Global| Jan 08 2018

Global| Jan 08 2018EMU Retailing Bounces Back

Summary

Retail sales across the EMU and in other early reporting EMU and EU nations largely show a rebound or accelerating in November. The EMU and the seven countries in the table show declines in October in six of these eight jurisdictions. [...]

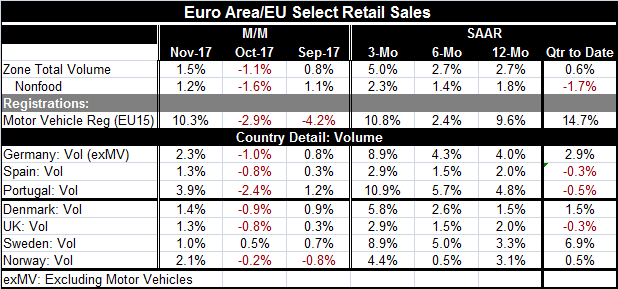

Retail sales across the EMU and in other early reporting EMU and EU nations largely show a rebound or accelerating in November. The EMU and the seven countries in the table show declines in October in six of these eight jurisdictions. All show a rebound from a decline or acceleration in sales in November compared to October.

Retail sales across the EMU and in other early reporting EMU and EU nations largely show a rebound or accelerating in November. The EMU and the seven countries in the table show declines in October in six of these eight jurisdictions. All show a rebound from a decline or acceleration in sales in November compared to October.

Sales also show acceleration in seven of eight jurisdictions over three months compared to six months. All eight jurisdictions show stronger growth over three months (annualized) than over 12 months.

Despite these rosy calculations, sales are not actually all that strong in the quarter. For the EMU in the quarter-to-date (two months into the final quarter of 2017), sales are up at only a 0.6% annual rate for their Q3 level. Nonfood sales actually are declining in the fourth quarter-to-date for the EMU overall. Spain, Portugal and the U.K. also show sales falling in the quarter-to-date calculation. Sales on this basis are strongest in Sweden at a 6.9% annual rate followed by Germany at 2.9% with relatively weak growth rates of 1.5% in Denmark and 0.5% in Norway.

The chart actually gives a good sense of sales having fallen off sharply in October and despite a rebound in November demonstrating a generalized loss in momentum.

Still, news for EMU continues to be more upbeat than not...

In December, the euro area confidence index, also released today, rose more than expected to 116.0 from 114.6 in November. This brings the index to its highest point since October 2000, well before the onset of the financial crisis and global recession. Also the Sentix investor confidence index gained to 32.9 in January, rising from 31.1 in December and beating expectations for a lesser gain. Assessments of conditions in the EMU are quite solid and still strengthening. The fly in the ointment for today's data was the reported decline in German orders in November which fell by 0.4% after a 0.7% gain in October on drops in both domestic and foreign orders. Still, for Germany this was the first drop in orders in four months; it can hardly be construed as bad news given the fluctuations in order data overall. German real orders are still growing at a 6.5% annualized rate over six months and by 8.7% over 12 months. Foreign orders are still growing faster over three months than over 12 months. It is German domestic orders that have stalled rising at just a 0.4% annual rate over three months and a 0.2% annual rate over six months but still gaining 6.2% over 12 months. On the whole, the German order data may be a little spotty, but they do not seem to be anything to worry about at this point despite some minor decelerations. Year-on-year domestic and foreign real orders are still both on rising trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief