Global| Jun 13 2013

Global| Jun 13 2013EMU Inflation Continues to Wither or Plunge...

Summary

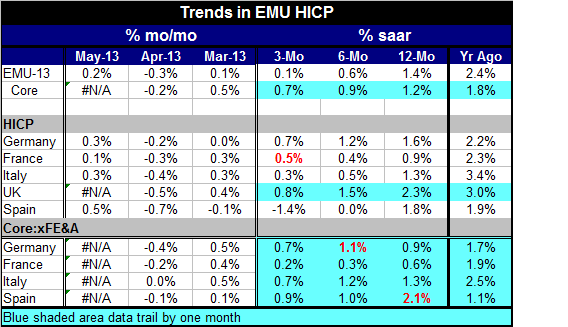

Inflation in the Eurozone rose by only 0.2% in May. Over three months the annual rate of inflation is only a 0.1% there was a steady deceleration in the growth rate of inflation from 12 months to six months to three months. Meanwhile, [...]

While the ECB is not burdened by the dual mandate that the Federal Reserve labors under it is nonetheless true that inflation continues to decline and to grow a pace that is below that which is sought by the European Central Bank (ECB). Growth in the Eurozone continues to undershoot; its overall and national unemployment rates continue to be pressured up across the zone by and large.

There is no sense denying that growth and inflation are strongly correlated. And this provides a policy dilemma particularly at times like this. The correlation between growth and inflation is negative: when growth booms inflation usually rises and when growth busts inflation usually falls. So Europe much like the United States finds itself in a situation where its growth is undershooting and its unemployment rate is rising (or too high) and its inflation rate is more than well contained. So what should policy do?

The table and the inflation charts that we present here underscore the sense in which inflation is contained across the euro-Zone even among the periphery members that have in the past had more severe inflation problems. Spain is looking forward to an alleviation of some of the austerity so that it can grow. Its inflation rate is, however, one of the higher ones among peripheral countries.

The ECB is making public arguments to the German courts that its monetary policy has been conducted legally and that its Outright Monetary Transactions have been a necessary tool to support growth in the Eurozone. However, the recent statements by Mario Draghi, head of the European central bank, suggest that he may be less sure about the actual verdict of the German courts.

Economics has long sought to come up with the proper policy mix. Most fundamentally economists study the interactions of monetary policy with fiscal policy. Europe has taken those economic findings and turned them on their head by pursuing fiscal policy with a large dose of austerity without much compensation from monetary policy. More recently, when monetary policy has sought to swerve to provide some stimulus, it has done so by treading close to the line of what the ECB charter allows it to do/and what it prohibits.

With inflation under control, and the ECB under some degree of pressure for its past actions, and with austerity being set aside to some extent within the Zone, there is some increased optimism about the prospects for growth to take hold again in Europe.

But it's always important for us to remember what the euro-Zone really is. The euro-Zone is a unification of countries that has adopted some common rules and continues to allow a great deal of national exceptions that keep the competitive forces from reaching into every corner of the Zone itself. And because of that, this zone which is truly dedicated to the stability of its currency is not functioning the way it was envisioned. Make no mistake about it, the currency union was formed and the rules were polished intentionally to tie the hands of the European Central Bank and to keep its focus on maintaining the stability of the currency. The focus is not on the elasticity of the currency. The focus was not on maintaining the growth rate in the currency area. The focus was meant to be wholly on maintaining the stability of the currency. And so now when Europe finds itself in difficult growth straits it finds also that monetary policy has very little flexibility to help and when that flexibility is pushed to its limit dissenters emerge.

The European Monetary Union is a success if we judge it on its goal which has been to form a single currency area and keep the currency stable. But the very next question is whether that has been the right goal or not...It has not so far been successful in improving and maintaining the welfare of the residents in the Eurozone in fact it has led to excesses which have caused backlashes and severe policy contractions that have fed instability political in the zone itself. Ironically one of the reasons for forming the Zone was to make Europe's politics more stable. If the initial thought was that, all good things would flow from monetary stability, that has been proved wrong.

The question now is this: "Where does Europe goes from here?" "How will it be able to reconstitute growth in areas that have been so severely afflicted?" "Can it put all of its member nations back on the same level playing field while still keeping the monetary union together?"

These are largely unanswered questions. The countries with the biggest (relative) fiscal deficits have made the biggest sacrifices and yet still have the longest way to go and are not getting the answers that they need from the countries at the core of the Zone that have fared the best and have the strongest finances.

There is no doubt that the architecture of the Zone has had flaws. EMU members are doing what they can now to try to combat these flaws and are moving forward under improved rules. But is no consensus on how to deal with the damage that has been done and that also impedes the ability to move forward.

For the time being, inflation remains a nonissue in terms of its level, and its momentum. Growth is still lacking, although some backing off on austerity seems to be paving the way for growth to reignite. But the period of turmoil and austerity has brought such backlash that it's unclear the extent to which the lessons of excess have been learned or if pent-up demand and the desire for retribution will interfere in the ability of the Zone to right its ship. The near-term is looking brighter; longer outlook continues to be challenged.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief