Global| Oct 15 2009

Global| Oct 15 2009EMU HICP Drops in September Core Rate Remains in Subdued Trend

Summary

The EMU HICP fell by 0.1% m/m in September. The 12-month pace for headline inflation was -0.3%. The headline rate has not increased Yr/Yr since April. Headline inflation is choppy at a low level. Core inflation has been very steady at [...]

The EMU HICP fell by 0.1% m/m in September. The 12-month pace

for headline inflation was -0.3%. The headline rate has not increased

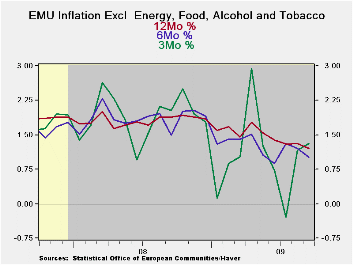

Yr/Yr since April. Headline inflation is choppy at a low level. Core

inflation has been very steady at a 1.1% pace; it barely ticked up to

1.2% over three months in Sept.

In EMU goods sector inflation has been falling under the influence of

weak oil prices aided by the impact of a rising euro exchange rate.

Services prices have been steady at 1.8% but over the recent three

months service sector inflation stepped down to a 1.3% pace.

The headline inflation trend across selected large EMU nations shows

subdued rates. Spain and France show a hint of inflation acceleration

in their sequential growth rates. Spain’s 1.9% 3-month pace is the

highest in this group.

Core inflation is both stable and low across the large EMU countries.

Italy alone shows some hint of acceleration with a core inflation pace

of 1.9% over three months up from what has generally been a 1.5% pace

for core inflation there.

On balance inflation, inflation trends inflation dynamics and inflation

fundamentals appear to be very well contained in the zone. We see the

inflation readings and trends above. The dynamics do not show wages or

prices getting out of control across the economy. The fundamentals show

constrained money and credit growth, lots of economic slack, as well as

a rising exchange rate. There is little ground for the ECB to be

inflation wary. The increases in global commodity prices have been well

blunted by euro strength Vs the dollar.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % SAAR | ||||||

| Sep-09 | Aug-09 | Jul-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU | -0.1% | 0.5% | -0.3% | 0.8% | 0.8% | -0.3% | 3.6% |

| Core | 0.0% | 0.2% | 0.0% | 1.2% | 1.1% | 1.1% | 2.5% |

| Goods | 0.5% | 0.4% | -1.7% | -2.9% | -0.2% | -1.8% | 4.4% |

| Services | -0.7% | 0.2% | 0.8% | 1.3% | 1.8% | 1.8% | 2.6% |

| HICP | |||||||

| Germany | -0.3% | 0.7% | -0.5% | -0.4% | 0.4% | -0.5% | 3.0% |

| France | -0.1% | 0.5% | -0.1% | 1.1% | 0.7% | -0.4% | 3.4% |

| Italy | 0.4% | 0.5% | -0.6% | 1.1% | 1.5% | 0.4% | 3.9% |

| Spain | -0.3% | 0.7% | 0.1% | 1.9% | 1.4% | -1.0% | 4.6% |

| Core excl Food Energy and Alcohol | |||||||

| Germany | -0.2% | 0.4% | 0.1% | 1.1% | 1.3% | 1.0% | 1.7% |

| France | -0.1% | 0.3% | 0.1% | 0.8% | 1.0% | 1.2% | 2.3% |

| Italy | 0.4% | 0.5% | -0.4% | 1.9% | 1.5% | 1.5% | 3.0% |

| Spain | -0.1% | 0.1% | 0.2% | 0.7% | 0.7% | 0.3% | 3.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief