Global| Nov 14 2014

Global| Nov 14 2014EMU GDP Edges Higher Or, Yes, We Have No Recession

Summary

European growth data for the third quarter provided a much-needed upside surprise. The European Monetary Union grew in the third quarter and Germany avoided a second consecutive quarter of decline by rising by 0.3%. Among the EMU [...]

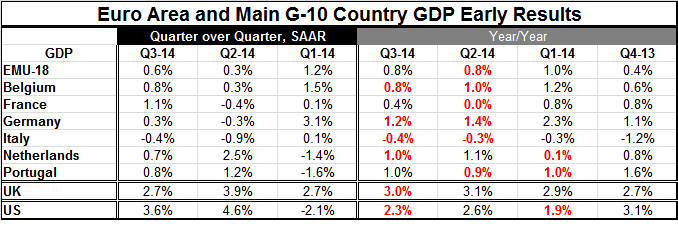

European growth data for the third quarter provided a much-needed upside surprise. The European Monetary Union grew in the third quarter and Germany avoided a second consecutive quarter of decline by rising by 0.3%. Among the EMU early-reporting countries in the table, only Italy has a GDP decline in the third quarter, its second drop in a row.

European growth data for the third quarter provided a much-needed upside surprise. The European Monetary Union grew in the third quarter and Germany avoided a second consecutive quarter of decline by rising by 0.3%. Among the EMU early-reporting countries in the table, only Italy has a GDP decline in the third quarter, its second drop in a row.

The EMU PMI sector gauges had been telling us that the private sector was perhaps slow but expanding in the third quarter and that appears to be borne out by the GDP reports.

Even so, the good news is not great. If it's `good news', it's small good news. Of the six early reporting EMU members, four of them show that GDP growth has slowed in the third quarter compared with growth in the second quarter using year-over-year growth rates. The countries that have improved on that basis are France and Portugal, with Portugal accelerating ever so slightly to a 1% growth rate from a 0.9% growth rate. France has made a more substantial rise to 0.4% from 0%, but France obviously still is quite weak with a year-over-year growth rate of less than one-half of one percentage point. In addition, for that same group of six countries, there has been a deceleration for five of six of them in the second quarter as well. So we now have two quarters in a row where GDP growth is decelerating on a relatively widespread basis for some key euro area members.

Even the U.S. and the U.K., whose performances are compared at the bottom of the table, show some growth deceleration for third-quarter year-over-year growth compared to second-quarter growth. But for the U.K. that deceleration is technical, a drop to 3% from 3.1%. Moreover the U.K. has a growth rate of 3%, which is fairly substantial. The U.S. has a more substantial slowdown from 2.6% to 2.3%, but it still is logging better than 2% growth in the third quarter, better than any of the early reporting EMU members in the table above it.

Sometimes we take as good news, news that simply isn't as bad as what we had expected. And I think that applies to this circumstance. Looking at the chart, you can see that the U.K. has had a real lift off in GDP. That seems to continue. On the other hand, Germany has had a liftoff that is fading and French GDP resembles the path of a stone skipping across the water with the amplitude of each rebound more suspect than the one before it.

What Europe has going for it is that the central bank to trying to do it can to spur growth, although not all European members are on board for the kind of stimulus that the European Central Bank seems to be willing to attempt. Europe will be helped in the coming months, like most countries in the world, by lower oil prices, which will put money back in the pockets of consumers, but that will also be adverse to the central bank's efforts to boost inflation back up to its target zone.

The unstable situation in Ukraine and the role of Russia there continues to cast a pall across the prospect for geopolitical stability in Europe. The upcoming summit will put world leaders directly in contact with Vladimir Putin and perhaps something good will come of it, although the odds are against it. Putin has been defiant and now his economy is being damaged even more than he wants to admit by sanctions; he is looking to get more to compensate for his suffering - not to give in. This is an increasingly dangerous situation. Russian destabilization of Ukraine is likely to continue and to worsen and Russia is likely to continue to deny involvement.

As we documented in yesterday's report that focused on price level differences that have developed around the European Community, Europe continues to struggle with regional issues related to differing regional inflation rates and differing degrees of competitiveness. There also are different levels of fiscal health around the community. At this time when some fiscal laxity would be a great help, Germany, the country with the most flexibility to have some fiscal laxity, has instead decided to continue to make even more progress on its own budget and fiscal standing.

The IEA today warned that there's been a regime change, and that there are likely to be low oil prices for the foreseeable future owing to the increases in energy supplies and to the slowed growth in China. An environment of slower growth could mean a milder in future for all commodity prices. Central bankers are going to have to be careful to operate in this new environment where the new needs of the economies may be for lower rates than what central banks have been traditionally comfortable.

While conservatives continue to fear that all the operations of quantitative easing around the world could ignite some huge bonfire of inflation, with the new approach to bank regulation, it seems to me that the greater risk is still that growth will underperform rather than to become excessive and create inflation. That's another way of saying that we have transitioned out of a period of recession and financial chaos into a new period where we are still dealing with the issues from the financial crisis. Some of them we are still in the process of fixing. We have yet to transition into times that are truly normal. When we make that final transition, central banks will have to be more vigilant. Many seem to think that that event is right around the corner. However, I think it may still not much farther down the road.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief