Global| Apr 23 2009

Global| Apr 23 2009E- Area PMIs Are Still Low-Valued But Jump

Summary

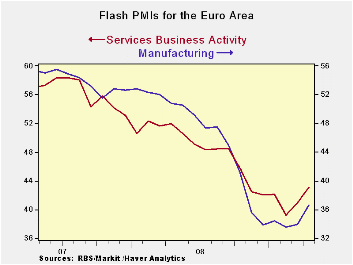

The PMI’s for the zone are up sharply in April. At 36.33 the MFG PMI is still in the lower 11 percentile of its range. The services reading at 43.10 is in the lower 16 percentile of its range. These are weak positions that speak of a [...]

The PMI’s for the zone are up sharply in April. At 36.33 the

MFG PMI is still in the lower 11 percentile of its range. The services

reading at 43.10 is in the lower 16 percentile of its range. These are

weak positions that speak of a continuing low level of economic

activity. But there is also some good news.

In April the MFG PMI has made its largest jump since the

series began in June of 1997. The MFG index is up by 2.73 points in

April. Similarly the Services PMI has risen by 2.15 points and that is

the fourth largest jump m/m rise for services since Feb of 1999 when

that series started.

The jump for services comes on the heels of a 1.17 point gain

in the index in March which was the eight largest rise at that time. So

services in Europe are making greater strides toward improvement in the

last few months.

Of course the level of the two indices is still very low. Both

are below the break-even line of 50; both indices attest to the

continuing unraveling of economic activity in Europe. On top of that a

new poll by the German economic think-tanks projects a 6% drop in GDP

for the year ahead in that key e-Zone country. For the UK, Barclays CEO

has just prognosticated a deep and long downturn in the UK. In France

has a new domestic survey on business sentiment says that it has gained

some small ground.

There are both scattered signs of improvement in Europe and at

the same time pessimistic assessments of where the economy is as well

as of where it is going over the rest of the year. It is not clear

which of these signals markets are going to latch onto. Still, it is

reassuring to see the down drafts slowing. The report of new industrial

orders out the e-Zone today is an example of this topsy-turvy news. EMU

orders took the largest Yr/Yr drop in their history today. Still the

series reported a one of its smallest month-to-month drops. So, even as

the year /year data confirm how bad the orders drop has become, there

is evidence that the declines are set to slow. The bottom line is that

Europe is probably worse off than many have been thinking- including

the authorities that have been reluctant to act aggressively and even

stiffed the US request to do more at the recently concluded G-20

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the E-Zone | ||

| MFG | Services | |

| Apr-09 | 36.66 | 43.10 |

| Mar-09 | 33.93 | 40.95 |

| Feb-09 | 33.55 | 39.24 |

| Jan-09 | 34.42 | 42.16 |

| Averages | ||

| 3-Mo | 33.97 | 41.10 |

| 6-Mo | 35.41 | 41.66 |

| 12-Mo | 41.90 | 45.06 |

| 127-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 11.6% | 16.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief