Global| Jul 12 2019

Global| Jul 12 2019EMU IP Is Surprisingly Strong

Summary

EMU industrial production jumped in May. After falling for straight four months, EMU IP jumped in January 2019, then was flat in February, fell for two more months in a row, and now it is up by 0.9% month-to-month logging only its [...]

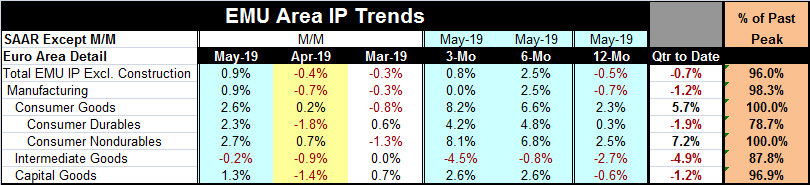

EMU industrial production jumped in May. After falling for straight four months, EMU IP jumped in January 2019, then was flat in February, fell for two more months in a row, and now it is up by 0.9% month-to-month logging only its second rise in nine months.

EMU industrial production jumped in May. After falling for straight four months, EMU IP jumped in January 2019, then was flat in February, fell for two more months in a row, and now it is up by 0.9% month-to-month logging only its second rise in nine months.

Despite the monthly rise, IP is still falling year-over-year and still consistent with the signal from the Markit manufacturing index. In fact, this is the second year-on-year decline in a row for manufacturing after posting two increases in a row in February and March. Despite the sizeable monthly rise, the year-on-year drop deepened to -0.7% in May from -0.5% in April.

Output only declined in the intermediate goods sector in May. Sequential growth rates from 12-months to six-months to three-months show few clear trends. One clear trend, however, is for consumer goods, driven largely by nondurable goods where acceleration is clearly in play. Intermediate goods do not show a trend, but sector output declines on all timelines. Capital goods show a weak acceleration as the year-over-year drop in output gives way to the same 2.6% growth rate over three months and six months.

However, the quarter-to-date statistics show a good deal of weakness. Output is declining two months into the second quarter in most sectors except for overall consumer goods because of strength in nondurables. Total output is contracting, manufacturing output is contracting, and consumer durables output is contracting, Intermediate goods output is contracting and capital goods output is contracting. There is still one month to go to complete the quarter so these tendencies could change.

Output as a percentage of past peaks by sector shows consumer nondurables output back to its past peak and that is true for consumer goods output overall as well. The consumer sector has been leading the way forward. Intermediate goods are only at 87.8% of their past peak after declining over a long period. Capital goods are at their 96.9 percentile of their past peak despite a modest year-over-year output decline.

Output as a percentage of past peaks by sector shows consumer nondurables output back to its past peak and that is true for consumer goods output overall as well. The consumer sector has been leading the way forward. Intermediate goods are only at 87.8% of their past peak after declining over a long period. Capital goods are at their 96.9 percentile of their past peak despite a modest year-over-year output decline.

On balance, output in the EMU is being better maintained than expected. Manufacturing IP is still tracking with the Markit diffusion report showing that contraction remains in play. But both manufacturing IP and manufacturing PMI readings show that tendencies to decline have begun to slow in recent months. What is clear is that weakness, while persisting, is not gaining momentum.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief