Global| Oct 23 2009

Global| Oct 23 2009EMU Orders Continue to Rise and Cut Year/Year Drop

Summary

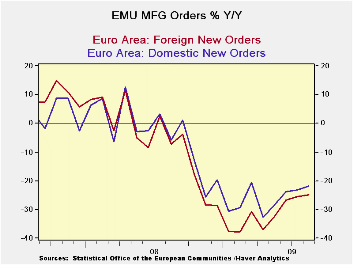

The EMU economy continues to spin off better economic signals. Orders rose by 2% in August after a 3% rise in July and a 4.2% gain in June. As a result the sequential growth rates are showing explosive growth in orders- up at a 43% [...]

The EMU economy continues to spin off better economic signals. Orders rose by 2% in August after a 3% rise in July and a 4.2% gain in June. As a result the sequential growth rates are showing explosive growth in orders- up at a 43% annual rate over three months - still orders are lower Yr/Yr by over 20%. EMU MFG sales were up in August, too, and they show sequential growth rates are improving.

Orders rose in two of the four largest economies as Italy and the UK took order setbacks in August. Italy and the UK also show dropping orders over three months.

The UK took a set back in growth as GDP dropped 0.4% Q/Q in Q3 (a 1.6% annualized rate of decline) an unexpected result that extends the UK recession that was thought to have ended. Italy ’s sharper drop in orders of 8.6% raises some questions there. The UK GDP drop has brought pressure on sterling as one might well have expected, but the weakness in Italy is another matter as it is safely cocooned within the euro area. We do not know how badly Italy ’s orders drop will affect the economy but retail sales have faltered recently. Consumers and businesses are seeing and expecting totally different trends there. The hardest thing for EMU policymakers is to have countries within the Zone moving in different directions.

| Euro Area and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | % m/m | Aug 09 |

Aug 09 |

Aug 09 |

Aug 08 |

Aug 07 |

Qtr 2 Date |

||

| Euro Area | Aug 09 |

Jul 09 |

Jun 09 |

3 Mo | 6 mo | 12 mo | 12 mo | 12 mo | Saar |

| Manufacturing Sales | 1.0% | 1.6% | -0.9% | 7.1% | 2.3% | -19.6% | 3.5% | 5.8% | 11.2% |

| Intermediate | -3.7% | 4.8% | 6.8% | 34.6% | 3.2% | -21.4% | 2.0% | 9.0% | #N/A |

| Manufacturing Orders | 2.0% | 3.0% | 4.2% | 43.7% | 20.4% | -21.8% | -2.1% | 4.7% | 37.5% |

| Countries: | Aug 09 |

Jul 09 |

Jun 09 |

3Mo | 6mo | 12mo | 12mo | 12-mo | Qtr 2 Date |

| Germany: | 1.8% | 2.0% | 4.1% | 36.9% | 33.2% | -24.7% | -1.0% | 6.0% | 30.5% |

| France: | 3.0% | 4.1% | 1.5% | 39.8% | 6.1% | -13.8% | -7.7% | 8.1% | 43.8% |

| Italy | -8.6% | 2.1% | 1.6% | -19.0% | -18.8% | -29.8% | -3.4% | -1.6% | -34.5% |

| UK(EU) | -15.6% | 7.3% | 3.6% | -22.5% | 1.3% | -11.1% | -12.6% | 4.3% | -48.8% |

Markit PMIS are up-beat - The goods news for EMU was that the Markit monthly look-ahead PMI reading for October improved overall and for each of MFG and Services. The MFG reading actually showed expansion for the first time since May of 2008. Overall the EMU area seems to be continuing its progress despite Italy ’s troubles.

Adding to the sense of good news in the face of the UK ’s ominous GDP drop was an improvement in Germany ’s IFO index as business climate improved along with current conditions and expectations.

A background report from the OECD demonstrated that world trade flows had stabilized in 2009-Q2. To be sure it remains a day of mixed data but putting the UK ’s GDP report aside the news elsewhere was pretty upbeat. Dropping UK GDP is a big fly in the ointment, but on the whole the signals from the UK economy have not turned uniformly glum. Until GDP was reported, based on data in hand, economists had expected a rise in GDP. Sometimes GDP accounting can have this effect. While GDP is the best comprehensive measure of how an economy is doing, around economic turning points oddities with trade and inventories can send mixed the signals more than they should. While we need to be wary of the UK economy’s performance, on the whole the global economy seems to be in an upswing and doing better. Ultimately that will help the UK too.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief