Global| Aug 14 2009

Global| Aug 14 2009EMU HICP In Large Yr/Yr Drop

Summary

The EMU HICP fell by a larger than expected 0.7% Yr/Yr. But with France and Germany emerging from recession in yesterday’s GDP reports, markets are not focused on inflation being under control or worried about deflation with the Yr/Yr [...]

The EMU HICP fell by a larger than expected 0.7% Yr/Yr. But with France and Germany emerging from recession in yesterday’s GDP reports, markets are not focused on inflation being under control or worried about deflation with the Yr/Yr drop, but instead worried that inflation is going to be a problem sooner rather than later. Isn’t that just like markets? Nothing is what is seems.

Forecasts made up to this point have been assuming that Europe was going to remain weak for some time. Now with the early exit from recession by Germany and France and the small drop in EMU GDP in 2009-Q2, inflation forecasts are beginning to get a re-think.

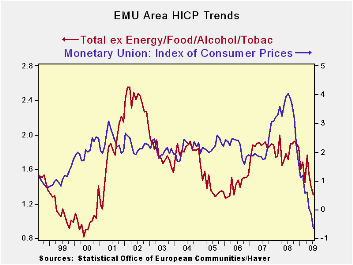

Ex food and energy inflation in EMU is at +0.6%. The core measure of inflation was flat in July, up by 0.1% in June and flat in May. There isn’t exactly any news saying inflation is building momentum here.

Moreover, although Germany and France have ‘existed recession’ they have done so in a most peculiar way. And before calling it the ‘end of recession’ perhaps we should wait and see what has been cooked into its GDP stew. As we pointed out in the write–up of European GDP yesterday, the diffusion indicators that track the various sectors across European nations and in EMU are still at very depressed levels. This has to conjure up concerns of what ether GDP rose upon in Q2 and if those fumes will still have lifting force in 2009-Q3.

In short, it seems a bad time to start to raise inflation forecasts and fears. The EMU-wide HICP is in a strong drop; it is not covering for any inflation under the surface and the surprising growth served up by several European economies is equally surprising after the fact as we try to understand it. Is that real and is it really a basis for concerns about STRONG growth?

The bottom line is that inflation is under control in Europe and barring something exceptional - that we have not yet seen -- it should stay that way.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % Mo/Mo | % Saar | ||||||

| Jul-09 | Jun-09 | May-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | -0.3% | 0.3% | 0.0% | -0.2% | 0.2% | -0.7% | 4.0% |

| Core | 0.0% | 0.1% | 0.0% | 0.6% | 1.3% | 1.2% | 2.5% |

| Goods | -1.7% | 0.2% | 0.1% | -5.5% | -0.1% | -2.4% | 5.1% |

| Services | 0.8% | 0.1% | 0.1% | 4.1% | 3.7% | 1.9% | 2.6% |

| HICP | |||||||

| Germany | -0.5% | 0.5% | -0.2% | -0.7% | -0.2% | -0.7% | 3.5% |

| France | -0.1% | 0.2% | 0.0% | 0.3% | 0.3% | -0.8% | 4.0% |

| Italy | -0.6% | 0.3% | 0.0% | -1.1% | 0.7% | -0.1% | 4.1% |

| Spain | 0.1% | 0.4% | -0.1% | 1.7% | 0.3% | -1.4% | 5.3% |

| Core:xFE&A | |||||||

| Germany | 0.1% | 0.2% | -0.1% | 0.8% | 1.7% | 1.1% | 1.8% |

| Italy | -0.4% | 0.1% | 0.1% | -0.7% | 1.3% | 1.3% | 2.8% |

| Spain | 0.2% | 0.2% | 0.0% | 1.3% | 0.5% | 0.7% | 3.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief