Global| May 22 2013

Global| May 22 2013EMU Current Account Spurts...Oh My!

Summary

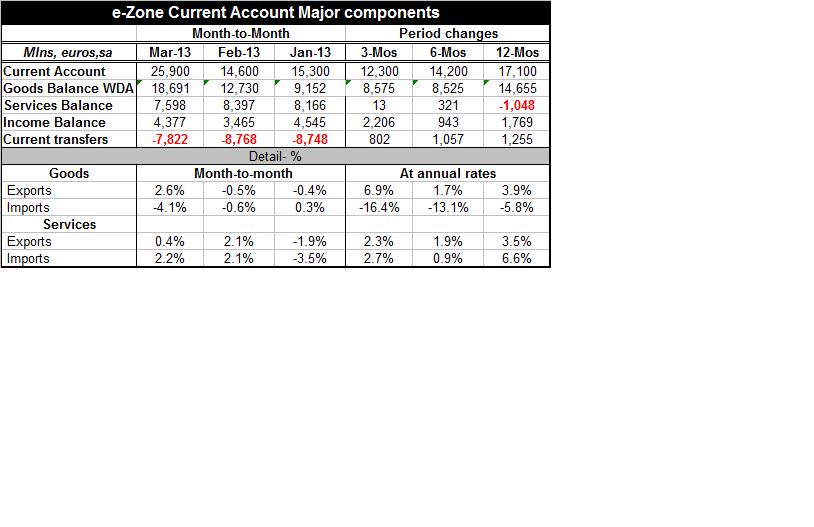

The European Monetary Union (EMU) current account surplus jumped to 25.9 billion euros in March from 14.6 billion euros in February. The surplus is the largest on record since the Union was formed. While there are some countries in [...]

Or, How Can Such 'Good News' Be So Bad?

The European Monetary Union (EMU) current account surplus jumped to 25.9 billion euros in March from 14.6 billion euros in February. The surplus is the largest on record since the Union was formed. While there are some countries in the monetary union looking for some relief from their suppressed growth conditions by weakening the euro, this huge spurt in the current account makes it clear that a weaker euro should not be an option for Europe. Europe has internal problems that should not be addressed through manipulation of the external exchange rate. Japan is already doing that since the exchange rate is the cutting-edge of its program for quantitative easing. Europe is too large for it to join in 'the fun' and begin a new era of competitive devaluation.

In March, in goods trade, exports from the Zone rose by 2.6% as imports fell by 4.1%. Over three months goods exports are growing at a 6.9% annual rate while goods imports falling in a 16.4% annual rate. Over the year there is nearly a 10 percentage point gap between the growth rates of exports and imports, as imports are falling at a 5.8% annual rate and exports are rising at a 3.9% annual rate. The chart of the of the trade situation makes it clear what an incredible spurt is occurring in the EMU current account.

This surging surplus will be buffering the negative effects of growth within the euro-Zone and also will be transmitting substantial and severe negative growth effects to the rest of the world. The countries in EMU are continuing to advance their export penetration in foreign markets while pushing aside imports at an extremely strong pace after a long period of deceleration.

The decline in imports is nowhere near as severe as it was during the financial crisis. However, in the financial crisis the entire global economy was mired in recession; the picture of the European economies was more or less mirrored by other global economies. Now the rest of the world is in the recovery phase but demand in Europe is continuing to sink. Europe is propping itself up by living off of exports to the rest of the world. In the last recession both exports and imports were in a free-fall decline everywhere - not so for Europe today. Remember since these are figures are for the European Monetary Union they cancel out all the internal trade. What we are looking at, are the net exports out of the euro area to the rest of the world versus the net imports into the euro area from the rest of the world.

We can take this chart as another reason why the G7 changed its tilt to try to get countries to see a role for growth rather than simply for austerity. Continued, or growing, recessions in Europe could act like a black hole to help suck other countries down into a morass of weakness. In a world economy where growth is fragile and still floundering even a country like the US that only sends a moderate proportion of its exports to Europe could find the blowback from declining European imports a substantial impediment to deal with.

Today the IMF has released a report urging The United Kingdom to change or moderate its program of austerity. UK authorities have indicated that they intend to hold the line and to continue to stay with what they are doing. Some recent data for the UK have been a little bit more upbeat playing into the hand of the policymakers that want to stay the course. On the other hand, fresh retail sales data for April were announced as unexpectedly weak, just today. Meanwhile the BOE is getting prepared to install a new Governor, one who appears to be a strong advocate of more QE. The bulk of the BOE policymakers are still opposed to that. The BOE may get a new face but not a new policy.

Let there be no doubt that the main problem facing the global economy is insufficient demand. There also are huge differences in competitiveness because of the extraordinarily rapid growth achieved in some developing nations that have developed without substantially raising their standard of living or letting their currencies appreciate to reflect their new status.

In the developed world countries are grappling with ongoing banking sector issues as well as an excessive buildup in debt. Over the past several years Europe has pursued a policy of harsh and unrelenting austerity. It would now seem to that policy has gone about as far down the road as it can. The US has been more willing to use fiscal policy but now finds itself faced with yawning future deficits based on ever richer promises made to future generations. In the US a recent pickup in tax revenues seems to be short-circuiting the air of urgency that had existed around the need to deal with those future deficits.

The world economy appears to have come to a subtle crossroads. Fiscal policy has been excessively tight. Monetary policy has been trying to fill in the gaps and may have been too loose for too long. And, wherever, you would prefer to see changes made, it is clear that the fiscal/monetary mix has moved onto a stage where it's threatening to future growth.

When countries or regions like the European Monetary Union or Japan use policy and their special circumstances to export their deflation to the rest of the world that world becomes more dangerous place.

While there certainly is evidence that the yen had been overcooked on the upside and is overdue for some of the backtracking that we are now seeing, in Europe the argument we make is different. Europe's problems are internal and they require an internal solution that Europe doesn't have the backbone to face. Its leading countries will not back its weak countries strongly enough, even when they undertake severe austerity. Europe's people want to keep the European dream alive, yet they unclear about whether they want to be European or nationalist. They don't want to give up on being 'European' but none of them wants to lose their national identity or control. Yet, the simplest solution for Europe would be to let the struggling countries leave the Zone and float their own currencies so that they could reset their competitiveness. So far that option is not on the table as Europe continues to kick the can down the road hoping that some new solution will somehow present itself. That seems unlikely.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief