Global| Nov 04 2014

Global| Nov 04 2014EMU PPI Ticks Up, Is It Real?

Summary

The euro area PPI picked up in September, rising by 0.1% after a 0.2% August decline. While this may seem to suggest a turning point indicating that the downward pressure has abated, that conclusion is premature. One month does not [...]

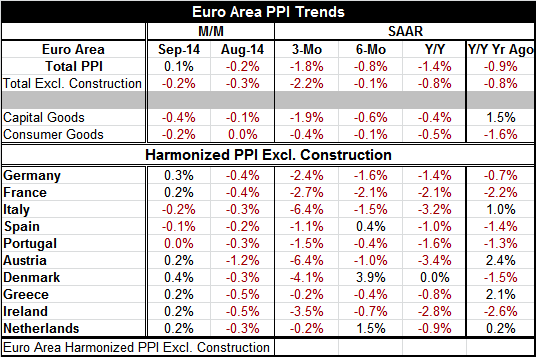

The euro area PPI picked up in September, rising by 0.1% after a 0.2% August decline. While this may seem to suggest a turning point indicating that the downward pressure has abated, that conclusion is premature. One month does not assure a change in trend. Longer terms trends are still heading lower. PPI trends by member countries are still substantially tilted lower. Oil prices are still sliding. Growth is weak and the outlook for growth in the euro area has been cut. All of these factors argue that the PPI is not really turning higher yet.

The euro area PPI picked up in September, rising by 0.1% after a 0.2% August decline. While this may seem to suggest a turning point indicating that the downward pressure has abated, that conclusion is premature. One month does not assure a change in trend. Longer terms trends are still heading lower. PPI trends by member countries are still substantially tilted lower. Oil prices are still sliding. Growth is weak and the outlook for growth in the euro area has been cut. All of these factors argue that the PPI is not really turning higher yet.

PPI Overall Trends

The PPI over three months is falling at a 1.8% annual rate, a steeper drop than its 1.4% decline year-over-year. The PPI excluding construction continues to fall, dropping by 0.2% in September after a 0.3% decline in August. Over three months the ex-construction PPI is falling at a 2.2% annual rate, compared to a 0.8% drop over 12 months.

Sector Trends

Capital goods prices are accelerating their drop, falling at a 1.9% pace over three months, 0.6% over six months and 0.4% year-over-year. Capital goods stepped up the drop in September, falling by 0.4% after a 0.1% August decline. Consumer goods prices fell by 0.2% in September after being flat in August; the sequential growth rates show a steady menu of declines without much clue about the trend for consumer prices.

Member Trends

Looking at a selection of member nations, we see this group of ten has only three members with PPI declines in September compared to all of them with declines in August. Over three months each of these countries has a decline in its PPI. Only Greece and the Netherlands have annual rate declines over three months that are less than 1%. Only Greece has the three-month rate of decline not accelerating compared to the pace of the six-month rate of decline. In all other countries, the deceleration of prices steps up from three months to six months. In all cases except Greece and the Netherlands, the three-month pace is also lower than the year-over-year pace, implying ongoing deflationary forces from producer prices across most member nations.

Environment and Oil Prices

Getting beyond the PPI trends, we continue to have weak economic figures reported across the euro area. In addition, oil prices on world markets continue to fall with oil prices opening today's sessions below $78 per barrel. Saudi Arabia has increased its discounts to the United States. Oil prices and market indicators are showing no indication that prices are going to stick around $80 per barrel. Of course, if oil prices continue to fall, producer prices are likely to continue to fall as well. And there are likely to be knock-on effects to the consumer prices that the ECB targets.

Weakness and a Weaker Outlook

In addition to the background of weak oil prices, weak global growth, weak global commodity prices, generally, we have the European Commission today cutting its outlook for growth for the euro area to below 1% for the year. The Commission cited a complicated array of factors but blamed ongoing weakness and outlook modification on stalled recoveries in France and Italy.

Geopolitics Erode

In addition, the geopolitical situation remains tender with the eastern provinces in Ukraine having elected officials sympathetic to Russia, in defiance of a previous agreement with Ukraine. This has heated up tensions in the region again. The combination of heightened geopolitical tensions and a reduced outlook by the EU Commission is a double dose of bad news.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief