Global| Jun 29 2021

Global| Jun 29 2021EMU Indexes: a 20-Year High in June

Summary

The EU Commission indexes have been making a huge move to higher ground for the last several months. In June we are looking at the highest EU Commission index for the EMU in over 20 years. This should help to establish the case that [...]

The EU Commission indexes have been making a huge move to higher ground for the last several months. In June we are looking at the highest EU Commission index for the EMU in over 20 years. This should help to establish the case that these indexes are forward-looking and aspirational since (for example) unemployment rates are still elevated and not back down to even their recent lows. A 20-year high in the EMU index reflects optimism more than achievement.

The EU Commission indexes have been making a huge move to higher ground for the last several months. In June we are looking at the highest EU Commission index for the EMU in over 20 years. This should help to establish the case that these indexes are forward-looking and aspirational since (for example) unemployment rates are still elevated and not back down to even their recent lows. A 20-year high in the EMU index reflects optimism more than achievement.

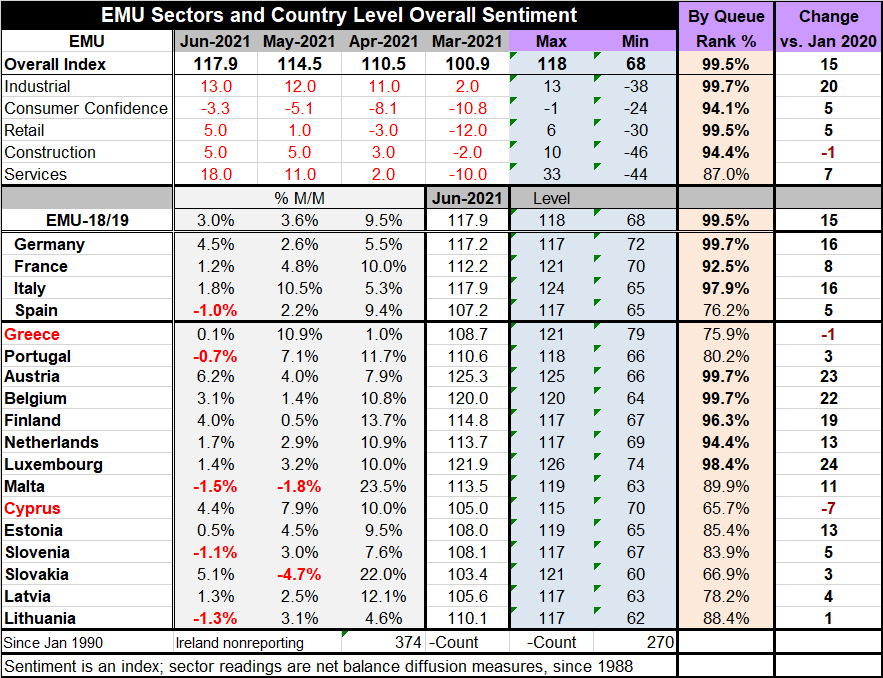

Of the five individual metrics of EMU health, only the services sector in June has a rank standing below the 90th percentile. However, it does produce a still impressive 87th percentile standing.

Since January 2020, all these sector readings are higher except construction where the reading is lower by one point but it still registers a 94.4 percentile standing. Unlike other sectors, construction was exceptionally strong when the virus struck. The industrial sector now is up the most since January 2020 on a gain of 20 points.

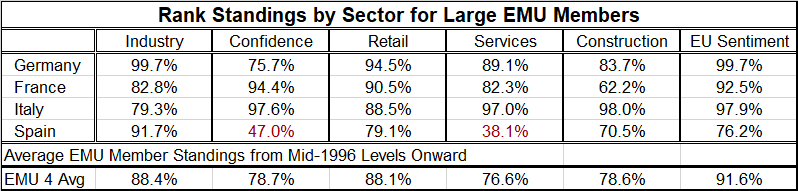

Looking across reporting EMU members, it has been a time of exceptional strength. In June only five countries backtracked; that was after only two had backtracked in May and after none had backtracked in April. Among the four largest EMU economics, in the last three months only Spain has backtracked in one of those months; that's one decline out of 12 opportunities.

Of the eighteen early reporting EMU members, eight have standings in their own ninetieth percentiles. There is enough strength up and down the line that the EMU ranking is in its top one-half of one percentile. That is because of the uniformity of strength. The weakest rankings are at the 65.7 percentile (Cyprus) and the 66.9 percentile (Slovakia). There are three in the 70th percentile decile and five in the 80th percentile decile.

Table 1: Overview

The overarching sentiment gauges have the highest average score among all sector readings. This is an admission that the collection of strength that is spread across the region exceeds the intensity in any individual sector. Among sectors, industry has the highest average standing followed closely by retail. Confidence, construction and services are behind those two and are closely clustered. The service sector has made up a lot of ground and has made the strongest gain of any sector over the last three months, but its ranking lags slightly.

Table 2: Sectors

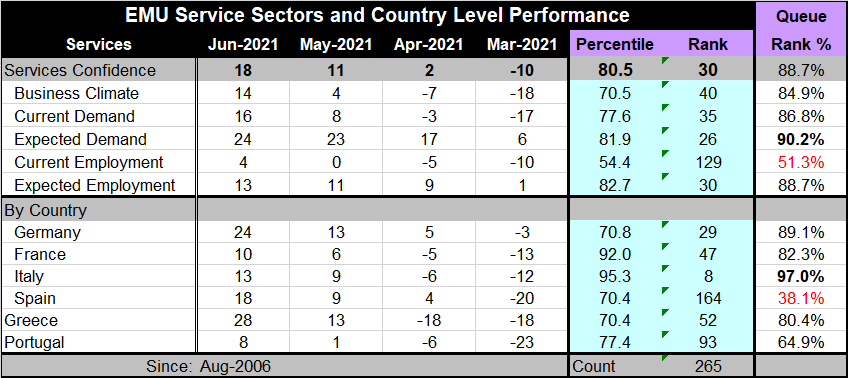

The service sector detail tells about where the strength is coming from. The detail on that sector shows that expected demand has a 90.2 percentile standing. Compare that to current demand at a still-strong 86.8 percentile standing. The current business climate is at an 84.9 percentile standing. But current employment is only at a 51.3 percentile standing. This contrasts with expected employment at 88.7 percentile standing. The strength here is well rounded, but there is clearly more strength in expectations and still lingering traces of weakness in current conditions. In this way, the EMU readings are out in front of reality and are built on hope and expectations.

It is the step up in the services sector that makes the biggest difference in recent months. And it will make the biggest difference in the evolution of recovery too since jobs are needed to fill in the holes. And while the services sector is the best one to do that, we see in the services detail there is more hope than actual jobs in the sector's current performance.

Table 3: Services

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief