Global| Oct 03 2014

Global| Oct 03 2014EMU Retail Sales Perk Up

Summary

Euro area retail sales in August snapped back sharply, rising by 1.2% after falling by 0.4% in July. The three-month performances boosted the growth rate to 4.9%, up from 0.6% over six months and 0.6% over 12 months. The growth of [...]

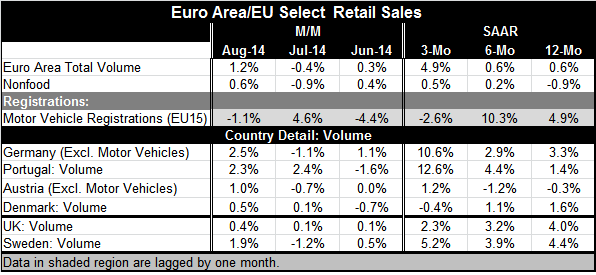

Euro area retail sales in August snapped back sharply, rising by 1.2% after falling by 0.4% in July. The three-month performances boosted the growth rate to 4.9%, up from 0.6% over six months and 0.6% over 12 months. The growth of nonfood items stepped back up in August; its trends, the sequential growth rates, show some acceleration as well. Motor vehicle registrations are quite volatile and fell by 1.1% in August after a 4.6% increase in July and a 4.4% decline in June. The balance of these effects leaves a negative three-month growth rate -2.6%, down from 10.3% over six months and 4.9% year-over-year. Still, because of volatility, it's hard to conclude that motor vehicle registrations are slipping with any degree of certainty.

Euro area retail sales in August snapped back sharply, rising by 1.2% after falling by 0.4% in July. The three-month performances boosted the growth rate to 4.9%, up from 0.6% over six months and 0.6% over 12 months. The growth of nonfood items stepped back up in August; its trends, the sequential growth rates, show some acceleration as well. Motor vehicle registrations are quite volatile and fell by 1.1% in August after a 4.6% increase in July and a 4.4% decline in June. The balance of these effects leaves a negative three-month growth rate -2.6%, down from 10.3% over six months and 4.9% year-over-year. Still, because of volatility, it's hard to conclude that motor vehicle registrations are slipping with any degree of certainty.

Retail sales volume figures across some selected European Union and European Monetary Union members, shows us gains for all those countries listed in the table in August. Germany and Portugal show double-digit gains and reveal that sales acceleration is in place in both countries. Sweden's growth, at 5.2% over three months, is also part of an ongoing acceleration. Austria's 1.2% three-month growth rate is also better than its six month and 12-month growth rates, but the pattern is not as reliable as for other countries showing acceleration. In the U.K., three-month growth is at 2.3%, part of a gradual slowdown from 4% over 12 months to 3.2% over six months to 2.3% over three months. In Denmark, the negative growth of 0.4% over three months is also part of an ongoing slowdown from 12 months to six months to three months. However, Denmark also has sales gains back-to-back in July and August that for the moment are being swamped by a 0.7% drop in June; so its deteriorating pattern may not be set in stone.

Also released today were service sector PMI metrics which allow for the completion of the overall PMI metrics for the euro area and its members that report such data. For the EMU as a whole, the composite PMI slipped to 52.0 in September from 52.5 in August. For Germany, the PMI improved to 54.1 from 53.7. For France, the PMI slipped further to 48.4 from 49.5. For Italy, the PMI slipped to 49.5 from 49.9. Spain's PMI metric declined to 55.3 from 56.9. Among the four largest EMU countries, two of them, France and Italy, show contraction in their private sectors; the other two, Germany and Spain, show continued growth.

Today's data are somewhat surprising in that retail sales continue to rebound against the background of deteriorating private sector growth. We have seen consumer confidence hold to reasonably firm levels in many European countries, indicating that consumers have not been totally spooked by the ongoing question marks about growth. There had been some tendency to see growth weaken ahead of the development of the Ukraine crisis. However, since the Ukraine situation has unfolded, and since sanctions have been placed on Russia, and since Russia has taken some counter moves and continued to meddle in the affairs of Ukraine (even after a ceasefire agreement was signed), Europe's economic behavior and its outlook has been more muddled.

The one thing that could change consumer attitudes for the worse is the growing evidence that Russian shipments of energy have not been up to the demands of the European countries whose markets it serves. So far, there have been no statements by Russia that it is restricting any kind of shipments. But the facts on the matter are that actual deliveries are falling short of where they should be for this time of year. Should the situation continue to worsen, we might find European consumers much more affected and concerned about economic well-being. For the moment, there is also a bit of a game of musical chairs being played by countries that have pipelines flowing through them, as some are diverting supplies destined for other locations in order to make up for delivery shortfalls that they themselves have experienced. This sort of thing, of course, could wind up pitting one European country against another. And the breakdown in European unity is exactly what the Russians would like to see happen. All of this is still speculative, but it's based on a clear set of economic facts to date.

Although the facts we cite are totally due to supply and, apparently, the willingness of the supplier (in this case Russia) to send the right volumes down the pipeline, there is a contrary trend in the works as Saudi Arabia is threatening to pump more oil in order to keep from losing its market share.

Other oil-producing countries have continued to keep their output levels high, but the Saudis are no longer willing to be the flexible partner who cuts back their output in order to keep oil prices where they have been. The Saudis want to keep their share of the oil market and now they're willing to pump oil to the point of depressing oil prices in order to create discipline across the rest of the noncomplying OPEC members. While in past situations these circumstances would be viewed as good news, with central banks trying to fight off deflation, the potential for oil prices to drop sharply near-term could tend to exacerbate that very trend and to confuse central bank policy.

The policy situation has certainly turned into a difficult jumble. We can hope that European consumers continue to spend in a manner that's reflected in their current retail sales report. We also hope that the industrial slippage and service sector weakness manifest in the PMI indices prove to be temporary and that Europe's reaction to the Ukraine crisis shifts and allows its economies to stabilize. Oddly, the Russian service sector showed some improvement in September despite everything that's going on with Russia. My reaction to this is to doubt the veracity of that survey. But as a rule I think it's a bad idea to discard economic data points that you don't like. In this case, I do think there's a reason. On the political front, Russia has done nothing to cause us to think that we can believe anything that it says or about what it is doing. I don't think we should assume that that disconnect doesn't extend to its economic reports.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief