Global| Apr 30 2018

Global| Apr 30 2018EMU Money and Credit Vs. Money Growth Elsewhere

Summary

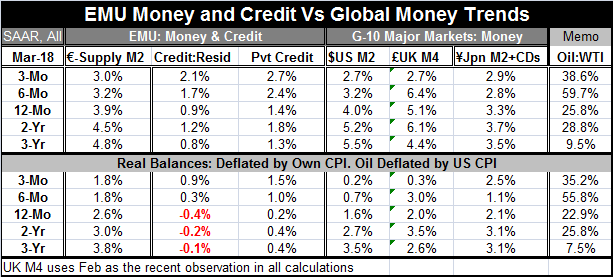

The chart shows the gradual roll-over in EMU money and credit growth. Both series have slowed over 12 months compared to their year-ago rates of growth. EMU private sector credit growth is at 1.4%, down from 1.8% a year ago. However, [...]

The chart shows the gradual roll-over in EMU money and credit growth. Both series have slowed over 12 months compared to their year-ago rates of growth. EMU private sector credit growth is at 1.4%, down from 1.8% a year ago. However, sequential growth rates over six months and three months point to a speed up in credit growth – that is encouraging. But on the same timeline nominal money growth is decelerating; monetary growth has steadily decelerated on all of the timelines in the table.

The chart shows the gradual roll-over in EMU money and credit growth. Both series have slowed over 12 months compared to their year-ago rates of growth. EMU private sector credit growth is at 1.4%, down from 1.8% a year ago. However, sequential growth rates over six months and three months point to a speed up in credit growth – that is encouraging. But on the same timeline nominal money growth is decelerating; monetary growth has steadily decelerated on all of the timelines in the table.

Expressed in real terms, the EMU money and credit gauge changes their growth rates but not their trends. Credit growth still decelerates year-over-year compared to its pace of a year earlier and over shorter horizons credit shows some signs of life and its pace picks up from 12-month to six-month to three-month. Real money balance growth decelerates steadily but then the growth rate gets stuck at 1.8% over six months and three months as it stops decelerating.

On balance, there is little in the trend of money growth that is encouraging at all. But the stirring of credit growth may be enough to be meaningful. For the first time in a long time, the growth rate of credit is close to the growth rate of money – at least over three months and six months.

Changing EMU expectations

However, expectations in the EMU are changing, according to the Survey of Professional Forecasters published by the European Central Bank on Friday. Euro area inflation is expected to rise more slowly over the next two years. Forecasters maintained their inflation expectations for 2018 at 1.5%. For 2019 and 2020, projections were trimmed to 1.6% and 1.7%, from their previous outlook of 1.7% and 1.8%, respectively. These are, of course, small changes but as always they reveal the mindset of the forecasting community and help to establish where they see risk. The risk is not in inflation running away. Even as forecasters have been envisioning inflation projections lower, they have revised growth slightly higher and set unemployment expectations at lower levels as well. It appears that the world no longer obeys Keynesian principles.

Globally money is weak or lethargic

Europe is not alone with money growth slowing. The U.S. shows real and nominal money growth slowing across all horizons in the table. 12-month U.S. money growth is at a pace of 4% while over three months the pace dips to 2.7%. The U.K. shows money growth slowing with some interruptions. U.K. nominal money growth speeds up over two years compared to three years and then speeds up over six months compared to 12 months. But at 2.7%, three-month U.K. money growth ties the U.S. for the weakest three-month pace in the table. U.K. real money growth does speed up over two years compared to three years as well, but then its one-year pace drops below even its three year pace. Japan’s money growth shows decelerations for the most part with an upturn over three months. The upturn is significant for the growth rate of real money balances. Japan is the only country with an upturn in money growth over three months compared to six months and the only country with three-month real money balance growth stronger than year-over-year growth.

On balance, the global monetary growth situation is still feeble. No one wants to make anything of it since money has not been a front and center policy gauge for some time. So interestingly, what we see are analysts ignoring money growth and making forecasts that are inconsistent with the precepts of Keynesianism. Isn’t that interesting? It makes you wonder what their underlying models are really like? Of course, the step up in velocity has filled the gap for now. But there is a broader question of whether this phenomenon is a new-normal conditions or something we should be concerned about. Slowing money and weak credit have not deterred the EMU forecasters from looking for stronger growth and improved economic conditions. But they have trimmed back their inflation outlook. It is interesting that this is going on in Europe as the Fed in the U.S. has hit its inflation target for the headline PCE and is on the cusp of reaching it for the core PCE. Still, there is little evidence anywhere of inflation concerns.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.