Global| Aug 13 2009

Global| Aug 13 2009EMU GDP Falls But French And German GDP Rise

Summary

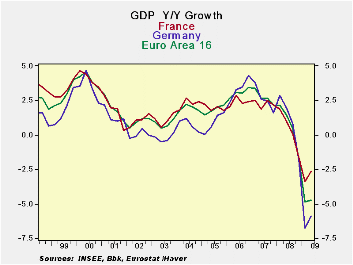

European growth figures continue to be weak when we log the indicators month by month but if instead we complete a formal GDP presentation, Germany and France have exited recession while the EMU GDP drop is only -0.1% in Q2 of 2009, a [...]

European growth figures continue to be weak when we log the

indicators month by month but if instead we complete a formal GDP

presentation, Germany and France have exited recession while the EMU

GDP drop is only -0.1% in Q2 of 2009, a drop at an annual rate of

-0.4%. EMU’s GDP decline in Q2 is less than the drop in the US but

Europe’s Yr/Yr decline has been worse at -4.7% compared to the US

year-over-year loss of -3.9%.

In the US the Fed is less downbeat - At

its meeting yesterday the Fed implied that the recession in the US was

ending but did not take the step of saying in any clear voice that

recovery was beginning. It issued in a vague voice the statement saying

that activity was leveling off. In Q2 some of Europe, at least, is

doing better than that.

GDP as the standard - The contrast

between what GDP sees and what monthly indicators show is an important

one to keep in mind. GDP accounting has its peculiar elements. Fewer

imports boost GDP even though there is no direct impact on domestic

output (there is less bought from abroad and so fewer payments made to

foreigners- all things equal fewer imports mean higher sales by

domestic agents for the same GDP). And inventories cut at slower pace,

add to GDP growth even though they are still being cut.

Indicators can lag - Jobs tend to trail

activity shifts so the economy will be in recovery before job growth is

even positive. In the case of Europe its purchaser induces and the EU

Economic indicators from the EU Commission are woefully weak and seem

inconsistent with the notion that the recession is ending even if just

in Germany and France. But that is the way recessions sometimes end.

Indicators really do lag in this cycle -

To put it differently early recovery periods often do not look very

different from end recession periods. That is not surprising because

they are chronological neighbors. What makes recovery so different is

where it is headed compared to the recession period. Even so, the

indicators of economic performance in Europe are uncharacteristically

weak for the recession to be ending. Even those in Germany and in

France are lacking. The GDP rebounds hardly seems like they can be from

the same countries as the ones that have produced the indicators they

have up to mid-year.

What indicators have been telling us- To

begin with we have no detail on GDP in Europe just the few things that

might be said at press conferences where the data are released.

Industrial data in EMU as well as in Germany and France, in particular,

continue to be very weak. The German and French economic sentiment

readings which are a weighted average of the EU Commission’s underlying

sector indices rank in the bottom 20th percentile of their respective

rage of values. The German and French readings are up about 10% or so

from their weakest readings in the recession on this score. The EU

Commission indices are from underlying diffusion data. All continue to

show deep contractions across are all sectors. Germany and France show

GDP that is rising, nonetheless. Apparently the change in the EMU index

is more important that the level of the index even though it is a

diffusion index that has to turn positive to signal sector growth and

all sectors industrial, retail, services, construction and consumer are

weak.

German’s IFO - Germany has its own IFO

survey with a diffusion component and for July its services reading

just barely turned positive.

More indicators - The NTC/Markit readings

are ISM type readings where a level above 50 denotes expansion. For EMU

in June the NTC reading stood at 42.4 for MFG and 44.5 for Services.

Both of these indices register declines as they are below 50. For

Germany, an economy that is showing positive GDP growth in Q2, its

NTC/Market diffusion index stood at 40.8 and was ins the bottom 40

percentile of its range of readings. France at 45.9 also signaled a

declining MFG sector but its index was closer to neutral standing in

the 49th percentile of its range, despite its low raw diffusion level.

The service sectors in France and Germany were weak in June as well,

with raw diffusion readings 45 and 47 respectively. Those readings

ranked in the lower third of each country’s respective historic

experience.

GDP does not seem to have widespread support -

In short the industrial data and service sector data we have do not

confirm the message from GDP in EMU. We could go through a litany of

consumer confidence data as well, as they are weak too. If Europe is

recovering (France and Germany, any way) it must be the government

spending that is boosting the economy coupled with lower imports and

inventories that are being cut by less than before –all these are what

I would terms passive augmentations of GDP. The active augmentation

from more consumer spending and more business investment has not begun.

Inventories are likely adding to GDP growth but not by actively being

built.

Exports and government are probably the main drivers -

We have seen episodic country reports that have revealed exports have

begun to rise. So the economies that are in recovery may now be firing

on two cylinders exports and the government sector. It’s not a very

wide base for growth yet. But it is also the support within EMU that is

helping to cut the drop in the formal measure of GDP. Progress is being

made but it does look like the sort of progress that usually marks the

ends of recessions. Too many European, German and French sectors are

just too weak.

| E-Area and main G-10 country GDP Results | |||||||

|---|---|---|---|---|---|---|---|

| Quarter over quarter-Saar | Year/Year | ||||||

| GDP | Q2-09 | Q1-09 | Q4-08 | Q2-09 | Q1-09 | Q4-08 | Q3-08 |

| EMU-15 | -0.4% | -9.7% | -6.9% | -4.7% | -4.9% | -1.7% | 0.5% |

| Austria | #N/A | -3.3% | -3.9% | #N/A | -3.4% | 0.2% | 2.0% |

| France | 1.4% | -5.3% | -5.5% | -2.6% | -3.4% | -1.6% | 0.1% |

| Germany | 1.3% | -13.4% | -9.4% | -5.9% | -6.7% | -1.8% | 0.8% |

| Greece | 1.3% | -4.7% | 1.2% | -0.2% | 0.3% | 2.4% | 2.7% |

| Italy | -1.9% | -10.3% | -8.3% | -6.0% | -6.0% | -3.0% | -1.3% |

| The Netherlands | -3.4% | -10.3% | -4.1% | -4.9% | -4.2% | -0.8% | 1.7% |

| Portugal | #N/A | -6.2% | -7.1% | #N/A | -3.7% | -2.0% | 0.3% |

| Spain | #N/A | -7.4% | -3.8% | #N/A | -3.0% | -0.7% | 0.9% |

| UK | -3.1% | -9.2% | -7.0% | -5.6% | -4.9% | -1.8% | 0.5% |

| US | -1.0% | -6.4% | -5.4% | -3.9% | -3.3% | -1.9% | 0.0% |

| Japan | #N/A | -14.2% | -13.5% | #N/A | -8.4% | -4.4% | -0.3% |

| Switzerland | #N/A | -3.2% | -2.2% | #N/A | -1.6% | -0.4% | 1.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief