Global| Aug 31 2015

Global| Aug 31 2015EMU Inflation: Stuck Low

Summary

The EMU HICP gauge in August fell 0.1% m/m. The core measure ticked up 0.1% after a 0.2% July increase. Headline inflation has fallen month-to-month in two of the last three months. Sequential inflation from 12-month to six-month to [...]

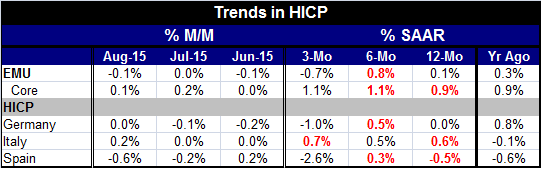

The EMU HICP gauge in August fell 0.1% m/m. The core measure ticked up 0.1% after a 0.2% July increase. Headline inflation has fallen month-to-month in two of the last three months.

The EMU HICP gauge in August fell 0.1% m/m. The core measure ticked up 0.1% after a 0.2% July increase. Headline inflation has fallen month-to-month in two of the last three months.

Sequential inflation from 12-month to six-month to three-month has no clear patterns, but it is not headed toward 2%. Core inflation is up from 0.9% over 12 months to running at a 1.1% pace over each of three-month and six-month, not much acceleration. Headline inflation is falling over three months, clearly not on a path to 2%.

The chart shows that inflation continues to run tepid in the largest EMU economies. At least the ECB has shaken off the brief period when prices were falling year-over-year. For a few months, it looked as though the turn from negative inflation to positive inflation would be decisive. But in subsequent months the bounce in prices gave way to more lethargy; currently over three-month prices are falling again at least on a month-to-month basis.

The EMU, facing still-weak GDP growth, has not had a compounded quarterly growth rate above 1.5% since Q1 2011. Only Finland has negative growth in Q2 year-over-year, but three of the 11 first member countries in the EMU are seeing GDP decelerate. Spain has the highest four-quarter growth in the EMU at 3.1% with the Netherlands at 2%, as the second best. With growth so weak, it is hard to get any traction for inflation. The ECB targets inflation just below 2%. Like the Fed, the ECB is making no progress toward its inflation target.

Globally China has just dropped a bomb on expectations about how weak its economy has become; its markets are backtracking rapidly. Oil and other commodity prices are dropping with no sign of catching on. That weakness is transmitting further weakness to developing economies that rely on the export of commodities to generate their income and growth. The weakness in the global economy shows no sign of letting up, although the authorities in the U.S. are hopeful that the U.S. economy will pick up in the second half of the year.

Fiscal austerity remains the rule of the day. While some countries have chosen to pursue a strategy of currency depreciation, that can't stimulate global growth; it can only rob from Peter to pay Paul. China's desperate depreciation strategy is a greedy me-first tactic as China has thrown in the towel on its ability to replace export demand with domestic demand.

Meanwhile, oil remains in surplus and the Saudis are still pumping oil at speed. Fracking in the U.S. has continued with U.S. output having actually risen in the last few months. Oil storage facilities are filled to overflowing.

It is not an environment in which one would expect inflation to make an about face quickly. The ECB and the Fed are likely to continue to see their inflation rates undershoot their respective targets for some time to come. There are individual country issues for inflation, of course, but the excess capacity and commodity glut are global problems that have some staying power. And nowhere in the G-10 has domestic growth been strong enough to raise inflation appreciably.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief