Global| Mar 24 2017

Global| Mar 24 2017EMU PMIs Are Off to the Races...Farewell Mediocrity?

Summary

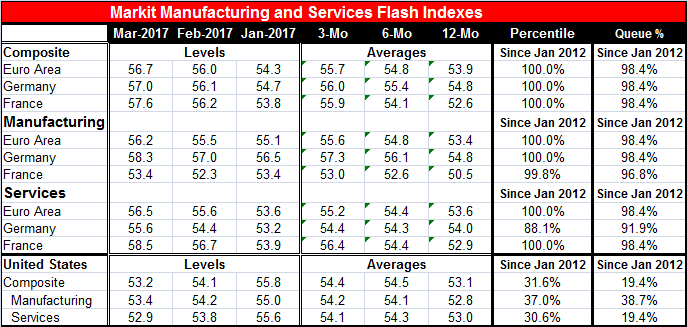

The PMI rankings for the manufacturing and service sector PMIs in the EMU are suddenly off the chart. The queue rankings mark most of this month's readings as this strong or stronger only about 1.6% of the time (since January 2012); [...]

The PMI rankings for the manufacturing and service sector PMIs in the EMU are suddenly off the chart. The queue rankings mark most of this month's readings as this strong or stronger only about 1.6% of the time (since January 2012); the percentile of range standing puts them at the 100th percentile marking these as the strongest readings on this period. The minor exceptions are the French manufacturing PMI that is not quite at its peak but almost, and the German services sector that has been stronger and peaked in May 2014.

The PMI rankings for the manufacturing and service sector PMIs in the EMU are suddenly off the chart. The queue rankings mark most of this month's readings as this strong or stronger only about 1.6% of the time (since January 2012); the percentile of range standing puts them at the 100th percentile marking these as the strongest readings on this period. The minor exceptions are the French manufacturing PMI that is not quite at its peak but almost, and the German services sector that has been stronger and peaked in May 2014.

What's my line?

Nit picking aside, these are extremely strong readings and rankings on this timeline. But of course, it is not a very demanding timeline. On the other hand, it is our timeline and the point is that, compared to where the PMIs have been over the past five years, they are now much stronger.

Strongly up relative to a legacy of weakness

On this last five-plus year timeline, the EMU composite reading averages only 51.5 while manufacturing averaged a reading of 50.6 and services averaged a reading of 51.5. These are a weak cluster of readings, all quite close to the boom-bust value of 50 for diffusion.

The U.S. vs. Europe...different strokes for different folks?

If we compare the EMU country level and overall standings to the U.S., we find that the U.S. composite PMI is 3.5 points weaker than the EMU reading in March. Manufacturing is 2.8 diffusion points weaker and services are 3.6 points weaker than the EMU services reading. However, in January the U.S. raw diffusion readings were generally stronger than for the EMU (with a one-tick exception for manufacturing). Over the past two months, Europe is moving strongly higher and the U.S. has been engaged in a similar degree of change but in the opposite direction widening the gap considerably between Europe and the U.S. and putting them on diverging paths as well. The premium of the EMU service sector diffusion reading over the U.S. reading is the largest of this five-plus year period.

The fork in the road...

Perhaps it is the U.S. where the path is of more uncertainly. But that is only because there is a separate diverging ISM survey for manufacturing and nonmanufacturing (the latter of which lumps mining and housing in with services forming a catch-all nonmanufacturing sector that helps to muddy comparisons between the Markit and ISM surveys). Still, the ISM (through February, and there is no ISM 'flash') is showing that both sectors are weaker in the Markit framework than in the ISM framework. The Markit manufacturing PMI can explain only about 45% of the variance in the manufacturing ISM and it can explain only 22% of the variance in the nonmanufacturing PMI. As result of these relatively poor manufacturing and nonmanufacturing trackings, we are not able to say with confidence what is going on in the U.S., although U.S. regional surveys (which are not comprehensive) have also been on the stronger side rather than on the weaker side at least for manufacturing.

Europe gets ready for change

The message from the metrics for Europe is relatively upbeat. But the weakness hinted at in the U.S. is a reason for caution since the U.S. economy is so large and it tends to be the bellwether. The U.S. financial markets have been upbeat (until very recently at least). The Fed in the U.S. has put two rate hikes together in the span of three months, making tightening look more like a policy than a one-off event. In the EMU, many central bank members are still talking about how it is too soon to abandon QE. In the U.K., the BOE is biding its time with inflation it views as excessive but also temporary on the back of rising oil prices and falling sterling. To be sure, there are market cross currents out there and a possibility that policies are getting ready to shift more decisively in the near, if not immediate, future.

Divergence makes economic impact harder to discern

While signs of greater strength are becoming more common, there is no consistent acceleration and the knock on effects to core inflation and wages are still quite muted. U.S., German and U.K. unemployment rates are quite low, but for much of the rest of Europe, unemployment rates are still above their median values struck since the EMU was formed. Fitch today issued a warning about China's reforms, calling them more likely to make its imbalances worse in the short run. Japan's manufacturing PMI backtracked in March. There have been monthly divergences between the U.S. and EMU manufacturing gauges in terms of them going in opposite directions. The longest such string of U.S.-EMU divergences played out over a period of nine months. But that included diverges of different types and direction; not all of them went in one direction. The two-month divergence we now have is the longest string of diverge with the exact same sort of divergence for two months in a row between the U.S. and EMU (i.e. U.S. weaker and Europe stronger) in the last five-plus years.

The real global scene: What's changed

The main changes I see in global events are:

(1) That because of oil we are back to a global economy that seems to have an inflation impulse (that is a more normal state of affairs). However, the nature of this 'impulse' is not really inflationary and neither is inflation really spreading. Yet, things 'look different' and headline prices do not look like deflation anymore.

(2) That growth is not looking as weak either. The PMI gauges for Europe are up; they are rising for developing economies too. But there is no 'boom.'

What's lacking

There is no real acceleration. Unemployment rate measures are either not very responsive (as in much of Europe). Or where they have been responsive, they are not creating the knock-on effects for wages or prices that they used to (Phillips Curve relationship is muted). While there is no call to action from superheated growth or from churning inflation, economic conditions are not as threatening to the downside and policymakers seem ready to act because of that. They are emboldened to try to restore some sense of normalcy to rate levels. The Fed is doing this and the Germans want to do it. But since there is little sense of acceleration in the economy, such actions might be like taking away the punch bowl before anyone has even tasted the punch. And what can that do to the party atmosphere? There should be more of a questioning of the switch to policy tightening and what impact it will have. We are barely out of the woods from the scare about deflation and backsliding. Rising oil prices only make it seem as though inflation has recovered much more than it has. When the dust from headline inflation settles, Japan will still be fighting deflation. The scariest thing I see in this new policy paradigm shifted environment is that central banks seem to think that downside risk is gone, that risks generally are more balanced and that such a thing means that rates can rise 'without consequence.' But since growth is still weak and still being helped by low rates, it does not make sense to think that removing the tail wind from the economy will not affect its speed. To me, such a proposition suggests that policy is trying to move full speed ahead to assert normalcy before normalcy has asserted itself. And putting the cart before the horse is always counterproductive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief