Global| Sep 10 2015

Global| Sep 10 2015EMU IP Shows Mixed Trends With Lingering Weakness

Summary

Spain is the large-economy success story for industrial production in the euro area. IP in Spain rose by 0.4% in July, up at a 3.8% annual rate over three months. The three-month pace is near the top pace for any EMU nation and by far [...]

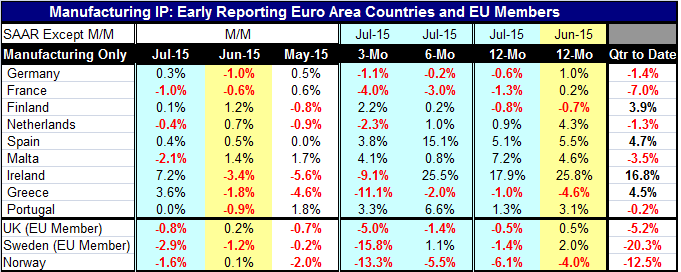

Spain is the large-economy success story for industrial production in the euro area. IP in Spain rose by 0.4% in July, up at a 3.8% annual rate over three months. The three-month pace is near the top pace for any EMU nation and by far the strongest pace for a large EMU economy. Similarly, Spain's 15.1% over six months trails only Ireland. Its 12-month pace trails Ireland and Malta, both small economies.

Spain is the large-economy success story for industrial production in the euro area. IP in Spain rose by 0.4% in July, up at a 3.8% annual rate over three months. The three-month pace is near the top pace for any EMU nation and by far the strongest pace for a large EMU economy. Similarly, Spain's 15.1% over six months trails only Ireland. Its 12-month pace trails Ireland and Malta, both small economies.

By comparison, German manufacturing IP is declining over three months, six months and 12 months. So is French manufacturing IP. Italy, the third largest EMU economy, has not yet reported for July.

The selected other European nations at the bottom of the table show abject weakness in manufacturing. Sweden and Norway show double digit annual rates of decline in IP over three months. The U.K. IP drops at a 5% pace over three months. Year-over-year IP is falling in each of these nations.

The picture emerging for manufacturing IP is not a strong one. Of the 12 countries in the table, six show output declines in July. Over three months, eight show declines. Over six months, five show declines. Year-over-year seven of 12 show declines. This is bad breadth.

Quarter to date- and it is very early in the third quarter- only four of these nations show IP is rising: Finland, Spain, Ireland, and Greece (one large economy, again Spain). Spain shows persisting upward momentum along with several of the smaller European economies. Nevertheless, on balance, the European data to date are not impressive.

Elsewhere...

This morning the Bank of England decided to leave it policy unchanged in a split decision. The BOE statement cited global economic conditions and expressed uncertainty about what the fallout from them would be. We can wonder if the BOE action is a preview of what the Federal Reserve statement will be next week. We already have stories in print from `those in the know' saying that the Fed has not been able to marshal the necessary votes for a rate hike at the upcoming meeting. Still, markets will stay on edge until the Fed decision is in the books. The BOE decision seems to provide a solid template for what the Fed will eventually do and say.

The OECD today released its unemployment rate for the whole OECD area, calling the area-wide unemployment rate unchanged. The unemployment rate has fallen by 1.3 percentage points from its peak in January 2013. The rate stands at 6.8%. These metrics tell us a lot about the feeble progress made in this economic recovery and the extent of the remaining unemployment problem. Developing economies are being hit hard. Today Brazil was downgraded to junk investment status by S&P. China's fortunes continue to hang in the balance. The Middle East is on fire with the extent of Russia's aid to Syria now a bone of contention. Greek elections have yet to be run and Europe is simply continuing its too slow recovery. On balance, there is a lot in the world that remains unsettled. Against that background, the pressures stemming from poor momentum and the poor breadth in the European manufacturing sector are not reassuring developments.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief