Global| Nov 13 2014

Global| Nov 13 2014EMU Inflation Divergences Show Progress- But Is It Enough?

Summary

Both the chart and the table show evidence of diminishing inflation differentials within the European Monetary Union. Among the plots in the chart, we can see the EMU inflation rate, Italy's inflation rate, France's inflation rate, [...]

Both the chart and the table show evidence of diminishing inflation differentials within the European Monetary Union. Among the plots in the chart, we can see the EMU inflation rate, Italy's inflation rate, France's inflation rate, and Germany's inflation rate. The German inflation rate is the highest among all those countries in the EMU region. This is significant because in the history of the EMU, Germany has had the smallest cumulative increase in its consumer price index, and therefore has consistently run the lowest inflation rate. That means that over the years Germany has acquired the largest improvement in competitiveness against all EMU members where all share the same currency, the euro.

Both the chart and the table show evidence of diminishing inflation differentials within the European Monetary Union. Among the plots in the chart, we can see the EMU inflation rate, Italy's inflation rate, France's inflation rate, and Germany's inflation rate. The German inflation rate is the highest among all those countries in the EMU region. This is significant because in the history of the EMU, Germany has had the smallest cumulative increase in its consumer price index, and therefore has consistently run the lowest inflation rate. That means that over the years Germany has acquired the largest improvement in competitiveness against all EMU members where all share the same currency, the euro.

If you believe as I do that one of the problems facing the EMU is that since it has been formed member countries have run different inflation rates, and therefore have created a heterogeneous network of competitiveness within the single currency area, then this development is a very positive one. The more that price levels within the community tend to gravitate back to their original relative positions the better the community is going to operate.

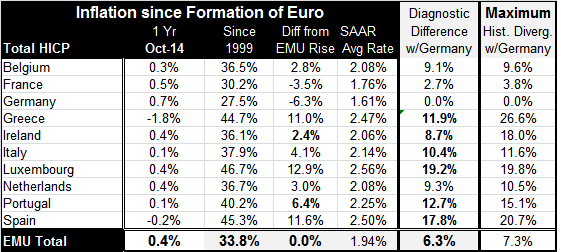

In the table, the far two right-hand columns provide an important comparison. The second from the right column compares the difference in the rise of each member's price level with the rise in Germany's price level since the community was formed as of today's available data. The second column shows the maximum divergence with Germany by country since the common currency was adopted.

In the comparison of these two columns, we see the difference between current divergences in competitiveness of member countries with Germany, the most competitive country in the euro area, and their historically greatest divergence. The difference between these two columns is a measure of progress that the euro area has made.

Let's look at the success stories. Not surprisingly, the biggest success has come from the countries that have suffered the most pain. At one time Greece's price level had risen 26.6% more than Germany's. But now Greece's price level has risen only 11.9% more than Germany's. Greece has cut its loss of competitiveness, down to something that puts it more the class of Italy or Belgium. Ireland, a county that also had undergone a great deal of turmoil, had seen a maximum divergence with Germany of 18 percentage points; that has been reduced 8.7 percentage points, a big difference.

However, apart from those two countries, progress elsewhere has been limited. Portugal has undergone a good deal of distress and has diminished its price disadvantage with Germany from 15.1% to 12.7%. Spain has reduced its divergence from 20.7% to 17.8%. This is progress, but not progress on the order that we have seen from Greece and Ireland.

In the case of Italy, its maximum divergence with Germany was 11.6%. But in the wake of all of its reforms and domestic distress, Italy has only reduced that to 10.4 percentage points. Luxembourg's divergence with Germany continues to be massive on the order of 19.2%, but for Luxembourg, that's not really a problem because it is not a manufacturing place and is a banking center so that competitiveness comparisons don't mean much for it.

In looking at these price-level comparisons, we can see that believers in the austerity plan approach can point to progress. But there has been a great deal of progress in Greece and Ireland and only some progress elsewhere. Substantial price level divergence remains in many other member countries and yet several have suffered a good deal from austerity, Spain being perhaps the best example of that. And when we look at the progress in a country like Greece, we recognize that Greece has more than halved its disadvantage versus Germany and in a relatively short period of time. But that has taken a tremendous toll on the economy and we have to wonder to what extent Greece is going to be able to keep this up.

We can see that the performance from the inception of the EMU to date is substantial compared to `worst' levels. If we look at the first column in the table, which gives us current inflation rates, we see that progress is ongoing. The German inflation rate at 0.7% is still higher than inflation everywhere else. That gap with Greece, for example, is continuing to make up ground as Greece's year-over-year inflation rate is falling by 1.8% as Germany's rises by 0.7%. Germany's economy is growing better than other economies in Europe; that's permitting it to have a higher inflation rate. However, the other economies are beleaguered and are running lower inflation rates than Germany's and rates that are low because of poor economic performance. This is not a sustainable model for progress.

At the same time, everybody in the EMU is running a lower inflation rate than the European Monetary Union target. The European Central Bank is trying to do what it can to boost inflation back up, hoping that measure will also boost growth. When we look at the line in the table that compares the EMU total inflation rate, we can see the difference between its worst divergence with Germany and its current divergence seems to be very small; it is only one percentage point. The average divergence - that is the average weighted divergence - within the EMU has only fallen by one percentage point from its worst level. And that, of course, is because Germany's divergence by definition is always zero. And it's the largest economy in the euro area. The incredible progress made by Greece counts for little because Greece is such a very small economy. In the grand scheme of things, it's very good to have Greece back on the same page or closer to the same page- at least in the same book- as Germany. But there is still much divergence in the rest of the EMU.

The table explores and reveals one of the key flaws in the construction of the European Monetary Union. That is that the ECB was given a mandate only to reach its target based upon a weighted average inflation rate. Even though there has been substantial divergence and for the most part growing divergences among the inflation rates of members right from the start of the EMU formation, no one ever paid any attention to it even though the pre-union inflation differentials were one of the biggest concerns that the monetary union's architects had. Once the union was formed, everyone acted as though that problem would go away. But it didn't. Undiagnosed cancer can be just as virulent as a cancer that is diagnosed. Not treating an existing malady does not make it better. This is the great lesson of the EMU formation.

It was hoped by members that the single currency formation and the competition created within the euro area, the harmonization of rules and regulations and the restrictions sought on fiscal policy (restrictions that proved to be a failed construct) would in fact be enough to keep inflation within the zone roughly homogeneous. But of course, even when it came to commercial policy, certain exceptions were allowed and that made cross-border competition less effective. The fiscal policy constraint was not effective at all, and that helped to set inflation differentials in place as local social welfare policies and wage policies encouraged far different things in different parts of the euro area. What has been learned is that monetary policy in a common currency isn't enough. Or at least it isn't enough unless the underlying structure and perhaps underlying economic values are far more homogeneous than what actually has existed in the euro area.

Austerity has helped to reclaim some of what has been lost. But the inflation differentials within the euro area are still only chipping away at what are substantial competitiveness differentials that have buildup since the zone's formation. It's unclear whether the countries that have suffered so much are going to be willing to continue down that path to fully reestablish their competitiveness within the zone. And it's also clear that the countries that have already undergone a good deal of austerity, but have not had much impact on improving their competitiveness versus Germany have not yet found the special sauce to bridge that gap.

As we look at the mix of progress versus stasis within the EMU. It seems that the union does not yet have the tools to achieve its goals. Union members are clinging to their desire to keep fiscal policy separate and off the table. Without fiscal transfers, good economic performance is going to depend even more upon the full restoration the price level competitiveness. That means that pressure will undoubtedly be placed on the ECB even though it has no tools to address this problem. To the extent that problems persistent they are going to continue to be addressed by the European Commission which will be trying to quash fiscal proclivity in countries that continue to trail Germany in terms of price level competitiveness. Such actions will likely breed resentment and discontent among monetary union members that will find that this pressure from the center undermines local fiscal policies and keeps them from implementing the social policy solution to the lingering domestic problems.

Let's understand that while Greece is just reported a lower rate of unemployment, both Greece and Spain continue to run enormously high rates of unemployment. Spain still has an 18% price divergence versus Germany; that is only lower by about two percentage points from its worst. While Spain has had chronically high unemployment, the additionally high unemployment hat has come from monetary union membership due to the adoption of austerity is going to make it extremely difficult for this country to maintain political stability, maintain its fiscal courses, and reduce its competitiveness gap versus Germany all of the same time. Something is going to have to give. And Spain isn't the only country with that sort of dilemma.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief