Global| Oct 07 2002

Global| Oct 07 2002ECRI Leading Indicators Fell Further

by:Tom Moeller

|in:Economy in Brief

Summary

The Weekly Leading Index of the US economy published by the Economic Cycle Research Institute (ECRI) has fallen 4.0% from the weekly peak reached late this past May. The indicator's six-month growth rate, perhaps the more important [...]

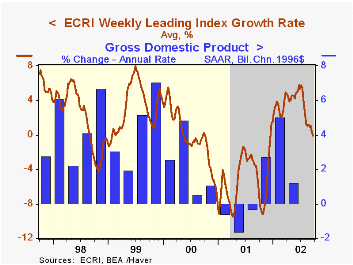

The Weekly Leading Index of the US economy published by the Economic Cycle Research Institute (ECRI) has fallen 4.0% from the weekly peak reached late this past May.

The indicator's six-month growth rate, perhaps the more important indicator, fell to -0.1%, the first negative reading since December 2001.

Construction of the ECRI Leading Index differs from the Index of Leading Economic Indicators published by the Conference Board. Nevertheless there has been an 80% correlation between the annual percent change in the two over the last 20 years.

The components of the index are money supply plus stock & bond mutual funds, the JOC-ECRI industrial materials price index, mortgage applications, bond quality spreads, stock prices, bond yields, and initial jobless insurance claims.

The median lead of the ECRI index at business cycle peaks has been 10.5 months and at cycle troughs 3.0 months. The sideways movement of the leading index in 2002 may or may not signal something about the economy's growth rate.

| ECRI | 9/20/02 | 9/13/02 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Weekly Leading Index | 119.0 | 119.3 | 3.0% | -5.0% | 0.8% | 2.4% |

by Tom Moeller October 7, 2002

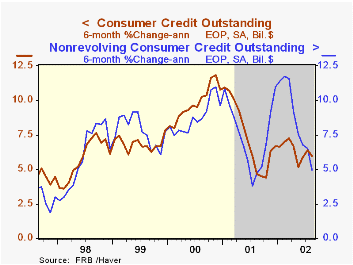

Consumer credit outstanding rose $4.2B (0.2%) in August, quite a bit less than expected. July figures were revised down slightly due to a lowered figure for nonrevolving credit. So far this year, consumer credit outstanding has risen at a 5.7% annual rate.

Revolving credit growth, up 0.5%, returned to the monthly rate of growth seen in in the months prior to July's 0.9% surge. Year to date revolving credit growth was 5.6% (AR).

One-month growth in nonrevolving credit extension, which was virtually unchanged, slowed to its lowest since June 1999. Nonrevolving extension is up 5.7% (AR) YTD.

Nonrevolving credit extension (NSA) was notably weak from finance companies where it fell.

| Consumer Credit Outstanding | Aug m/m | July m/m | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Total | $4.2B | $10.0B | 6.5% | 6.9% | 10.2% | 7.5% |

| Revolving | $3.9B | $6.4B | 4.1% | 5.0% | 11.5% | 6.3% |

| Nonrevolving | $0.2B | $3.7B | 8.3% | 8.3% | 9.2% | 8.4% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief