Global| Mar 03 2014

Global| Mar 03 2014EMU PMIs Back-off: Worried?

Summary

The peculiar case of the EMU slowdown: Just as everyone has begun to agree that the European Monetary Union (EMU) is in a state of recovery, that recovery has begun to downshift. In Q4 much of the euro area emerged from a long, [...]

The peculiar case of the EMU slowdown:

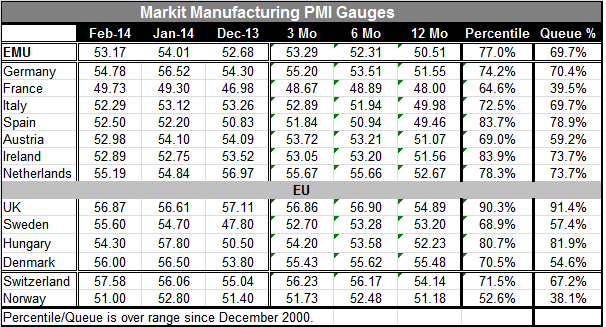

Just as everyone has begun to agree that the European Monetary Union (EMU) is in a state of recovery, that recovery has begun to downshift. In Q4 much of the euro area emerged from a long, ongoing recession. But in February the overall EMU metric for manufacturing from Markit fell back to 53.17 from 54.01 in January. Germany slipped in a noticeable way, dropping from a reading of 56.52 in January to 54.78 in February. Of the countries in the table, Germany, Italy and Austria backtracked.

The peculiar case of the EMU slowdown:

Just as everyone has begun to agree that the European Monetary Union (EMU) is in a state of recovery, that recovery has begun to downshift. In Q4 much of the euro area emerged from a long, ongoing recession. But in February the overall EMU metric for manufacturing from Markit fell back to 53.17 from 54.01 in January. Germany slipped in a noticeable way, dropping from a reading of 56.52 in January to 54.78 in February. Of the countries in the table, Germany, Italy and Austria backtracked.

Over three months, only France and Ireland have lower gauges than they did over six months, although the Netherlands is close to being in the same boat. All the EMU members in the table have better readings over three months than they have over 12 months; that also enhances the view that the setback in February was temporary.

The standing of the various PMI metrics in their historic ranges also adds to the notion that something good is in train. For all of EMU, the manufacturing PMI metric stands in the 69th percentile of its historic queue. While that is not a strong reading, the top 30th percentile is certainly a position that stands for growth, rather than for contraction.

Spain's manufacturing PMI stands in the 78th percentile of its historic queue. Ireland and the Netherlands stand in their respective 73rd percentiles. Germany stands in its 70th percentile. Close behind is Italy in its 69th percentile, despite its ongoing issues. Austria is sitting in its 59th percentile and France is really behind, standing in the 39th percentile of its historic queue. And these of course are only some of the EMU members and we already find a good deal of variability.

Among the non-EMU countries in the table, the UK and Hungary are particularly strong. But the rest of the non-EMU countries are, for the most part, much weaker than the run-of-the-mill EMU member. Four non-EMU members show slippage in their 3-month PMIs compared to six months and several others are barely higher. But compared to 12-month values, two countries, Sweden and Denmark, have weaker readings in the last 3-months. Thus, the euro area not only is struggling itself, but is surrounded by countries that themselves are struggling.

Manufacturing is not the whole of the economy, but it is a sector that has consistently been pushing ahead. Now we see evidence of some waffling and we see come splits developing among various European nations, both EMU members and not EMU members.

While the broad comparisons and the outright ranking of the topical EMU PMIs suggest that recovery is indeed in train, there is also clear contrary evidence of nagging problems that keep the engine missing rather than running smoothly. And this, of course, remains a threat to ongoing growth. For now Europe is on the growth path, but there are clear bumps in the road and obvious unevenness within and around the EMU community itself, and these irregularities pose threats to continued growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.