Global| Nov 10 2014

Global| Nov 10 2014EMU Industrial Sector Shows Mixed Trends Across Members

Summary

Industrial trends in the European Monetary Union remain mixed in September. Of the 10 reporting countries, four of them showed declines in industrial production. Six countries show increases and four those have increases that are 1% [...]

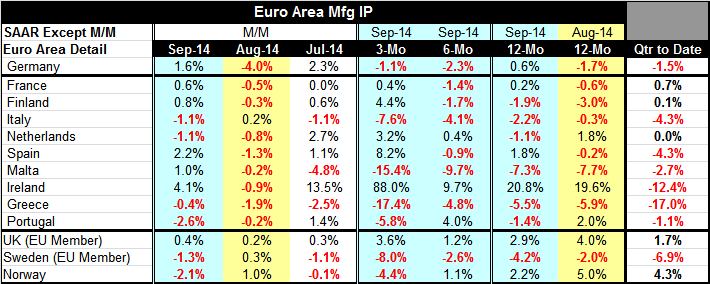

Industrial trends in the European Monetary Union remain mixed in September. Of the 10 reporting countries, four of them showed declines in industrial production. Six countries show increases and four those have increases that are 1% or more. Ireland has an IP increase of 4.1% in September and Spain has an increase of 2.2%. There is some good news lurking in September. It may be the light at the end of the tunnel, but it's still not the end of the tunnel. In the quarter to date, that is now the completed third quarter, industrial production is rising in only two of these countries, is declining in seven of them, and is flat in one other. France has the largest annualized increase, 0.7%. Finland has eked out a 0.1% increase in the quarter. The remaining countries show output declines in Q3 2014.

Industrial trends in the European Monetary Union remain mixed in September. Of the 10 reporting countries, four of them showed declines in industrial production. Six countries show increases and four those have increases that are 1% or more. Ireland has an IP increase of 4.1% in September and Spain has an increase of 2.2%. There is some good news lurking in September. It may be the light at the end of the tunnel, but it's still not the end of the tunnel. In the quarter to date, that is now the completed third quarter, industrial production is rising in only two of these countries, is declining in seven of them, and is flat in one other. France has the largest annualized increase, 0.7%. Finland has eked out a 0.1% increase in the quarter. The remaining countries show output declines in Q3 2014.

There is also the recent history to consider which puts September in a slightly weaker perspective. September is in some sense a rebound from a very weak August in which nine of 10 of these member countries saw industrial output fall. The lone IP rise, 0.2%, was from Italy. Over three months, industrial output is falling in half of the reporting members and rising in half of the members. Over six months, industrial production is falling in seven of 10 members. Over 12 months, industrial output is falling in six of 10 members. The trends are clearly on the side of declining rather than expanding although September by itself shows some promise.

Italy and Malta are the only two countries showing secularly deteriorating declines in industrial output. Finland and the Netherlands show sequential acceleration. The rest of the members fall in the middle, demonstrating mixed growth patterns.

Turning to the members of the European Union that are not members of the single currency area, we also see mixed patterns. The U.K. shows steady positive but not accelerating growth rates. Sweden shows steady negative but not decelerating growth rates. Norway shows growth rates turning from positive to negative and displays sequential deterioration.

European economic data continue to be uneven and for the most part, are indicating some additional slippage. The geopolitical situation in Ukraine seems to be more dangerous with news that Russia has moved a column of tanks into Ukraine's adjacent regions controlled by rebels. That move, made several days ago, has not yet led to any action. But in recent reports, Russia's central bank is admitting the economic damage that has been done by sanctions. The more that it becomes clear that sanctions are damaging Russia, the more dangerous Russia becomes because the more likely it is that Russia might decide that it has nothing to lose from stepping up the hostilities or its land-grab in Ukraine. Europe continues to face deteriorating economic conditions and heightened geopolitical risks; it's not a good combination.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief