Global| Mar 03 2015

Global| Mar 03 2015EMU Caught between a Rock and Soft Place as Germany Plays Ball instead of Games

Summary

Prices in the euro area continue to push lower as weak growth and dropping energy prices undercut the strength from price trends on two separate fronts. As the chart shows, PPI and CPI trends are pressing lower in the EMU. The table [...]

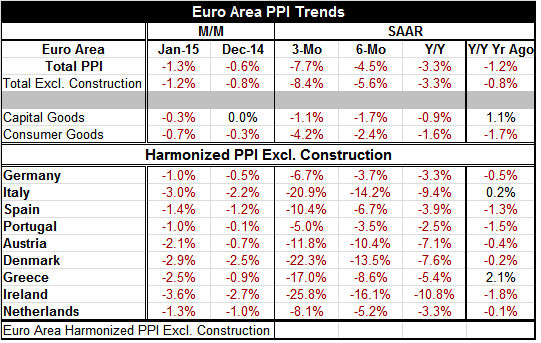

Prices in the euro area continue to push lower as weak growth and dropping energy prices undercut the strength from price trends on two separate fronts. As the chart shows, PPI and CPI trends are pressing lower in the EMU. The table of PPI results shows red ink for each of these nine early-reporting countries for the recent two months as well as for all three-month, six-month and 12-month growth rates. Rarely are price results this dramatic and this uniform even for a region like the euro area.

Prices in the euro area continue to push lower as weak growth and dropping energy prices undercut the strength from price trends on two separate fronts. As the chart shows, PPI and CPI trends are pressing lower in the EMU. The table of PPI results shows red ink for each of these nine early-reporting countries for the recent two months as well as for all three-month, six-month and 12-month growth rates. Rarely are price results this dramatic and this uniform even for a region like the euro area.

Over three months, prices are falling at double digit annual rates in six of nine nations. The pace of decline is accelerating in every single country from 12 months to six months to three months without exception. That is, except for functional product categories, where capital goods prices are not decelerating the same as other PPI prices.

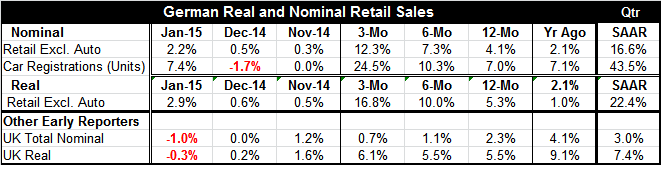

For all the dramatic price weakness, the German economy remains strong and its consumer sector has heated up showing a seven-year high in retail sales growth. Not only that, but the German fiscal budget is in surplus and Germany has decided to step up domestic investment activities by about five billion euros in the wake of posting its first budget surplus since 1969.

The table below chronicles German retail sales activities which are strong, rising by 2.2% in January. Unlike times in the past when German sales ebbed and flowed between high and low rates of growth, retail sales are building a clear head of steam as sales are accelerating to a 12.3% pace over three months from 7.3% over six months and 4.1% over 12 months. Real sales excluding autos are on the same sort of accelerating ride and car registrations are accelerating as well. The picture of the German consumer caught in the rapture of spending is as clear as it is unique.

Germany is seeing its first budget surplus since 1969, the first in 46 years. Germany has decided to engage in more investment spending with this largesse. This is something that will assist the German economy and potentially the rest of the euro area. It is a very welcome bit of economic news and unexpected.

It comes as German spending is not just accelerating but appears to be building a head of steam in the new quarter as real retail sales ex-auto spending is up at a 22.4% annual rate in Q1 already. Car registrations are up at a 43% annual rate in Q1. German growth is suddenly bunching up.

So Europe at last may be getting the `locomotive effect' from Germany, something it has long sought and that I have long doubted it would ever see. How long Germany will be willing to nurture this sort of growth remains to be seen. But for now Germany is going along with funding Greece and going with the flow of strong growth- even adding a flow of investment to it. Germany has become a team player in Europe with the exception of the Bundesbank which stepped back from QE and forced it to be done on a risk-off basis with local central banks executing the local programs under QE and taking the risk. It is still a remarkable step forward. While Germany still pursues its own interests on the foreign policy front and the Bundesbank remains highly protective of the monetary schematic in Europe, Germany is being much more of a team player than it has been since the EMU was founded.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief