Global| Dec 29 2016

Global| Dec 29 2016EMU Credit Growth Stirs...Is It Meaningful?

Summary

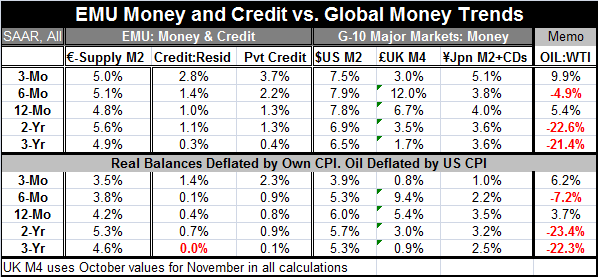

Money supply growth in the EMU and globally is still on trend or weaker. The lone exception here is a three-month pick-up in Japan's nominal monetary growth that is not reflected by a speed up in real money balances. But credit in the [...]

Money supply growth in the EMU and globally is still on trend or weaker. The lone exception here is a three-month pick-up in Japan's nominal monetary growth that is not reflected by a speed up in real money balances. But credit in the EMU is finally showing signs of stirring.

Money supply growth in the EMU and globally is still on trend or weaker. The lone exception here is a three-month pick-up in Japan's nominal monetary growth that is not reflected by a speed up in real money balances. But credit in the EMU is finally showing signs of stirring.

Over three months credit to residents in the EMU is up at a 2.8% pace and private credit is up at a 3.7% pace. These accelerations are echoed in their inflation-adjusted counterparts. Credit growth is steady at 1.3%, the same it was a year ago. But on shorter horizons, there is a speed up to a 2.2% pace over six months and again to that 3.7% pace over three months.

None of this is knock-your-socks-off news. But it is the best we have seen in quite some time. 2013 to 2015 showed a pick-up in loan growth that suddenly abated and flat-lined. This is the first real pick-up since 2015. Total credit growth is at its best year-on-year growth since late-2015, but private credit growth is at 1.3% year-on-year for three months running and that pace is its best since November 2011 which also was the last time when credit growth had a cluster of reasonably strong rates of growth. Inflation adjusted we have to go back to 2009 to find a string of year-over-year growth rates better than the last three months.

Globally, inflation has picked up. CPI inflation had been negative just about everywhere in mid-2015 then in early-2016 Japan and the EMU were visited by another negative inflation-rate episode. But that is over and inflation is on a steady rising in the U.S. and the U.K. with Japan showing a sharper but shorter term uptrend - all of this as oil prices firm and as OPEC tries to engineer them higher for good.

However, in real terms the EMU money supply growth rate has been steadily decelerating after peaking above a 6% pace in mid-2015. Globally, real money balances are showing flat growth in Japan and the U.S. They are accelerating in the U.K. and decelerating in the EMU. Money is not behind the push to prices (except in some very long and variable lag framework).

Oil prices on 12-month, six-month and three-month horizons are volatile, but underneath that facade of volatility they are rising steadily as the OPEC January 1 deadline for meeting output limitations approaches. WTI oil prices are up 5.4% over 12 months, down at a 4.9% annual rate over six months, and up at a 9.9% annual rate over three months. As of the data for this report (November), oil (WTI) is hovering at $45.60/barrel whereas in real time oil is up over $50/barrel, and around $53.86/barrel this morning.

Trends remain uninspiring and still convoluted, but there is also some hope in the growth of credit. In the U.S., a number of forward-looking measures have gotten quite strong on the expectation of a more business-friendly president and Congress. Still, most of the gains in these measures are from expectations while real-time data show less improvement. Europe is still under geopolitical strains, but Italy is an example of a country seemingly under a lot of pressure where consumer confidence has nonetheless had a nice rebound amid economic and political chaos. These economic and geopolitical times are hard to handicap- as we all know in the wake of the Brexit vote, the election of Trump and PM Matteo Renzi's failed Italian referendum. Central banks may insist that they need to make forward-looking policies, but we have no evidence that anyone can look forward these days with any amount of clarity. The Fed in the U.S. has hiked rates for only the second time in a year and sees three more rate hikes ahead. Jens Weidmann at the Bundesbank is warning that ECB policy must focus only on inflation. Everyone has an opinion on policy. But the bad forecasting record of central banks and inability of polls to accurately gauge national moods and leanings put all policy moves on notice and make all policy changes suspect. Stay alert and stay tuned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief