Global| Jun 03 2013

Global| Jun 03 2013EMU MFG PMIs Head Higher

Summary

In May the manufacturing index for the European Monetary Union rose to 48.32 from 46.69. Month-to-month the manufacturing barometers improved for every country in the table. The greatest month-to-month gain was in Denmark which [...]

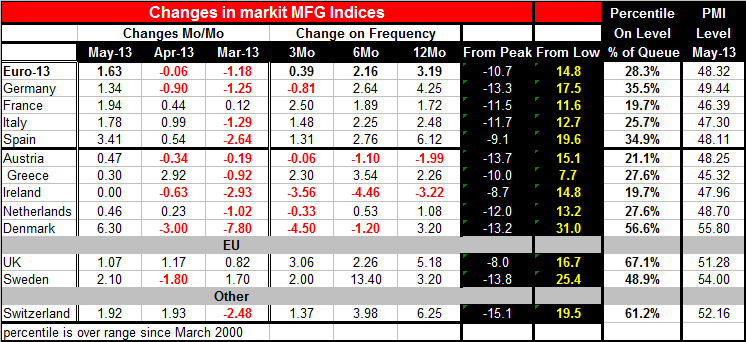

In May the manufacturing index for the European Monetary Union rose to 48.32 from 46.69. Month-to-month the manufacturing barometers improved for every country in the table. The greatest month-to-month gain was in Denmark which registered a surge of 6.3 points: next comes Spain, which improved by 3.41 points. Gauging its current level against its historic queue standing Spain is now nearly as strong as Germany is it stands in the 34.9 percentile of its queue compared to Germany at the 35.5 percentile of its queue. The German index level is at 49.44 in Spain the index level is at 48.11. Both indicate ongoing contraction. France's gauges are now improved over four months in a row, still it's index stands in the lower 20th percentile of its historic queue Austria and Ireland, the latter rated on last month's value (since the May figure for Ireland is not yet available), also stand around the 20th percentile of their historic queue. Italy stands in the 25th percentile of its historic queue; Greece stands at the 27th percentile same as the Netherlands while Denmark has the strongest relative standing at the 56.6 percentile of its queue. The EMU queue standing is in its 28th percentile.

In May the manufacturing index for the European Monetary Union rose to 48.32 from 46.69. Month-to-month the manufacturing barometers improved for every country in the table. The greatest month-to-month gain was in Denmark which registered a surge of 6.3 points: next comes Spain, which improved by 3.41 points. Gauging its current level against its historic queue standing Spain is now nearly as strong as Germany is it stands in the 34.9 percentile of its queue compared to Germany at the 35.5 percentile of its queue. The German index level is at 49.44 in Spain the index level is at 48.11. Both indicate ongoing contraction. France's gauges are now improved over four months in a row, still it's index stands in the lower 20th percentile of its historic queue Austria and Ireland, the latter rated on last month's value (since the May figure for Ireland is not yet available), also stand around the 20th percentile of their historic queue. Italy stands in the 25th percentile of its historic queue; Greece stands at the 27th percentile same as the Netherlands while Denmark has the strongest relative standing at the 56.6 percentile of its queue. The EMU queue standing is in its 28th percentile.

The EMU gauge improved on a net basis over three months, over six months, and over 12 months. So has the gauge for France, Italy, Spain, and Greece. Germany's indicator has fallen over the most recent three months as has a gauge for the Netherlands. Denmark's gauge is falling on balance over three months and six months despite the outsized gain it made in May- it has been extremely volatile. Austria and Ireland are declining on all horizons three months six months and 12 months. So many EMU members are experiencing very different trend forces at this time and members stand in very different positions of their historic queues. The challenge for policy remains great.

The UK and Sweden, both members of the EU but not locked in the common currency regime, show net increases in their manufacturing purchasing managers indices over three months six months and 12 months. Switzerland also shows gains over three months six months and 12 months.

There is a clear trend for improvement here.

It is evident in the calculations and it is evident in the chart. And even though there has been enough strength for the EMU region as a whole to advance on all these horizons, there remains some considerable variability within the euro-Zone itself. Today, Mario Draghi after a long period of silence once again made some positive comments about stabilization and the outlook for improved prospects in the euro-Zone. While the euro-Zone's problems are fixed, it does look as though the European, economy and the global economy have lost a lot of their downward pressures. Still, with concerns remaining about quantitative easing in the US as well as elsewhere we've seen markets that are looking to the transition away from QE become extremely shaky when they think that transition is close at hand. It's still too soon to be sure that we have dodged the final bullet because we still need to get the markets to make the transition from seeing central banks as helping them ahead every her step of the way to a time when they can stand on their own two feet and absorb the ordinary pressures of economic oscillation without the constant help of the Federal Reserve and other central banks propping up markets.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief