Global| Nov 17 2014

Global| Nov 17 2014EMU Exports Revive and Surplus Grows

Summary

The trade surplus in the European Monetary Union rose to 17.7 billion euros in September from 15.4 billion euros in August. Exports rose 4.2% in September after a 1.4% decline a month earlier. Imports also revived, rising by 3% after [...]

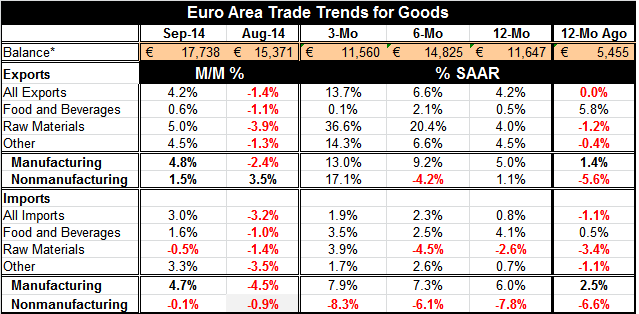

The trade surplus in the European Monetary Union rose to 17.7 billion euros in September from 15.4 billion euros in August. Exports rose 4.2% in September after a 1.4% decline a month earlier. Imports also revived, rising by 3% after a 3.2% August decline.

The trade surplus in the European Monetary Union rose to 17.7 billion euros in September from 15.4 billion euros in August. Exports rose 4.2% in September after a 1.4% decline a month earlier. Imports also revived, rising by 3% after a 3.2% August decline.

Over one year, exports are expanding by 4.2% as imports have been limited, rising by only 0.8%. Sequential growth rates from 12 months to six months to three months point to steady acceleration of exports. Exports are expanding at a 13.7% pace over three months after rising at a 6.6% annual rate over six months and by 4.2% over 12 months. Imports also have revived, over the period, but are not steadily accelerating; their three-month growth rate is 1.9%, down from 2.3% over six months but up from 0.8% over 12 months. The European Monetary Union's exports seem to show continued vitality while imports continue to struggle.

If we divide trade flows between manufacturing and nonmanufacturing, manufactured exports continue to show robust acceleration from 12 months to six months to three months, with the three-month manufacturing export growth rate climbing steadily to 13%. Nonmanufacturing exports also accelerate from 12 months to three months but not sequentially.

Manufacturing imports also show to a steady acceleration to 7.9% over three months from 7.3% over six months and 6% over 12 months. While that is a technical acceleration, it's a little bit more like steady import growth. Nonmanufacturing imports, on the other hand, are contracting, showing consistent negative growth rates of -8.3% over three months, -6.1% over six months and -7.8% over 12 months.

Europe's trade flows on balance show steady if unspectacular demand for imports when we look at manufacturing trade. In looking at overall trade, we lose this pattern because of weak and erratic nonmanufactures' imports. Still, the pattern in manufacturers' imports is somewhat reassuring about the state of growth in Europe. While purchasing manager surveys for Europe have continued to be quite weak, third quarter GDP showed that in the EMU GDP has still been growing. However, Europe looks like it continues to thrive off of export-led growth. Europe's exports to the rest of the world continue to exceed and to outpace its imports and yet the euro continues to drop. This means that Europe, which is already in a position of surplus, is going to have an increasingly larger surplus and is going to continue to take domestic demand from the rest of the world rather than to contribute to it. Europe's trade surplus at 17.7 billion euros compares to the 12-month average of 11.6 billion euros, a considerable step up.

News that Japan has posted its second consecutive quarter of contraction has been destabilizing to Japanese markets and has reverberated throughout the markets around the world. Japan already had a huge decline in GDP when its sales tax hike took effect. Negative growth was not expected to persist. We find this as the global situation: China is slowing. Japan sinking and Europe is stuck in a morass from which it is continuing to grow through its dependency on external demand.

This is not a very good prescription for continued world growth. The U.S. economy may be growing faster than Europe, but it still is not doing all that well and the rising dollar will tend to undercut and possibly to destabilize U.S. growth. At the conclusion of the G-20 summit, leaders made some vague promise to stimulate growth but it's not clear that this is really going to happen, especially not in Europe where there continues to be such focus on austerity. Japan, however, appears to have been truly frightened by its second consecutive quarter of contraction and appears to be ready to give back some of its fiscal progress in order to be sure that there isn't backsliding on growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief