Global| Mar 04 2014

Global| Mar 04 2014EMU PPI Is Softer Faster-Is That Good or Bad News in This Troubled Time?

Summary

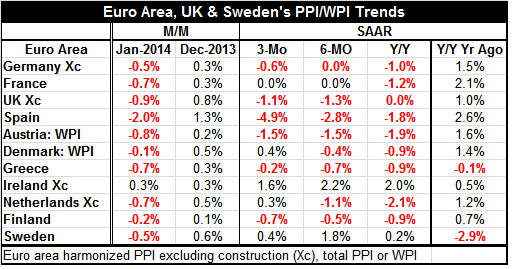

EMU producer prices continue to crash and burn. While the European Central Bank has its focus on consumer prices using the Harmonized Index of Consumer Prices (HICP), the ongoing drop in PPI prices will give the ECB plenty of [...]

EMU producer prices continue to crash and burn. While the European Central Bank has its focus on consumer prices using the Harmonized Index of Consumer Prices (HICP), the ongoing drop in PPI prices will give the ECB plenty of confidence that inflation is well under control in the euro area. But is it that confidence that the ECB needs or does it need some different reassurance?

EMU producer prices continue to crash and burn. While the European Central Bank has its focus on consumer prices using the Harmonized Index of Consumer Prices (HICP), the ongoing drop in PPI prices will give the ECB plenty of confidence that inflation is well under control in the euro area. But is it that confidence that the ECB needs or does it need some different reassurance?

While the ECB is often portrayed as a single-mandate central bank, it has been very clear that under the direction of Mario Draghi it has had a much broader focus to the delight/consternation of its various members (e.g. do what's necessary). At times, the Germans have been quite livid over the ECB's policy tacks and its justification under the treaty mandate. But in retrospect it is hard to fault the various policy maneuvers of the bank under Draghi as the euro area continues to flounder and struggle even as it shifts to a regime of growth. We are reminded that growth is not simply a binary state and that it has many gradations. An oft-used analogy is that while Europe may have achieved lift off, it has not yet fully achieved escape velocity. Can it escape the pull of the gravity of its past lethargic momentum? What about the new headwinds of geopolitical change?

Growth in the euro area is a weighted average affair. While it `only makes sense' to give Germany, the largest economy in the EMU, the largest weight in the euro area, Europe still has what the United States would see as a Senate/House-of-Representatives problem. The euro area is in one sense a single zone, but its politics has not been thoroughly shaken and stirred together. The problem is that euro zone data still are reported on a national jurisdictional basis, but policy is made solely on a weighted-borderless-economic basis. For example, the ECB shoots at an inflation target made up of the weighted HICP without regard to the dispersion of inflation within the euro area. This is a policy admixture sure to create strife - and it has.

Basically, there is no formal vehicle for the smaller European member countries to have their say except through their vote on the ECB board (and of course through the EU Commission on non-monetary matters). Since there is no formal weight attached to policy dispersion, there is little ground to stand on in ECB discussions for smaller nations with problems that differ from the weighted average for the EMU as a whole. EMU policy is aggregate-data focused. Because small-country economic weighting is so low, the ECB can (and has!) hit its (inflation-only) targets even with quite a number of smaller economies in severe and persistent violation of the ECB standards. were those standards to be applied on a country by country basis (which they are not). Had the ECB/Europe paid attention to such divergence in the past the crisis may not have occurred.

With Mario Draghi as ECB head, there has been much more attention to the needs of the peripheral nations than there was with a German banker as the ECB's head. While a German was in line to head the ECB this round, the main candidate stepped aside because he could see the pressure mounting and he wanted no part of being head of the ECB as the strict standards that would have been applied at the Bundesbank were set to be eroded or pressured in the conduct of policy by the ECB.

The Bundesbank has continued to express its opposition to some of the policies of Mario Draghi which seem to have stretched the ECB mandate. But in the end weakness not inflation has remained the main EMU problem. And no German can point to any bad repercussion from the innovative Draghi policies save the ever-lurking concern that `moral hazard' might emerge as an issue in the future. Still, it would have been hard for the ECB to ignore the real world problems of the euro area and one can only wonder how different the world might have been had Draghi not swerved. Would there still be a euro area?

That musing brings us back to the circumstance of the current PPI which continues to be so weak. Obviously, the ECB has little mandate to swerve its policy even with the PPI falling on a broad-based front across the euro area and most horizons. The PPI is more volatile and will undergo more extreme movement than the CPI (HICP); that is one reason why the ECB really is focused upon the HICP. Still, pronounced weakness on any of these key measures is also a proxy for economic strength albeit that the PPI will be tossed around more than the CPI by commodity price movements. We know we can have stagflation (weak growth with high inflation) and there have been periods of robust growth with low inflation (nirvana/true equilibrium), but more generally low inflation and low growth as a pairing reinforce the signal of weakness in the economy.

I do not propose that the ECB become more proactive- that is not its place. But I do propose that market observers and investors absorb the sense of helplessness that the ECB will have under these circumstances unless a crisis develops and Draghi thinks, once again, he can twist the rules.

Simple stagnation will not do it. While growth is turning the corner to positive numbers in Europe, this corner has a severe angle and the road surface has a slippery surface with no guard-rail and a steep drop off the shoulder. The risks are still in full tilt for the EMU. Low inflation, a usual comfort for the bank, no longer is so comforting. Ongoing weakness in prices will add to the atmosphere of instability as political unrest is now encroaching on Europe's very borders - a Europe that is very dependent on energy shipments from Russia through the currently unstable Ukraine. If anyone thinks that Europe's recovery will continue being affected by these developments, I wish them well, but bid him/her to buy some insurance for that view against the potential for the future to be quite different.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.