Global| Sep 16 2013

Global| Sep 16 2013EMU Inflation Trends Stabilize and May Hide Problems

Summary

The chart shows the path of inflation in the European Monetary Union and for a few select members using the harmonized index of consumer prices (HICP) for EMU and for each country. What's interesting about the chart above is that [...]

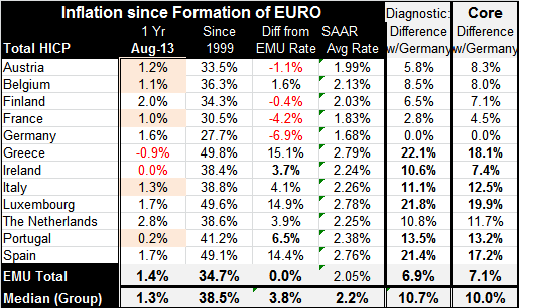

The chart shows the path of inflation in the European Monetary Union and for a few select members using the harmonized index of consumer prices (HICP) for EMU and for each country. What's interesting about the chart above is that since inflation came down and a started to increase again, inflation has been increasing slightly faster in Germany than the other countries and in the Zone at large. This is significant because Germany historically is the low-inflation country in the European Monetary Union. Instead, here we see that the overall EMU pace is below the German pace, that the French pace is lower and that the German pace, and Italy's inflation is also lower than Germany's. Part of this is that the German economy is growing better, faster, more solidly than the EMU region and in comparison with France or Italy. Some of it seems to be that Germany has decided not to turn the screws down quite so hard in fighting inflation.

The chart shows the path of inflation in the European Monetary Union and for a few select members using the harmonized index of consumer prices (HICP) for EMU and for each country. What's interesting about the chart above is that since inflation came down and a started to increase again, inflation has been increasing slightly faster in Germany than the other countries and in the Zone at large. This is significant because Germany historically is the low-inflation country in the European Monetary Union. Instead, here we see that the overall EMU pace is below the German pace, that the French pace is lower and that the German pace, and Italy's inflation is also lower than Germany's. Part of this is that the German economy is growing better, faster, more solidly than the EMU region and in comparison with France or Italy. Some of it seems to be that Germany has decided not to turn the screws down quite so hard in fighting inflation.

However, we know from recent comments from Jen Weidmann at the Bundesbank that there still is no tolerance for excessive inflation in Germany. The German view is that the ECB's policy of `forward guidance' is not embraced at the Bundesbank as a policy to forebear a rise of inflation.

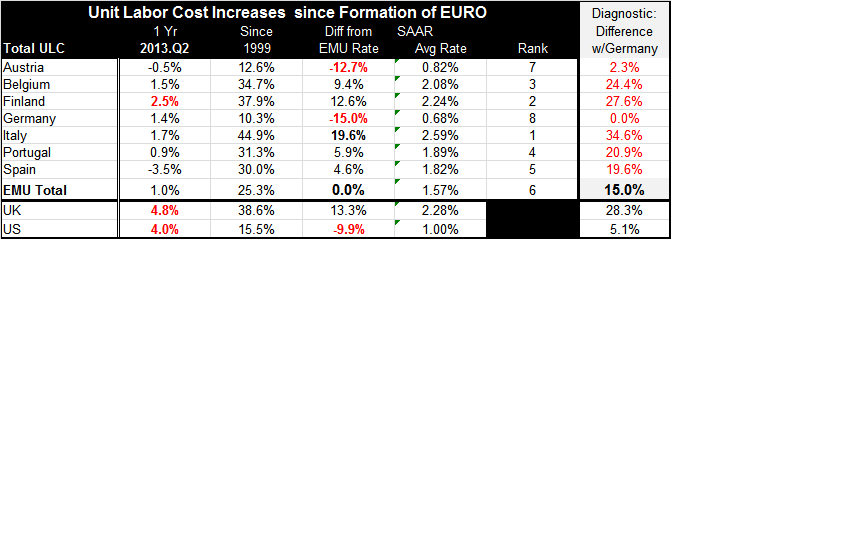

Not all EMU members have contributed up-to-date data for unit labor costs. But to make the point of competitiveness differences we have to add data on productivity to data on inflation. Unit labor costs do exactly that. The table provides some cross sectional results that are more or less in line with what we've seen from consumer price comparisons. Since the formation of the monetary union German unit labor costs have risen by only 10.3%. On balance this compares with a 44.9% rise in Italy the country with the largest gain in the table. Of course, the UK also shows a big increase in unit labor costs at 38.6%, but that's not such a big deal since the UK is not in the single currency mechanism and the pound sterling is free to decline in value to restore British competitiveness if its ULC rises too much.

Austria is the EMU country that has tracked the most closely to German labor costs, where its costs have increased by just 12.6% overall. By comparison US unit labor costs have risen by 15.5% during the same period just slightly back of the result for Austria and much better than any other monetary union member in the table.

In looking at unit labor costs, which are basically wages adjusted for changes in productivity, we can see that during this period German workers were not very well compensated by the standards of the m monetary union. There are different ways to think about unit labor costs.

Clearly because we call the statistic `unit labor costs' we tend to look at this measure from the firm's side and we tend to look at low labor costs as a very good thing. Low unit labor costs will keep a country's labor force highly competitive. To the extent that labor is an important input in the production process, keeping labor costs down relative to their productivity is a way for firms to stay competitive or to become more competitive. The one message in this table is that the German firms during this period became much more competitive relative to their fellow members in the monetary union based on labor cost developments. The second message is that German labor was not very well compensated during this period. Compared to their productivity, Italian workers were paid very richly as were workers in Finland and Belgium and Portugal and Spain. Workers were given increases far in excess of their productivity and that's undoubtedly led to an increase in their living standards and their ability to consume. Living standards rose in the rest of Europe faster than in Germany but the increase was built on a shaky base since firms were basically paying workers out of `profits' and in excess of what their labor input warranted. This undermined the health of the employers. To some extent the added gains came in the form of higher inflation and since public sector workers kept their wages at parity with the private sector, the burden on government finances grew.

When we see statistics like this we are reminded of the complicated nature and responsibilities of being locked up in a monetary union with another country. We think of Germany as the strong country in the European Monetary Union, yet it doesn't grow very fast. The German economy does not shift into overdrive. It's an economy that can sustain first and second gear and grind it out under almost any circumstance. It's the stability of this economy, in its ability to continue to move forward under a host of different experiences, as well as its population's fear of inflation and willingness to accept modest increases in their standard of living that marks Germany as different. Since this country is going to be the anchor for the European Monetary Union it is going to be difficult for any other country to possess a different set of values and to prosper in the Union where its currency will be tied to the German currency. And its labor will be in direct competition with German labor.

In other words if you are an EMU member country and you want to have a higher standard of living, if you want your living standard to rise faster than Germany's, then you need to find ways to increase your productivity so your productivity-adjusted wages will not go up any faster than Germany's. Then you won't experience a loss in competitiveness as you raise your standard of living. This is definitely not the way of the European Monetary Union has been operating.

The differences that we chronicle in these tables marking costs and in prices across the e-Zone, reflect a lot about the different philosophies of the countries whose currencies are tied together in the European Monetary Union. It should be very clear that the economics of being in the same union is going to force some degree of sameness about these values onto member countries. The economics of choosing different welfare trade-offs will definitely play out under the competitive process of the European economy -across borders and under the protection and constraints of a single currency. Europeans have to decide what they're going to do to try to preserve some degree of national distinctiveness and yet not undermine or exacerbate differences in competitiveness. While nations might espouse very different attitudes about social welfare and pay, there will be economic limitations that will provide an underlying constraint to countries that have values that stray too far from the norm- unless those nations adopt compensating mechanisms.

While the recent data on inflation show that some countries have finally been able to undercut Germany on inflation when you look up and down the line of the countries that are running low-inflation rates it is a largely in countries that have been under the yoke of a terrible burden of austerity where this progress is being made. These countries are paying a very high price in terms of unemployment and low growth; the lower inflation rate is being bought at an extremely high price. For this reason I don't look at the chart on inflation rates or at the table for the broader group of countries and conclude that Europe is finally moving in the right direction. It seems clear to me the while this is `progress in the right direction,' it is also progress that is being bought at a price that is unsustainably high. Europe still needs to find another way to gain convergence and to smooth over accumulated differences in competitiveness in order for the European Union to achieve sustainability.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief