Global| Mar 27 2017

Global| Mar 27 2017EMU Money and Credit Growth Are Less Than Impressive Than Euro-PMIs

Summary

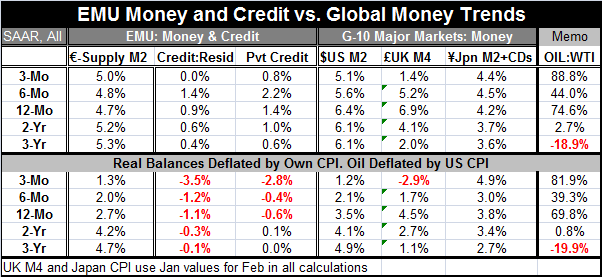

EMU nominal money supply growth is slightly higher over three months, but credit growth in the EMU is slower. Real balances (inflation adjusted month and credit) show slow and slowing money and credit growth with credit growth [...]

EMU nominal money supply growth is slightly higher over three months, but credit growth in the EMU is slower. Real balances (inflation adjusted month and credit) show slow and slowing money and credit growth with credit growth negative over 12 months, six months and three months. While there are signs of a pick-up in the Markit diffusion data on service sector and manufacturing sector progress, the financial side data tell a much grimmer tale with a less hopeful horizon.

EMU nominal money supply growth is slightly higher over three months, but credit growth in the EMU is slower. Real balances (inflation adjusted month and credit) show slow and slowing money and credit growth with credit growth negative over 12 months, six months and three months. While there are signs of a pick-up in the Markit diffusion data on service sector and manufacturing sector progress, the financial side data tell a much grimmer tale with a less hopeful horizon.

Globally, money supply growth is muted

Beyond the EMU, money growth has flattened or weakened. In the U.S., the U.K. and Japan, money is less ebullient. Moreover, real balance growth in money supplies shows decelerations in the U.S. and the U.K., but not in Japan where a real speed-up is in progress.

Oil puts policy on a more winding road

The summary data on oil are interesting. Over three years, oil prices are falling at an annual rate of 18.9%. Over two years, oil is up at a 2.7% annual rate. Over one year, oil is up by 74%. These metrics underscore how convoluted the oil price effect is. Depending on the length of the lagged impact of oil on the economy and on prices, oil is either very depressing, neutral or super-stimulating. That probably explains why all of the recent ratcheting of oil prices has had such a muted effect. Different industries and pricing mechanisms are probably in different stages of their own cycles in terms of dealing with what oil is doing let alone what is being planned for in the future. Over the past year, of course, oil is having a substantial upward impact on prices, but since oil has risen so strongly from such a low level, the impact on psychology is quite muted compared to oil's statistical one-year persona.

The uncertain impact of oil

The typical impact we expect from oil has not always evolved in this cycle at least not in the U.S. because the U.S. has been re-developing its own oil sector through fracking. As a result, when oil prices fell and stimulus to consumption was expected instead, there was a destructive impact on the oil sector that muted the stimulative impact of falling oil prices on the economy. Now with oil prices rising, we are tying gauge the net impact of that in the U.S. as well as globally. In the U.S., the rig count has been rising, signaling some revival in the oil patch, but actual oil pumping has lagged that statistic.

Oil is weaker again...oil market limbo: how low can you go?

Globally, oil prices are easing again (yes, I know it sort of makes your head spin that there are so many price twists and turns in the oil market) as the one-time production cuts that OPEC launched early in the year no longer seemed sufficient. Several weeks ago, the Saudi oil minister referred to OPEC production limits as being a still-new process and declared that adherence to the benchmarks was good across its membership. He suggested that OPEC was going to watch how things develop for a while and it may be that in the wake of these comments oil price weakness has been encouraged as some have perceived that the Saudis are on the sidelines for a while. But OPEC is a wily cartel and there is no telling what it will do next or when despite the fact that its membership is less powerful than it used to be, that its alliances are more fractious and that it depends more on voluntary nonmembers for compliance.

Time for a shift or just losing their nerve?

Globally, the lifting of oil price from their lows has injected the trappings of inflation into the headline of all nations' main indicators. But we also know that the nature of this price bulge is not really inflation per se but due to the lifting of the relative price of oil. Still, central banks, nervous about the extent of past stimulus, have taken this as an opportunity to express renewed fealty to price stability and to plan (as in Europe) or act (as in the United States) or talk (as in the U.K.) or not (as in Japan) about policy shifting to a less accommodative paradigm. The question is whether this shift is wise or properly timed.

Healthy PMI or pie in in the sky?

PMI data tell us that sectors in Europe are becoming better than they have in five to six years. And although that seems like a long leap, it is actually a small step over a low hurdle.

Real vs. financial schism

Business and consumer confidence readings largely are higher. But the financial data do not really echo this same sort of bravado. And one should wonder about the extent to which inflation is back or simply a headline patina covering over a still-troubled economic process. The revival of the PMI's is a nod to the notion of things being better. Stock prices and consumer confidence have been driven up globally by expectations of stronger U.S. growth and by the Trump rally in the U.S., a rally that has just recently run into the cold cruel and harsh reality of the divided and remorseless U.S. political scene. After an inability to pass his healthcare reform bill late last week, U.S. President Donald Trump is already threatening to pivot and make deals on tax reform or infrastructure spending with the Democrats instead of with the conservative Republicans who have been so impossible to deal with over the past eight years. Perceptions of fiscal, regulatory and tax progress must be kept intact if markets are to stay on course. Financial market success certainly has played a role in making people feel better. And the U.S. has helped to foster that perception globally. Meanwhile, across Europe some of the more feared economic scenarios do not seem to be developing and that too is helping policymakers to take heart. But are they hooking up their wagons to a train of false perceptions?

Nonperforming loan problems

In the EMU, there are still concerns about banks and about the extent of nonperforming loans (NPLs). Daniele Nouy, Chair of the Supervisory Board of the European Central Bank, said Monday that NPLs remain a big issue for some euro area members and would be a top priority for some time to come. From Q3 2015 to 2016, NPLs have shrunk across the euro area from 7.3% of loans to 6.5% so progress is being made but the issue is still a live one. She noted that NPLs weigh on the profitability of banks and limit their ability to finance the economy. In that regard, Italy is still trying to firm up its rescue plan for Monte dei Paschi di Siena and is working on requests for similar help from two other smaller banks.

Money, credit, and banking...oh my!

Despite the fact that core of the financial crisis has been left far behind, its legacy remains in many ways right on our doorstep. The inability to get money and credit flows to behave is reason enough to view things like apparent headline inflation or incipient strength in the real economy indicators with some degree of caution. Actually European money growth in the 4% to 5% range is just fine. That is plenty to allow nominal GDP to spin out less than 2% inflation and 2% (or so) growth. But the real problem has been decline in the velocity of money that has impeded that process. Loan growth, which is weak in nominal terms and falling in real terms, is the real reminder that all still is not well with money credit and banking in Europe. If that is true, how good can growth get?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief