Global| Sep 14 2020

Global| Sep 14 2020EMU IP Continues Its Strong Rebound...Can It Continue?

Summary

There are at least two stories on how to look at the evolution of IP in the EMU. One is to note the sharp ongoing rebound that is clearly depicted in the table as well as in the chart. The other is to note how, despite this recent [...]

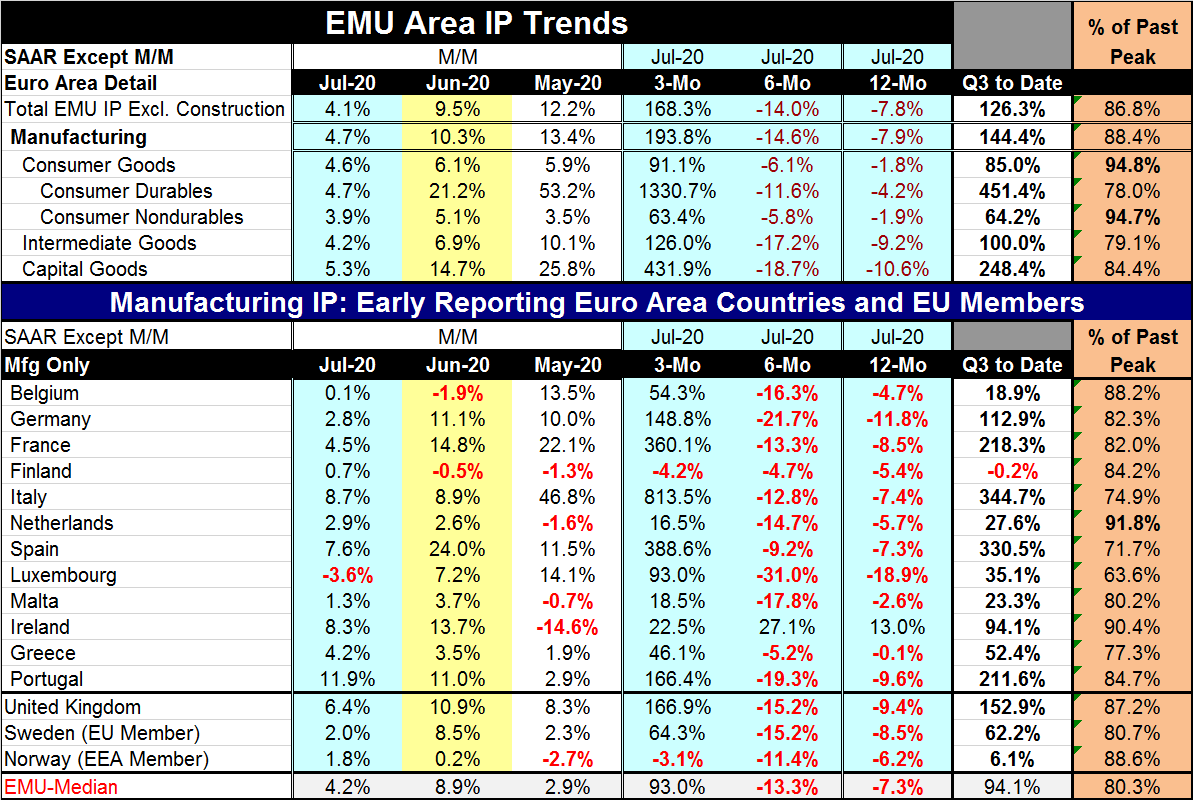

There are at least two stories on how to look at the evolution of IP in the EMU. One is to note the sharp ongoing rebound that is clearly depicted in the table as well as in the chart. The other is to note how, despite this recent surge, IP still lags below its past peak values. So IP is rising rapidly, but it remains below recent past peak levels for output. Manufacturing IP is some 7.7% below its level in February of this year and also some 9.2% below its level of output of February 2019. In the last 14 months, manufacturing IP has fallen in eight of them although it has risen for three months in a row gaining back a cumulative 30 percentage points of output in those three months -- wow!

There are at least two stories on how to look at the evolution of IP in the EMU. One is to note the sharp ongoing rebound that is clearly depicted in the table as well as in the chart. The other is to note how, despite this recent surge, IP still lags below its past peak values. So IP is rising rapidly, but it remains below recent past peak levels for output. Manufacturing IP is some 7.7% below its level in February of this year and also some 9.2% below its level of output of February 2019. In the last 14 months, manufacturing IP has fallen in eight of them although it has risen for three months in a row gaining back a cumulative 30 percentage points of output in those three months -- wow!

Those two perspectives are the 'good' and the 'bad' of IP output trends. But the future will not be decided by past trends, long or short; it will be decided by the conduct of the virus which is having another outbreak in Europe – more on that later.

The unfolding trends are confusing enough to handicap as they show generally enormous three-month growth rates, sizeable contractions over six months and net declines over 12 months. The quarter-to-date trends show more enormous rates of growth by sector as well as across countries with only Finland showing a QTD output decline in July. France, Italy, Spain and Germany, are the four largest EMU economies; they show manufacturing gaining in the quarter at annualized growth rates that range from 112% to 344%.

Manufacturing sector consumer durables output is rebounding the fastest of the sectors, followed by capital goods over both three months and in the QTD period. Consumer durables output is still lagging, however, as it is only 78% of its past peak value which is the weakest across sectors only slightly weaker than the 79% ratio for intermediate goods but well behind consumer nondurables that are 94.7% of their past peak and capital goods (84% of past peak).

By country, we have already named some of the strongest performers and they are among the largest EMU economics. However, at 91.8% the Netherlands has output at its highest ratio to its past output peak while Spain at 71.7% and Italy at 74.9% are among the weakest on this gauge (despite surging growth!) after the outlier Luxembourg where output is only 63.6% of its past peak.

When someone's medical facts rule the world...

Medical experts are racing to produce a vaccine. That could potentially open economies and free them from concerns of backsliding and having infections spread again. The problem with the current set-up (everywhere but Sweden) is that reliance on mitigation and lockdowns to slow the spread of infection set the stage for repeat and seemingly never-ending performances. Since no country except Sweden seems reasonably confident to let infection spread as long as it does not overwhelm the heath system, every time a new outbreak occurs the policy response is to shut up shop and slow the spread. If that stoppage is effective it will keep the virus from spreading very much and that will put the economy at a greater risk for reinfection than if the virus had been allowed to 'run its course.' There is no debate about this as being a policy that is in some sense based on its own demise. Reopening leads to the spread of infection which lead to mitigations or shutdowns and then the cycle runs again. A vaccine would have the power to break these cycles by inoculating people against reinfection so that upon a start up there would be no further infection spread because of the immunity the vaccine would bring. But vaccines are still developmental and engaged in a pipeline process of some complexity. Even if they do pass muster, they will have to be manufactured, distributed and administered a process that will take some time.

Meanwhile, we trust science...or do we?

While you are undoubtedly familiar with the expression 'Trust Science,' you may not really have focused on what it means. This is an expression used by anyone who does not like the behavior or speech of another person. It is a slap in the face intended to make that person act as the first person would have them act based on science as he or she knows it. But the problem with this is that science does not and has not been speaking with one voice. Science is dynamic; it learns new things that sometimes contradict old things. Sometimes science 'does not know'…or only has a hunch. Science is complicated and not just because science as a discipline is complex. There is also the 'complication' that there are many different angles to science and, if you will, many different 'sciences' whose opinions are relevant. Often the phrase 'Trust Science' is meant to 'shout down' any factual or scientifically accurate statement that may come into conflict with what someone's favored epidemiologist might say. And remember epidemiology is not the only science here.

Since the virus is not very lethal and preys mostly on people with weakened immune systems killing most among the old, among those with other medical conditions and with 44% of the dead (in the U.S.) being in nursing homes, there is a lot of room to frame the pandemic concerns in a different ways and to focus instead on the sorts of problems that arise when economies are shuttered. Stay at home orders also spawn their own medical and psychological issues as well as creating horrible economic conditions financial strains bankruptcies and conditions that eventually create very bad feedback loops back into the realm of health care. There are various 'sciences' to study these effects.

There is still no balance or even an attempt at a balance or cost-benefit analysis being done on the trade-offs among the costs flagged by the different sciences. As the virus fades and as vaccines are developed (if they are developed) and as infection rates gradually rise, all of these problems will eventually solve themselves. But it's an age of science. When we know so much, why do we use so little of what we know and instead used stupid phrases to try to cow others into to doing the bidding of those who are in charge? Why not take issues and policy dilemmas head on and solve them with real science? This is a question that various democracies are going to have face when this crisis is over. Shutdowns cost people their freedoms. Did all of these countries take the right steps for the right reasons? Was the medicine worse than the cure? Why did no one try to find out? Who 'died' and made the epidemiologists kings in the world of the selective pandemic? We may never find out.

Commentaries are the opinions of the author and do not reflect the views of Haver Analytics.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief