Global| May 17 2019

Global| May 17 2019EMU Inflation Shows Some Pressure; Germany Shows Even More...

Summary

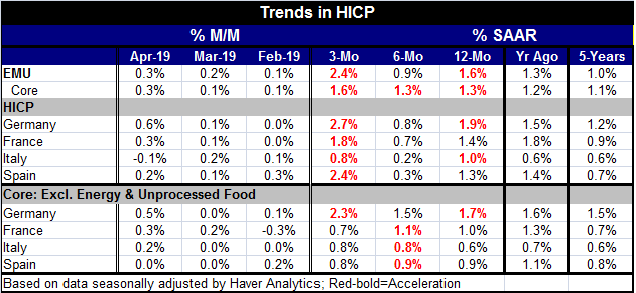

Every picture tells a story was we well know. And it is said that a picture can be worth a thousand words (sometimes more). In that vein (although I will not stop writing), the chart speaks very loudly and carries some unusual [...]

Every picture tells a story was we well know. And it is said that a picture can be worth a thousand words (sometimes more). In that vein (although I will not stop writing), the chart speaks very loudly and carries some unusual inflation schtick.

Every picture tells a story was we well know. And it is said that a picture can be worth a thousand words (sometimes more). In that vein (although I will not stop writing), the chart speaks very loudly and carries some unusual inflation schtick.

No, this is not a comedy routine and especially not if you are German. The ECB speaks loudly but doesn’t carry the inflation schtick that Germans want to see. The chart reminds us that while Keynesianism may seem to be dead in some respects (such as when we try to resuscitate the Phillips Curve), Keynesian principles still can carry clout. The chart spouts the ‘heresy’ that during this period Italy not Germany has been the low inflation country and that Germany has been the high inflation country. This as you can see has been in progress for some time. It did not just happen and it did not happen overnight. But it does put the constant pressure by Germans for the ECB to raise rates and normalize policy in some perspective. It also may explain somewhat why Germany is so determined to run a fiscal surplus since fiscal policy is all that Germany can control anymore. The ECB controls monetary policy and monetary policy is made for the whole of the union which Germany is not right now very representative of despite the higher weights that German data carry in setting the ECB data table (see Table below, if you prefer to paint by numbers). Note that the five-year headline and core inflation rates have Germany as number one; this is no fluke of the month. And Italian headline and core rates rank at the bottom for five-year inflation trends. Has Hell frozen over?

Why/how has this happened? This is the result of German prosperity and of Germany forcing austerity on other countries with budget/debt violations. Germany now has the lowest unemployment rate in the EMU and that percolates traditional Keynesian pressures (Ah, there’s that guy Keynes! Guten morgen). Meanwhile, Italy’s GDP is still below its prerecession level of GDP in real terms and has suffered greatly under austerity. All this slack has lowered inflation in Italy and has prompted a social uprising as renegade Italian political factions now run the Italian government and are looking to upset the EU apple cart in the upcoming elections.

Germany is slipping back in the inflation queue

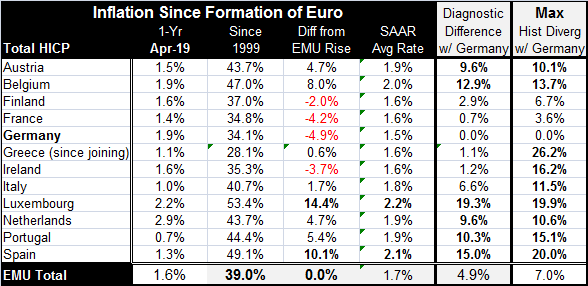

Inflation data since the EMU was formed are arrayed in the familiar table below. I drag this table out from time to time to show the cumulative effect of countries tied together in the same currency system but running different domestic rates of inflation. The far right hand column shows what the maximum start-of-euro-to-date divergence has been with Germany for each country. There are nine countries that, at one time or another, had a maximum divergence in double digits. Currently, that number is down to six even after rounding up. Italy, Ireland and Greece are notable for their improvement.

There ae now five countries among the earliest EMU members with EMU-start-to-date price levels that have risen by less than 5 percentage points more than Germany’s. This marks a lot more members that can compete with Germany on even terms within the EMU. Italy is only at a 6.6% disadvantage Luxembourg is a financial center so its competitiveness loss is not an issue. But Austria, Belgium, the Netherlands, Portugal and Spain are still behind despite some of these countries having made significant progress.

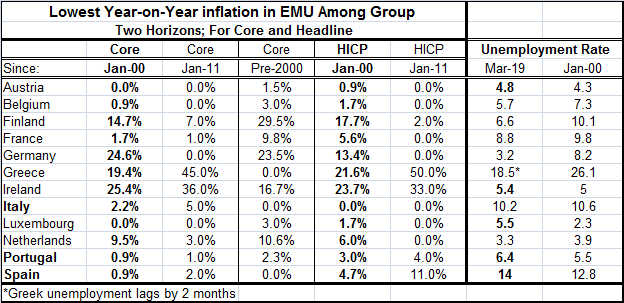

The table below compares the old with the new. We show how often which countries have had the lowest year-on-year inflation rate as measured by the headline or core since 2000 and since 2001 in the wake of the financial crisis.

For the core pre-2000, Germany had the lowest rate 23% of the time. That was exceeded only by Finland whose rate was lowest 29% of the time. Ireland was lowest 16% of the time. The Dutch were the low man 10% of the time.

Sticking to the core measure and looking at results since 2000, we find Germany has had the low inflation rate…never. N-E-V-E-R. Greece has had the low rate (brace yourself) 45% of the time. Ireland has had it 36% of the time. Finland has had it 7% of the time. Italy has had it 5% of the time.

While inflation has not been entirely bottled, only Luxembourg and Spain run inflation from the EMU start-date to today that is above the ECB mandate. Belgium is a hair stronger with a pace at 2% flat instead of a bit below 2%. Of course, countries are still at a disadvantage to Germany since it has kept inflation low at 1.5% on average since the EMU was formed. Countries with competiveness issues have them mostly relative to Germany more than they have them because they have overshot the ECB’s (implicit country) target.

Of course there is no country by country target for inflation. The data are for comparison sake and to further understanding of the inflation process. The ECB shoots at united country-weighted aggregate. That has risen at a 1.7% pace since the EMU has been in place.

Crossroads or double crossed at the roads?

Now Europe is at different cross roads. It has been moving slowly cautiously toward integration and more integration in the Post WWII period. First commercial policies were aligned beginning with the Iron and Steel Community and then expanding. Eventually the customs union was formed (a ‘free trade’ area) with a common tariff imposed on outsiders. And some EU members eventually joined their currencies (EMU). Some opted out of the currency fix and that was allowed. However, since then, any member admitted to the EU is an aspiring EMU member as well.

The migrant crisis has blown a lid off of what were already simmering tensions. There is no political unity; countries still make their own foreign policy. There is no common fiscal policy. Interestingly, a country like Finland with a strong socialist make-up has no interest in joining a fiscal union. This points out how much individual countries’ economic systems are organic and form from the social fabric of the country. Finland does not trust its tax revenue in the hands of outsiders. Europeans do not want another layer of government spending to support. So the chance at a stabilizing fiscal policy is going to pass it by (Keynes again). But as others have noted, fiscal policy has become structural and there is little left of the role for Keynesian cyclical fiscal stimulus because stimulus is always in gear.

It is not surprising that while the EMU can claim some success and even transformative success on the inflation front it can’t do that with growth or with unemployment. But of course, the EMU is a monetary union. It is dedicated to monetary stability and from that better economic prospects are supposed to flow… have they? There is still substantial variation across countries for the unemployment rate. But today the intra-European variation among unemployment rates is about half of what it was in January 2000. The rate itself is about two percentage points lower (unweighted). But the results are uneven. Greece and Germany have made the most progress in reducing their respective rates of unemployment. But while Spain’s and Italy’s rates are lower than they were, they are still in double digits; France is not far behind.

There is backlash to the way Germany and France as the two largest economies in the EMU have dominated the euro area. With the EU losing the U.K., the influence of Germany and France will loom larger at a time that there is a rebellion against it. Despite an etched in stone Maastricht set of rule specifying how high debt can be relative to GDP and how large annual fiscal deficits can be relative to GDP, several countries want more flexibility. European elections are upcoming and that battle is about to be fought.

Outside of Europe, there are also changed relationships with old allies like the U.S. Europe has not been eager to just follow the U.S. lead. The U.S. and Europe are on the verge of opening trade talks and the EU and the U.K. can’t decide what their new post-Brexit relationship will be. There is a lot in flux in Europe. It ranges from the economic to the geopolitical. And what happens here will define the rest of the millennium.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief