Global| Jan 31 2020

Global| Jan 31 2020EMU GDP Disappoints in Q4 While the Virus Goes Viral

Summary

The preliminary GDP results are in for early EMU GDP reporters. The results are not good. I have presented the Q/Q results as compounded growth rates as they are usually presented in the U.S. Europeans tend to report the simple Q/Q [...]

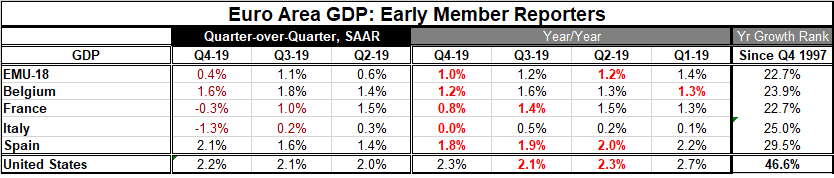

The preliminary GDP results are in for early EMU GDP reporters. The results are not good. I have presented the Q/Q results as compounded growth rates as they are usually presented in the U.S. Europeans tend to report the simple Q/Q percentage change. But if one wants to compare GDP growth in Q4 to their recent pace, annualization is the answer. The table presents compounded annualized growth rates. The far right column ranks the current year-over-year growth rate among all year-on-year grow rates quarterly back to end-1997. All EMU early reporters have growth rates in the bottom quartile of results on that timeline except for Spain whose growth is in its 29.5 percentile, only slightly higher. U.S. growth is just under its median result for this period (just below a 50% standing). Only Spanish and EMU results show clear trends and they are both trending lower over the past four quarters, sequentially using year-on-year data. On quarterly data, Italy and France are trending lower over the past three quarters; Spain is trending higher.

The preliminary GDP results are in for early EMU GDP reporters. The results are not good. I have presented the Q/Q results as compounded growth rates as they are usually presented in the U.S. Europeans tend to report the simple Q/Q percentage change. But if one wants to compare GDP growth in Q4 to their recent pace, annualization is the answer. The table presents compounded annualized growth rates. The far right column ranks the current year-over-year growth rate among all year-on-year grow rates quarterly back to end-1997. All EMU early reporters have growth rates in the bottom quartile of results on that timeline except for Spain whose growth is in its 29.5 percentile, only slightly higher. U.S. growth is just under its median result for this period (just below a 50% standing). Only Spanish and EMU results show clear trends and they are both trending lower over the past four quarters, sequentially using year-on-year data. On quarterly data, Italy and France are trending lower over the past three quarters; Spain is trending higher.

Do you feel lucky?

Weak growth is in hand, the coronavirus is stirring up trouble, Brexit is now in progress and trade conflicts are still percolating… A phrase from the movie Dirty Harry comes to mind...Do you feel lucky today...?

That is the question for policymakers. Can they sit back and let growth slip into gear and drive off into the sunset. Or is growth already weak, is the economic environment uneven and does the introduction of the coronavirus rob them of the ‘luck’ they thought would come their way with the conclusion of the U.S.-China phase-one trade pact?

Feelin’ alright? Not feelin’ so good myself

Today’s news on the coronavirus brings reports of new infections. England has reported its first two infections. Authorities in Wuhan say how hard it is still to contain the virus. There is optimism on prospects for developing a vaccination for it ‘soon.’ But for now the virus is still spreading and it is upsetting the global supply chain. WHO has finally declared a global health emergency. Flights to China are being stopped. Moody’s has warned of the impact on the global supply chain. Hyundai, Sangyong Motor, and Electrolux have indicated that they would be closing plants to deal with supply disruptions. Peugeot Citroen has three plants in Wuhan that it will close until February 14 (Source).

Danger Will Robinson Danger! Danger!

How bad? How dangerous? Travel warnings for China from the U.S. Department of State put the level of warning as equal to that for travel to Iraq and Afghanistan.

Speaking of disruptive…Virus trumps Trump

The virus could turn out to be far more disruptive that the Trump trade tariffs since tariffs allow goods to flow but attach a price penalty. When a virus causes shut downs to operations, the flow of merchandise comes to a halt. That is much more disruptive.

The flow of data continues uneven

The flow of data continues uneven

Life goes on despite weak GDP and a nasty potentially killer-virus. While yesterday the daily luck-of-the-draw seemed to provide some reports that were more upbeat, today’s reports are far more sobering. The Baltic freight index continues to drop-- a very bad sign since this index is updated daily. It reflects demand for shipping in the most up-to-date manner possible and its signal is weak and weakening. In addition to weak EMU GDP, both French and Italian GDP declined in Q4. Both of those events were unexpected. German retail sales fell in December and by more than expected. China’s manufacturing PMI ticked a bit lower to register a dead neutral 50.0 diffusion value. Given all the upset in the region, that is an ‘upside’ surprise to me.

As always, daily data releases ebb and flow. The U.K. showed a rise in consumer confidence. South Korean industrial production (IP) expanded. In Japan, IP rebounded and gained back more than it lost last month. Japan’s retail sales ticked higher but fell year-over-year. The daily grind of data is simply the daily grind of data, but on balance the news on the global economy is not favorable.

Rock, paper, scissors meets coronavirus, earnings, and the Fed

Markets are still selling stock off as coronavirus news is for now trumping what had been some good earnings news. The Fed Chairman’s remarks this week amounted to little more than an acknowledgement that the Fed knows that this virus is a factor. The Fed gave us no sense of how it had changed its own outlook or plans if it did so at all. What did change is that Powell did not say that the economy was in ‘a good place,’ a phrase that the Fed had been using persistently and was as conspicuous in its absence from Powell’s press conference as Sherlock Holmes’ famous ‘dog that did not bark.’ It’s one thing to bark up the wrong tree and another to not bark at all.

A side order of corona with everything

I have been injecting information on the coronavirus developments in everything I have written recently. I think it is important. That is not to dismiss other data or events but to point out that corona-related developments could completely change the signal from the flow of data we are seeing. I am not really arguing that we should ignore incoming data or only pay attention to a signal that is weak. But strong signals might easily be reversed. And weak signals might be (or might have been) amplified by the corona-effect.

Learning what we can from GDP

In the meantime, data have not been robust and the Q4 European GDP reports are not good news. While the U.S. Q4 GDP report was better than most expected, it was ‘bailed out’ by plunging imports which are not a good sign. Imports are the function of relative prices and domestic demand- plus shocks if there are any. There were no Q4 shocks. There may have been some lead-and-lag effects due to tariffs and the coming important Christmas selling season, however. Price developments generally filter though slowing and bend trend lines they don’t break them. Changes in domestic demand can shift import demand much more abruptly. There was in the U.S. a sharp pull back in inventory building in Q4. And since many consumer goods are imported in the U.S., a pullback in inventories could also cause a pull-back in imports. When that happens, the impact in GDP is muted since falling inventories reduce GDP but falling imports boost GDP. However, if imports are weak because of weakening domestic demand, that has a convoluted impact and signal since weak demand reflects weak GDP but it makes GDP stronger though the import channel as a feedback effect of sorts! For this reason, the U.S. Q4 GDP result is something to keep a close eye on. If imports plunged because of a one-off inventory adjustment, that’s not a problem. But if demand for inventories weakened because overall demand is weakening, the drop in imports would be a sign of more weakness to come. While so many international gauges show trade-flow weakness, it would be foolish not to pay attention to U.S. import weakness or to ignore the very weak Baltic freight index. But beware. They are not the same things, since the Baltic index is up-to-date to end-January while GDP is about trends set over October, November and December of last year. Maybe those trends will turn… Do you feel lucky?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief