Global| Oct 20 2009

Global| Oct 20 2009e-Schism! Italy and France Orders Show Signs of Past Progress, then Italy Backtracks

Summary

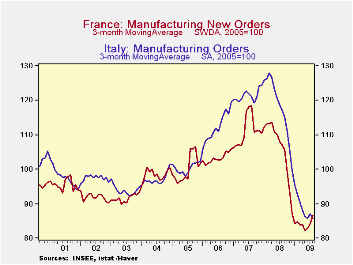

Industrial orders for Italy and France show strong signs of having shaken off the worst of the recession as each of them has rebounded sharply into 2009. But in August their paths have diverged. France continues to show signs of [...]

Industrial orders for Italy and France show strong signs of having shaken off the worst of the recession as each of them has rebounded sharply into 2009. But in August their paths have diverged. France continues to show signs of progress in leaps and bounds as orders are up by 7.9% m/m and are falling at an annual pace of just 11.6% over 6-months. By comparison Italy’s orders have plunged by 8.6% m/m in August and are declining at an annual rate of 18.8% over six months- and are worse over three months.

France reports increases in foreign orders and a larger gain in orders overall as it domestic orders are surging. In Italy both foreign and domestic orders are dropping: at -12.8% pace of decline; Italy’s foreign order drop is twice as large as its domestic drop in August. This decline is consistent with a drop-off in foreign orders first reported by Germany in July but German foreign orders snapped back in August. Maybe this foreign order weakness in Italy will prove to be temporary. But Italy still has two months in a row of dropping domestic orders it must deal with. This weakness, unfortunately, does not look like a fluke.

The starkest contrast may be over three months where French orders are rising at a 43% annual rate compared to Italy where overall orders are off at a 19% annual rate led by a collapse in domestic orders that are dropping at a 25.6% annual rate.

Divergences like this will create problems for policy in the e-zone. There is only one exchange rate and one monetary policy for all of the e-zone. The French and Italian economies, two of the larger EMU economies, are not on compatible paths. If this continues it could make for some real difficulties in policymaking. For sure the split- if it continues - will put a stop to the rise in the euro. Italy –despite having some special problems - is too-big of an economy to be ignored by markets or by the ECB.

Italy has recently surprised us with a sharp rise in consumer sentiment but this was reported even as industrial sentiment was still eroding. The weak industrial order result gives the drop off in the assessment of Italian businesses more credence. Clearly Italy is an economy with challenges and those problems could spillover into the e-Zone.

| Saar exept m/mAug- | 09 | Jul-09 | Jun-09 | 3-mo6-mo12-mo | ||

| Total | -8.6% | 2.1% | 1.6% | -19.0% | -18.8% | -29.8% |

| Foreign | -12.8% | 12.8% | 0.4% | -5.0% | -20.9% | -29.7% |

| Domestic | -6.1% | -3.2% | 2.2% | -25.6% | -17.6% | -29.9% |

| Memo | ||||||

| Sales | -1.4% | 0.7% | -1.7% | -9.5% | -7.8% | -21.7% |

| French Orders | ||||||

| Saar exept m/mAug- | 09 | Jul-09 | Jun-09 | 3-mo6-mo12-mo | ||

| Total | 7.9% | 3.8% | -2.3% | 43.7% | -11.6% | -21.3% |

| Foreign | 0.8% | 13.8% | -3.2% | 52.0% | 35.8% | -14.4% |

| IP xConstruct | 1.9% | 0.8% | 0.5% | 13.7% | 8.6% | -11.5% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief