Global| Jun 04 2015

Global| Jun 04 2015Emerging Economies Struggle Along with Everyone Else

Summary

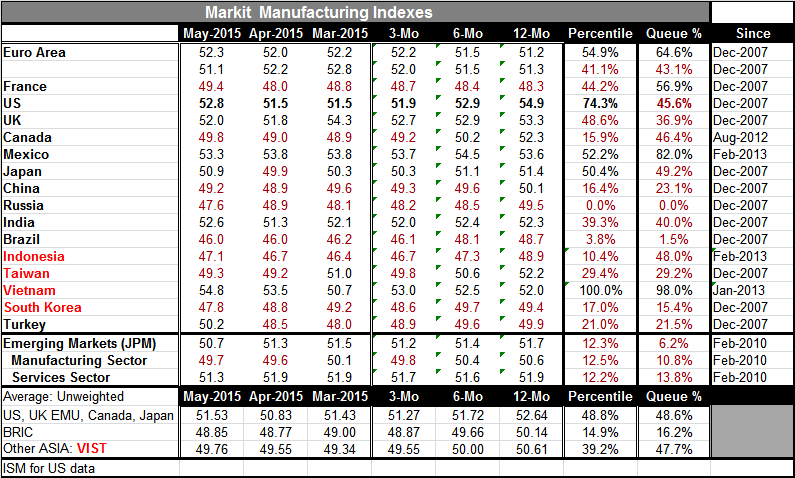

The emerging market economies' consolidated PMI fell to 50.7 in May from 51.3 in April, dropping it to a 6th percentile standing in its historic queue of data since 2010. The overall reading's percentile standing is at 6.2% and is [...]

The emerging market economies' consolidated PMI fell to 50.7 in May from 51.3 in April, dropping it to a 6th percentile standing in its historic queue of data since 2010. The overall reading's percentile standing is at 6.2% and is lower than either of the sector readings as manufacturing has a 10.8 percentile standing and services has a 13.8 percentile standing. What that means is that the depth and the coincident weakness of the two sectors is unusual. At this aggregated percentile standing, the overall PMI for emerging markets is barely above 50 at 50.7.

The emerging market economies' consolidated PMI fell to 50.7 in May from 51.3 in April, dropping it to a 6th percentile standing in its historic queue of data since 2010. The overall reading's percentile standing is at 6.2% and is lower than either of the sector readings as manufacturing has a 10.8 percentile standing and services has a 13.8 percentile standing. What that means is that the depth and the coincident weakness of the two sectors is unusual. At this aggregated percentile standing, the overall PMI for emerging markets is barely above 50 at 50.7.

Emerging markets have a lower overall percentile standing than the BRIC countries which themselves are weak at a 16th percentile standing. Other Asia (Indonesia, Taiwan, Vietnam and South Korea) is much stronger with a 47th percentile standing. The mostly G-10 grouping of the U.S., Canada, Japan and the EMU has only an unweighted average standing at the 49th percentile. These groups are only for reference as they are not weighted by GDP. But they do tell something of global conditions.

The developed economies are struggling, but the developing and emerging economies are having an even harder time. In the BRIC group, the Russian manufacturing sector is at its low since January 2010 and Brazil's standing is just above its low. China stands at its 23rd percentile. India is the strong one in its 40th percentile, where output is still below its median, but with a diffusion value of 52.6 at least output in India is not shrinking.

Other Asia is worse off than its average indicates. Vietnam has a huge 98th percentile standing that greatly elevates the average of the group. Within this group, South Korea has a 15th percentile standing and Taiwan has a 29th percentile standing. Indonesia has a 48th percentile standing. Only Vietnam has a raw diffusion reading that indicates that output is increasing. Individual countries are doing quite a bit differently from their group average. Of course, using a GDP weighted index would not make things any different as there would still be huge differences among countries.

Taken as an overall proposition, the divergence across countries both developed and developing measured by the standard deviation of manufacturing PMIs across all countries with observations back to January 2010, shows a 36th percentile standing for dispersion. That means that dispersion has been lower than this only 36% of the time since January 2010. While that is somewhat encouraging, dispersion has been increasing unevenly over the last six months. At the same time, the average global manufacturing reading has been slipping over the last one and one half years. The unweighted global manufacturing PMI has fallen to a diffusion level that is nearly exactly at 50- a neutral reading indicating no change in output.

The clear message from looking at global manufacturing PMIs, their levels, their trends and their dispersion is that the world economy is not doing well and is not getting better. Yet in the U.S., an important source of global demand, the central bank is itching to hike rates. Consumers are still so shell shocked they are not spending income as they earn it; instead the saving rate is rising. Instead of using fiscal policy for stimulus, the U.S. is preparing to use less monetary stimulus. Yet, huge differences among countries' PMI readings exist and are being sustained. There is no global policy to arrest this development nor are individual country policies so aligned. At a time when growth is insufficient, policies are still aimed mostly at austerity and are leaning too much on monetary policy to make the difference. However, you want to categorize global policy- it is not working. And it is not working for everyone, developed countries, developing economies, emerging economies alike. In the final analysis, less is not more.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief