Global| Nov 12 2009

Global| Nov 12 2009EMU MFG Still Digging Its Way Out

Summary

MFG IP in the e-Zone rose in September laying a foundation for continued economic recovery. Over three months the annual rate of IP growth is now 1.9% compared to flat over six months and lower by 13.8% over 12-months. To be sure the [...]

MFG IP in the e-Zone rose in September laying a foundation for

continued economic recovery. Over three months the annual rate of IP

growth is now 1.9% compared to flat over six months and lower by 13.8%

over 12-months.

To be sure the lift off in IP is less than in indicators such

as the Markit MFG PMI index or the jump in orders. But it takes longer

for actual output to be put to work than for indicators of improvement

to show progress. The large countries are showing more rapid increases

in growth than is EMU as a whole.

For Germany three-month growth is up at an 18.7% annual rate;

that is surpassed by the ever volatile results from Spain that

skyrocketed at a 29% pace over three months. France is up at an 8%

pace; Italy is up at a 4% pace. EU member the UK is lagging as it has

MFG IP up at a tiny 0.5% pace over three-months. For this group

six-month growth rates are all positive and the three-month results

show acceleration compared to six months. Over 12-months IP in all

countries still is falling rapidly, at a double-digit pace.

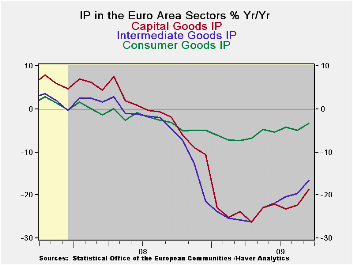

By industry the consumer sector continues to lag. Consumer

durables output is off on the month and over three months it is down by

-2.1% countered by a three-month rise of 1.6% in consumer nondurables

output. Capital goods output is up at a 6.6% pace over three-months.

Intermediate goods output is flying at a 13% annual rate of expansion

as commodities and raw goods lead the cycle

These figures confirm the trend we already have seen.

Consumers are lagging and raw goods are rising strongly. Investment is

picking up. Still consumer sentiment is one of the stronger barometers

for EMU even though consumer spending and the output of consumer goods

has been lagging.

| E-zone MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Sep 09 |

Aug 09 |

Sep 09 |

Aug 09 |

Sep 09 |

Aug 09 |

|||

| Ezone Detail | Sep 09 |

Aug 09 |

Jul 09 |

3Mo | 3Mo | 6Mo | 6Mo | 12Mo | 12Mo | Q-3 |

| MFG | 0.3% | 0.3% | -0.1% | 1.9% | 0.0% | 0.0% | -2.3% | -13.8% | -16.5% | 0.9% |

| Consumer | 0.3% | -0.4% | 0.5% | 1.4% | -0.8% | 1.7% | -0.6% | -3.2% | -4.9% | 1.0% |

| C-Durables | -6.0% | 5.2% | 0.6% | -2.1% | 8.3% | -10.7% | -4.2% | -19.2% | -15.0% | -- |

| C-Non-durables | 1.1% | -1.1% | 0.4% | 1.6% | -1.9% | 3.4% | 0.4% | -0.8% | -3.4% | -- |

| Intermediate | 0.6% | 1.0% | 1.4% | 13.0% | 13.4% | 10.7% | 7.3% | -16.6% | -19.6% | 14.1% |

| Capital | 1.7% | 1.4% | -1.4% | 6.6% | 0.5% | 3.0% | 0.2% | -18.7% | -22.2% | 2.1% |

| Main E-zone Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Sep 09 |

Aug 09 |

Sep 09 |

Aug 09 |

Sep 09 |

Aug 09 |

||||

| MFG Only | Sep 09 |

Aug 09 |

Jul 09 |

3Mo | 3Mo | 6Mo | 6Mo | 12Mo | 12Mo | Q:3 Date |

| Germany: | 3.2% | 2.1% | -1.0% | 18.4% | 7.1% | 14.9% | 9.6% | -14.3% | -19.2% | 15.2% |

| France:IPx Construct'n | -1.5% | 2.8% | 0.7% | 8.0% | 15.5% | 6.3% | 7.2% | -10.4% | -10.0% | 12.2% |

| Italy | -5.7% | 5.9% | 1.1% | 4.0% | 32.7% | 3.0% | 5.9% | -16.9% | -13.5% | 12.9% |

| Spain | 0.7% | -3.0% | 9.1% | 29.2% | 47.0% | 19.5% | 6.9% | -12.4% | -10.6% | 33.1% |

| UK: EU member | 1.7% | -2.0% | 0.4% | 0.5% | -4.0% | 0.2% | -2.5% | -9.4% | -11.6% | -0.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief