Global| Sep 12 2018

Global| Sep 12 2018EMU IP Falls Again in July and Barely Gains Year-on-Year

Summary

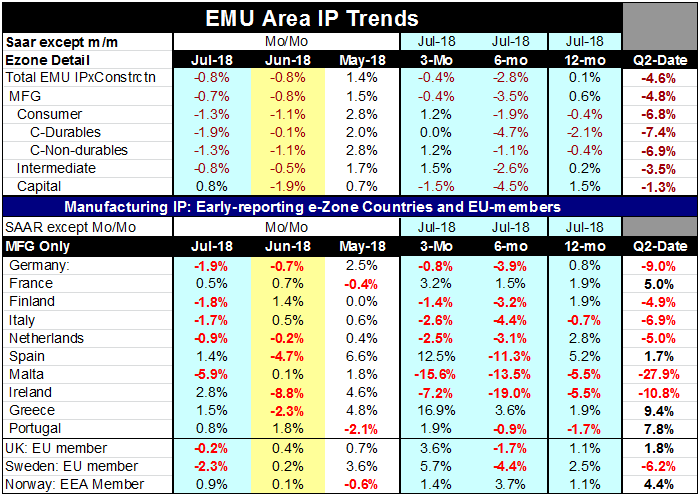

Industrial production trends show output slowing across all three sectors in the chart of 12-month rates of growth. Sequential growth rates from 12-months and less (table) do not show a steady deceleration but do show a legacy of [...]

Industrial production trends show output slowing across all three sectors in the chart of 12-month rates of growth. Sequential growth rates from 12-months and less (table) do not show a steady deceleration but do show a legacy of weakness.

Industrial production trends show output slowing across all three sectors in the chart of 12-month rates of growth. Sequential growth rates from 12-months and less (table) do not show a steady deceleration but do show a legacy of weakness.

12-month trends

Over 12-months total IP less construction is up by a skinning 0.1%. All consumer categories of output show declines over 12-months. There is a 0.2% rises in the output of intermediate goods over 12-months. Capital goods carry the brunt of the load for growth with output up by 1.5% over 12-months.

Inside 12-months: devils and angels

Over six months there are declines in all sectors of IP. The deepest decline is the 4.7% annual rate from for durable consumer goods output followed by the 4.5% drop for capital goods hot on its heels. Over three-months overall IP is lower and manufacturing IP is lower in both cases dragged down by the 1.5% decline in capital goods output. Ironically capital goods is the sector holding output up over 12-months but it is also the sector driving output to contact over three-months.

The circumstances of nation-members

Country level data show output declines in July for 5 of the 10 EMU countries in the table plus declines in two of three other reporting countries (UK and Sweden log declines while Norway posts a gain). There were also five out of ten EMU member IP-reporting countries with output declines in June but only two in May. Output clearly has been in an irregular patch. Over three months output is falling in six-member countries, over six-months it is falling in eight of ten of them. Over 12-months output falls in four of ten EMU reporters.

As between large and small counties in EMU France shows no IP declines over 12-months 6-months or three-months. Spain has a decline on only one of those horizons (6-months); Germany has declines over three-months and six months while Italy logs declines on all the horizons.

Quarter-to-date

A quarter to date basis (...a calculation that is now very early since it applies to the July level of output compounded as a growth rate over the Q2 average) reveals declines across the board for all sectors of output with headline output falling at a 4.6% annualized rate. Consumer goods show the greatest weakness on this period with capital goods (at -1.5%) the least weak sector. Looking at country level data there are declines in 6 of 10 EMU reporters in the table. Tiny Malta and Ireland show double digit declines while Germany, the largest EMU economy shows a 9% rate of decline, impressively weak for a large economy. Italy shows a drop at 6.9% annual rate while both Spain and France log solid increases on the period. Greece and Portugal show the strongest gains among the group

Summing up IP

On balance the IP data echo what we have been seeing in other recent reports and surveys on the European economy. Yesterday’s Zew survey showed a brighter assessment of current conditions than what output trends seem to paint here today. Zew showed a lot of concern for the outlook and at some point concerns about the future can and will affect the present.

Global conditions

Mark Carney’s term at the BOE has been extend by eight months. Today he warned about the importance of the Chinese economy for global growth. China issued statistics showing than loan growth there had fallen. Some estimates are showing the potential for a sizeable hit to China’s GDP growth if the next round of tariffs from the US goes into effect. Chair of the Supervisory Board of the European Central Bank Daniele Nouy said today that the global financial system is in much better shape today to face another crisis when it occurs. Should these sorts of comments ‘reassure us’ or should we run for the hills? After all did your Mommy hold your hand and tell you everything was OK in the middle of a lightning and thunder storm or did she do it on a bright sunny day? Just wondering…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief