Global| Dec 12 2019

Global| Dec 12 2019EMU Area IP Sinks Again As Inflation Undershoots

Summary

As disappointing as this news is, it comes on a day with a more cheerful note. Germany's IFO has declared that the downward spiral in German industry is over and that it now expects stabilization and growth. That is something to look [...]

As disappointing as this news is, it comes on a day with a more cheerful note. Germany's IFO has declared that the downward spiral in German industry is over and that it now expects stabilization and growth. That is something to look forward to.

As disappointing as this news is, it comes on a day with a more cheerful note. Germany's IFO has declared that the downward spiral in German industry is over and that it now expects stabilization and growth. That is something to look forward to.

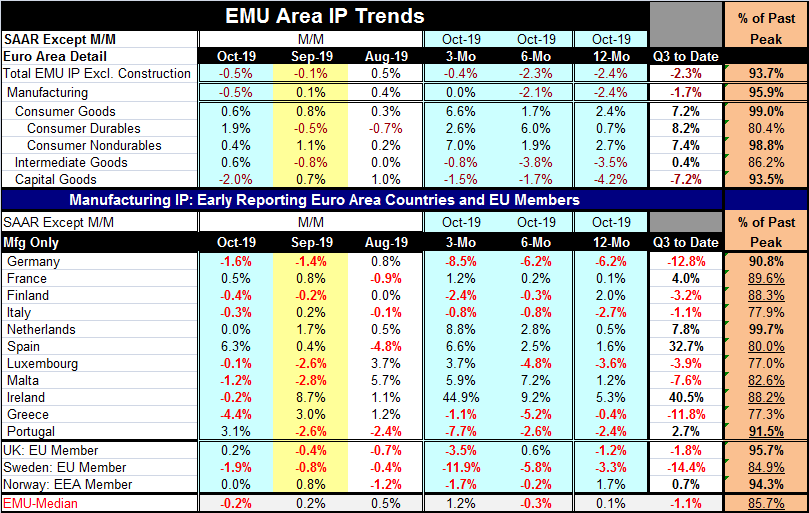

For now, however, the facts in front of us are still sour. It's a weak start to a new quarter with IP falling at a 2.3% annual rate measuring the growth of IP in October relative to the Q3 average (QTD: Quarter-to-date). Overall IP is falling and it is falling over 12 months, six months and three months although on that timeline there is a deceleration in the weakness. Consumer goods output for both sub-sectors as well as overall consumer goods output is up on each of these sub-periods and without a clear trend but on very strong gains over the last three months. Intermediate goods output declines on all three time segments, but its weakening trend also is diminishing. Capital goods output also is declining on each time segment and for this sector the decline in the pace of weakness is quite clear.

Manufacturing overall shows a diminishing pace of weakness culminating in flat output over the last three months. This is despite a sizeable 0.5% drop in October alone.

By country

The eleven reporting early-to-original EMU members show output declines in October in seven members. Decliners include Germany, the largest EMU economy, and Italy the third largest EMU economy. France and Spain (numbers two and four by GDP size) show gains in October and for Spain it's a very strong gain. In September five EMU members showed declines and in August four showed declines. Despite the IFO statement on Germany, across EMU the breadth of weakness has spread but as the sector growth rates show the intensity of the decline seems to be less virulent.

Five EMU members show output declines over three months, six show declines over six months and five register year-over-year declines in output. The EU and EEA countries of the U.K., Sweden and Norway mostly show output declines (see Table for their stories).

Quarter-to-date trends

The quarter-to-date shows IP declines in six of eleven EMU members and two of the other countries in the table. Germany is especially weak. Spain, Ireland, and to a lesser extent the Netherlands, are relatively strong. Looking at sectors among the EMU members, manufacturing overall shows a quarter-to-date decline early in Q4. Consumer goods output, in contrast, is relatively strong, intermediate goods output is positive but weak, while capital goods output is extremely weak to start Q4.

Output as a percentage of past peak

By Sector: Output as a percentage of past peak is strongest by sector for consumer goods, but that is on the back of nondurables output as durable goods are some 20% below their past peak in output generation. Intermediate goods are some 14% below their past cycle peak and capital goods output is 7% below its past peak.

By Country: By country output is at 90% of its past peak or better in Germany (despite recent weakness), the Netherlands and in Portugal. Output is at least 85% of its past peak in France, Finland, and Ireland. In the rest of the countries, there should be clear excess slack to keep price pressures in check. Outside of EMU, the U.K. and Norway have output only 5% to 6% short of their respective past cycle peaks. Sweden is about 15% off its past peak.

Momentum by country

The IP picture for Europe that emerges is a mixed one albeit with downward momentum and some countries with some still worrisome weakness. Even so some, the Netherlands, Spain, Malta, Ireland and to a lesser extent, France, show the emergence of upward momentum in a few cases; some of these have considerable momentum. However, Portugal, Greece Italy and Germany each show output declines of some degree across the timeline; only Portugal and Germany show clear deceleration in progress. And we have the IFO assessment to give us hope that the German situation is in flux in a new direction.

Inflation

Separately, inflation-data for November is being finalized and the results show ongoing target undershooting with widespread support for that trend. The ECB met today, its first meeting chaired by Christine Lagarde, and policy is on hold- the expected result.

ECB meets

Ms. Lagarde and the ECB have a clear conundrum as the ECB has a price-only objective and inflation has run below 2% since February 2013 with only a five-month exception of 2% or 2%-plus growth over the five-months ended in October 2018. The ECB has fallen far below the just-less-than-2% it targets and yet the conservative members of the ECB board are restive about the having negative rates and other stimulus in place.

Shortfall...how far short?

Since February 2013, inflation in the EMU area has expanded at a 0.9% annual rate over 81 months, a span of six-and three-quarters years. That means that the EMU price level over this period is roughly 6 and 3/4 percentage points below the targeted pace for EMU inflation of just under 2%. This result is straight forward since the short fall is about one-percentage point per year although with compounding the short fall in the PRICE LEVEL rises to nearly 7 percentage points.

Summing up

My point in this calculation is to demonstrate how far behind its target for inflation that the ECB has fallen; much like in the U.S. where the shortfall is less severe, however. Yet, in both the U.S. and in the EMU, policymakers seem to be more worried about the period ahead and the potential for inflation and for ‘excessive ease' to create bad economic incentives. In neither the U.S. nor in Europe are monetary officials dealing with the consequences of policy having delivered less inflation and less ‘stimulus' that it should have. In the case of the ECB, the short fall is impressively large. Policy hawks or conservatives on the ECB policy committee remain more worried about excess stimulus than about having provided too-little inflation. It is curious how after a long period of tempered inflation with still modest growth and even economic weakness, in an environment of exceptional global competition, there remains worry about overdoing it. Talk about fighting the last war instead of the next war - I can' think of a better example.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief