asia. Since the manufacturing sector is not a top employer, its lagging performance has not impaired consumer confidence. Note that apart from Germany, France, Italy and Spain each have consumer confidence standings in the mid-90th percentile or higher. Consumers are feeling much better despite lagging manufacturing. And consumer attitudes are ranked higher than either the manufacturing or services sectors in isolation (except in Spain where the rankings are identical).

These same trends are operative in the U.S. where manufacturing is slipping and the services sector is still advancing. In the case of the U.S., such sectoral divergence is very large and unusual. But in this global environment, the fact of the matter is that when consumers revive and begin to buy goods again the developing (or less advanced) economies have the cheapest manufacturing platform in town. That means that rising demand in the advanced economics will more quickly lead to some revival in the less developed world and that the local multiplier effects from those sorts of demand pick-ups will muted in the advanced economics. This will make getting sustained growth in gear more difficult.

In the EMU, this adverse effect is being blunted by past euro weakness which partly has restored European competitiveness relative to Asia. But the euro has been rallying a bit recently. In the U.S., the damped-multiplier effect is being accentuated by the overly strong dollar.

The current world trade make up that it is still all-too-much North-South (exports from less advanced economies to advanced economies) is undermining the attempt of the more advanced economics to get growth in gear by leaning heavily on monetary stimulus. The recent sharp widening of the U.S. trade gap (albeit after a surprisingly small gap the month before) is an example of this. With imports picking up, the U.S. will have to drive domestic growth extra hard to have anything left to go to the bottom line of GDP. Of course, the growth of spending in the services sector is more likely to stay at home. So far the U.S. services sector, like its counterpart in Europe, is staying strong even in the face of manufacturing sector weakness.

So the revival in services is a revival in growth that hits the bottom line of GDP. Europe is being pulled into recovery by its services sector and it has been that way for over a year. But manufacturing is still important and to make this recovery stable and lasting, the manufacturing sector has to join up. When will that happen?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief