Global| Aug 02 2018

Global| Aug 02 2018EMU PPI Is Off to the Races...Chased Exclusively by Oil

Summary

On the face of it, the PPI situation in the EMU is looking rather grim. Inflation is at 3.6% year-on-year and over six month. Skipping the two highest and two lowest inflation rates in the table of 13 members, inflation ranges from a [...]

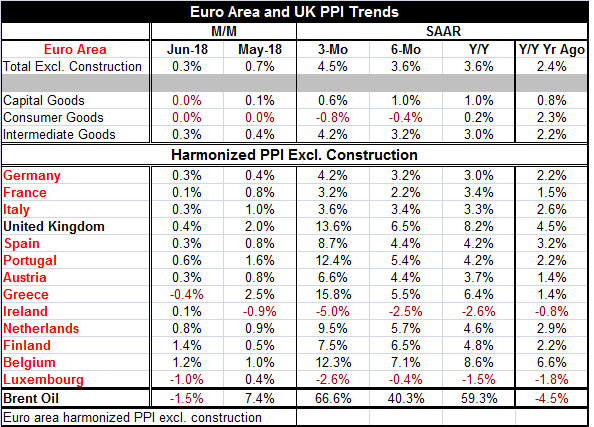

On the face of it, the PPI situation in the EMU is looking rather grim. Inflation is at 3.6% year-on-year and over six month. Skipping the two highest and two lowest inflation rates in the table of 13 members, inflation ranges from a low of 3.2% in Germany over six months to a high of 12.4% in Portugal over three months. Year-on-year on that same method, Germany has the inflation low at 3% and Greece has the highest on this ‘trimmed basis’ at 6.4%.

On the face of it, the PPI situation in the EMU is looking rather grim. Inflation is at 3.6% year-on-year and over six month. Skipping the two highest and two lowest inflation rates in the table of 13 members, inflation ranges from a low of 3.2% in Germany over six months to a high of 12.4% in Portugal over three months. Year-on-year on that same method, Germany has the inflation low at 3% and Greece has the highest on this ‘trimmed basis’ at 6.4%.

Not only is inflation high but it is rising. Inflation accelerated in 11 of 13 members from six-month to three-month. Inflation accelerated in 9 of 13 members from 12-month to six-month. Inflation also accelerated in 10 of 13 members, year over 12 months, comparing it to the pace of PPI inflation one year ago. These are clear signs of inflation acceleration.

And we know why inflation is accelerating; it is oil. Brent oil prices are up by 59.3% year-over-year and that compares to them falling by 4.5% over 12 months one year ago. Over six months, the pace of the Brent rise is 40.3%. Over three months, the pace is back up to 66.6%. So it’s no wonder that headline inflation is increasing for all these countries on all these horizons. Oil prices have just been hammering away as OPEC and Russia colluded to raise prices by cutting back output. But now that is over and more U.S. production is coming on stream. OPEC is setting a more ambitious production schedule, itself. After rising by 7.4% in May, Brent prices fell by 1.5% in June.

If we look at sector trends, we begin to get a clear picture of what is driving PPI prices and the answer is a loud and clear; OIL! Inflation is wholly- completely and artifact of intermediate goods where prices are driven by commodities and especially oil. Intermediate goods prices are up 3% year-on-year and at a 3.2% pace over six months. They are up at a 4.2% annual rate over three months.

In marked contrast, capital goods prices are up by 1% over 12 months, up at a 1% pace over six months and finally up at a 0.6% annual rate over three months. There is disinflation in the capital goods sector.

Consumer goods prices are up by only 0.2% over 12 months and falling at a 0.4% pace over six months; they are falling even faster at a 0.8% annual rate over three months. There is disinflation for consumer prices as well.

So the headline is being pushed around by oil, but capital goods and consumer goods prices remain subdued. The ECB does not target PPI prices, but these results should still clam nerves at the ECB. The headline is really not very descriptive on what is going on with pricing in the euro-economy. Headline PPI price gains are mostly the effect of oil prices, prices which are now starting to settle back down.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief